Futures Fall To Start Now Quarter With Warsh Sintra Comments On Deck

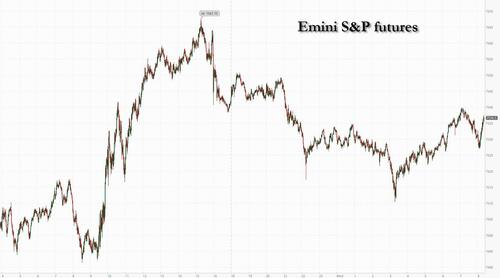

US equity futures point to a softer start to the third quarter as investors await a fresh batch of economic data and the first major overseas appearance by Fed Chair Kevin Warsh. As of 8:20am ET, S&P futures are down 0.2%, off session lows, while Nasdaq futures are down 0.6: techs lags following NDX’s 3.9% gain over the last 2 days; in premarket trading, chipmakers, which did much of the heavy lifting as investors piled into AI beneficiaries, were weaker with Mag7s mostly lower. Nike dropped 2% following a cautious outlook. Software names including Microsoft gained. Cyclicals are under pressure with HC and Staples leading a Defensives bid. Overnight the US removed Anthropic’s foreign access restrictions. Bond yields are flat to down 1bp, and USD is bid as positive progress is reported in US / Iran talk. In commodities, crude prices are lower as distillates rise; WTI futures are down about 0.8% following the biggest quarterly drop since the pandemic.Metals are under pressure, with Ags bid as the group has been the recent outperformer. US economic data calendar includes June ADP employment change (8:15am), June final S&P Global manufacturing PMI (9:45am) and June ISM manufacturing (10am).

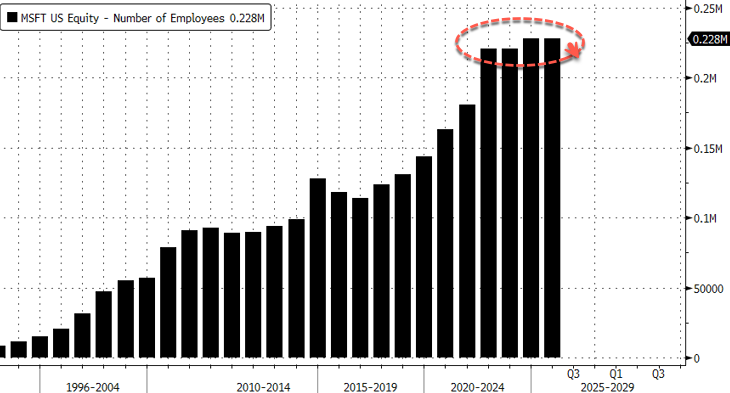

In premarket trading, Microsoft outperforms Magnificent 7 peers in premarket trading. Business Insider reports that the company is planning to announce job cuts, impacting thousands of roles, citing people it didn’t identify. Shares are up 1.7%. Other Mag 7 stocks are mixed early Wednesday (Alphabet -0.4%, Nvidia -0.6%, Apple -0.09%, Tesla -0.4%, Amazon +0.9%, Meta Platforms +0.3%). Here are some of the biggest US movers today:

- Abbott Lab (ABT) shares are up 0.03% in premarket trading after Baird initiated coverage of the stock with an outperform rating, saying a clearer path to upside for the medical device maker is “beginning to emerge.”

- Alcoa Corp. (AA) is down 5.0% after the mining company agreed to buy South32 Ltd.’s bauxite, alumina and aluminum assets in a deal worth as much as $5.6 billion. Morgan Stanley expects a negative reaction on the transaction multiple and limited visibility on synergies.

- Bloom Energy (BE) shares rise 8.3% in premarket trading on Wednesday after the company expanded its partnership with Brookfield from $5 billion to $25 billion to help grow the fuel cell partnership globally.

- Dow Inc. shares are down 0.7% in premarket trading, after RBC Capital Markets downgraded the chemical company to sector perform from outperform. Mizuho cut its price target to $35 from $43.

- FMC shares rise 7.0% after the company said Tessenderlo Group will make a strategic minority equity investment of about $400 million at $13.30 per share. Shares in Tessenderlo gain 3.4% in Brussels.

- General Mills shares are up 4.89% after the packaged food company’s adjusted earnings per share for the fourth quarter beat the average analyst estimate.

- Grindr shares gain 6.9% ahead of the bell after Morgan Stanley upgrades the LGBTQ community dating company to overweight from equal-weight, highlighting monetizing opportunities. The upgrade leaves the stock with only buy-equivalent ratings.

- NASA selected Astrobotic, Firefly Aerospace and Intuitive Machines for four moon missions in late 2028 as part of the Moon Base Program. Intuitive and Firefly shares are up 7.2% and 2.7%, respectively.

- Nike shares fall 1.6% in premarket trading on Wednesday after the sneaker company said on its conference call revenue expectations for the next two quarters are now seen down low-to-mid single digits from down low single digits earlier.

- Klarna shares rise 6.9% after a Swedish Patent and Market court ordered Google to pay SEK14.3b ($1.47b) to Klarna’s subsidiary PriceRunner International following antitrust damages proceedings.

- Microsoft outperforms Magnificent 7 peers in premarket trading. Business Insider reports that the company is planning to announce job cuts, impacting thousands of roles, citing people it didn’t identify. Shares are up 1.7%.

- Shares in ServiceNow, Salesforce and Check Point Software rise in premarket trading as Guggenheim upgraded all three to buy from neutral, saying that the fatal AI bear case on software is a “hallucination.” ServiceNow +5.0%, Salesforce +3.3% and Check Point Software +3.1%.

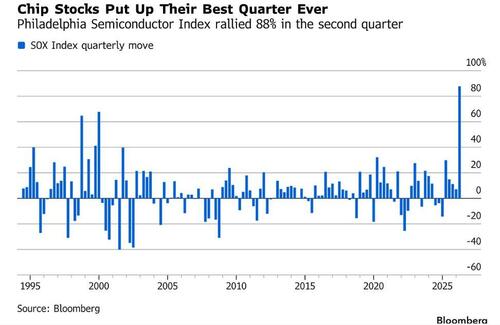

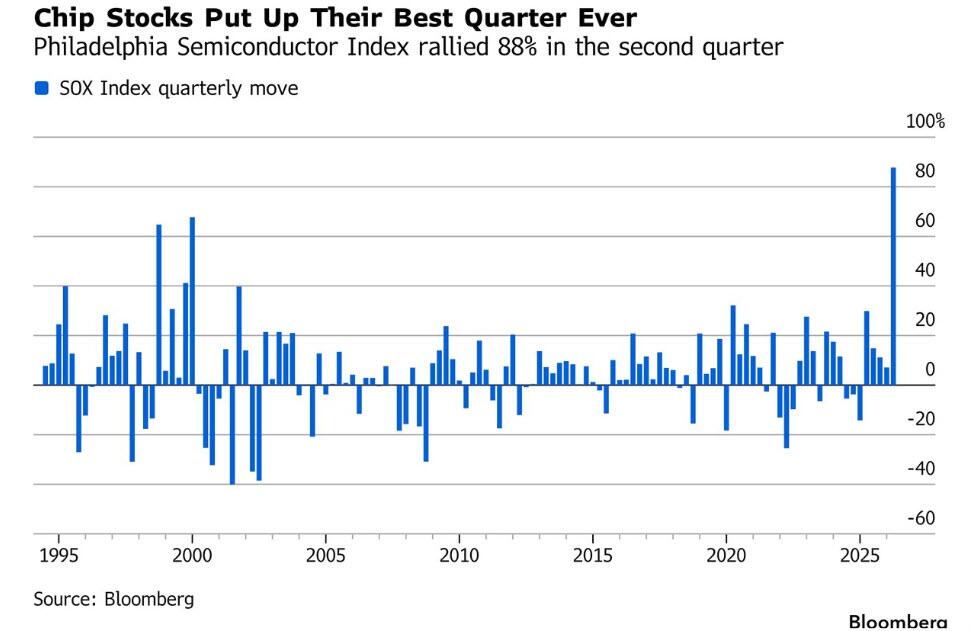

US stocks just posted their best quarter in six years with fresh signs of economic resilience bolstering confidence in corporate earnings. The rally added more than $8 trillion to the S&P 500’s market value over the past three months. The SOX semiconductor index posted its strongest quarter on record.

“As long as earnings continue to be good and broaden out, I think we will get continued gains through the second half — probably lower than what we saw in the first half — but I think it will quite broadly based,” said Goldman’s Chief Global Equity Strategist Peter Oppenheimer. Technology remains the main driver of earnings growth even as hyperscalers have “derated” on concerns about longer-term returns, Oppenheimer said. Their heavy spending should continue to underpin growth and “trickle out” into parts of the economy supporting the AI infrastructure buildout, he told Bloomberg TV.

Meanwhile, concentrated market leadership, passive investing, retail flows, leverage and a new volatility regime are increasingly dictating price action, Citadel Securities’ Scott Rubner wrote in a Tuesday note.

In other assets, the global oil market is set to swing back into oversupply even after strategic reserves are replenished, according to Goldman Sachs. Japan’s currency chief suggested intervention was an effective strategy.

Today’s main event takes place in Sintra, Portugal and the ECB’s annual symposium, where Warsh joins President Christine Lagarde and Bank of England Governor Andrew Bailey at 9 a.m. New York time. Bloomberg Economics expects Warsh to strike a carefully balanced tone after signaling different messages to hawks and doves at the June FOMC meeting. After his pledge last month to deliver price stability sent the dollar and shorter-dated Treasury yields higher, traders will be looking for further clues on the rate path for the year ahead.

“Given the absence of forward guidance from the Fed now, there is going to be intense focus on any comments” from Warsh, wrote Chris Turner, a foreign-exchange strategist at ING Bank NV. “A focus on price stability can keep the dollar bid.”

Investors are increasingly shifting focus to growing price pressures in an economy that’s firing strongly, with expectations building for a solid payrolls report on Thursday.

European stocks also slipped in early Wednesday trading, with indexes dragged down by mining companies on the back of weaker commodity prices. The Stoxx 600 falls 0.2% to 640.52 with 229 members up, 361 down, and 10 unchanged. Among individual stocks, Switzerland’s Galderma fell the most in over a year after the US FDA turned down the firm’s Botox rival Relfydess. CMC Markets jumped to a fresh record high after raising its guidance. Here are the biggest movers Wednesday:

- CMC Markets shares soar as much as 25% to a fresh record after the UK financial derivatives dealer raised its guidance for 2027 net operating income citing strong momentum

- Renault shares rise as much as 4.5% after the French carmaker hosted a pre-close call with analysts ahead of its first-half results scheduled for the end of the month

- Tecan shares rise as much as 10% after UBS raised its recommendation in the Swiss laboratory technology group to buy from hold, saying top-line growth has bottomed out and expected margin improvements are not yet priced in

- Aker ASA gains as much as 11%, the most since January, after it agreed to sell its shares in Cognite Holding to Schneider Electric, which meanwhile dropped as much as 3%

- ASOS shares gain as much as 12% after announcing it will sell its Atlanta fulfilment center and associated automation assets for net proceeds of ~£48 million

- RS Group rises as much as 5.1%, the most since May 20, as Deutsche Bank upgrades the distributor of electrical and industrial products to buy from hold on a strengthening recovery case

- Galderma shares slump as much as 6.6%, the most in more than a year, after the US Food and Drug Administration turned down the Swiss dermatology firm’s rival Botox treatment Relfydess

- AB Foods shares fall as much as 3.6%, the most in over two months, after the conglomerate delivered an underwhelming third-quarter update and downgraded the outlook for its sugar business in the 2026 and 2027 fiscal years

- Bucher shares fall as much as 3.6%, the most since April 28, after Kepler Cheuvreux cut its price target on the Swiss agricultural machinery company, citing capex sentiment indicators in Europe that are nearing recession territory

- Medacta drops as much as 4.1%, the most in a month, as Stifel cuts its full-year organic revenue growth estimates for the Swiss medical-implant firm to the midpoint of guidance

Earlier, Asian stocks fluctuated on Wednesday after capping their best quarter in 17 years, as investors paused to assess the outlook for the AI rally that has been a major driver of the gains. The MSCI Asia Pacific Index swung between gains and losses for most of the day. Declines in South Korean chipmakers Samsung Electronics and SK Hynix were a major drag, offsetting gains in Japan and Taiwan — which together account for about half of the benchmark. Hong Kong markets were closed for a public holiday. The Kospi declined as the National Pension Service was set to resume rebalancing its domestic stock holdings after a temporary suspension.

The Asian benchmark climbed 21% last quarter while a subgauge of tech shares soared a record 74%. However, the sector’s rally slowed in June as rising concerns over the payoff from hefty AI investments, coupled with elevated valuations and crowded positioning, sparked intermittent pullbacks, particularly in Korean shares. The AI trade within Asia has been “quite narrow,” Hebe Chen, senior market analyst at Vantage Global Prime, said in a Bloomberg Television interview. “That overcrowding is often exposed to a higher and sharper fall if the tide changes, because this rally has attracted so much liquidity,” she added.

In FX, The Bloomberg Dollar Spot index rises 0.2% to its highest level this week before Fed Chairman Kevin Warsh appears on a policy panel alongside peers from Europe and the UK.

Treasuries are narrowly mixed with yields less than a basis point away from their closing levels on Tuesday, when they climbed 7bp-9bp amid a flurry of month-end selling in futures. WTI crude oil futures are down, underpinning Treasuries, as traders monitor peace talks between the US and Iran. US 10-year yields are down 1bp to around 4.46%, Treasuries are little changed on the day while curve spreads are marginally steeper. European bonds lag Treasuries, following the late weakness in futures into the US month-end index rebalancing, which also saw the day’s steepening move accelerate. Focal points of US session include key manufacturing data and unscripted comments by Fed Chairman Kevin Warsh.

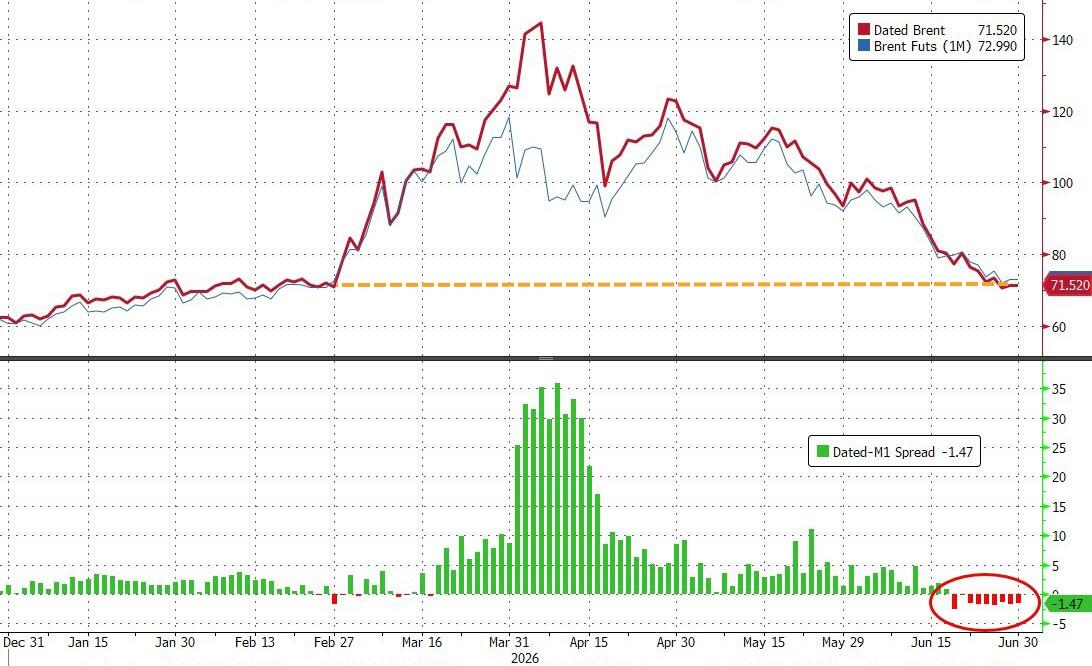

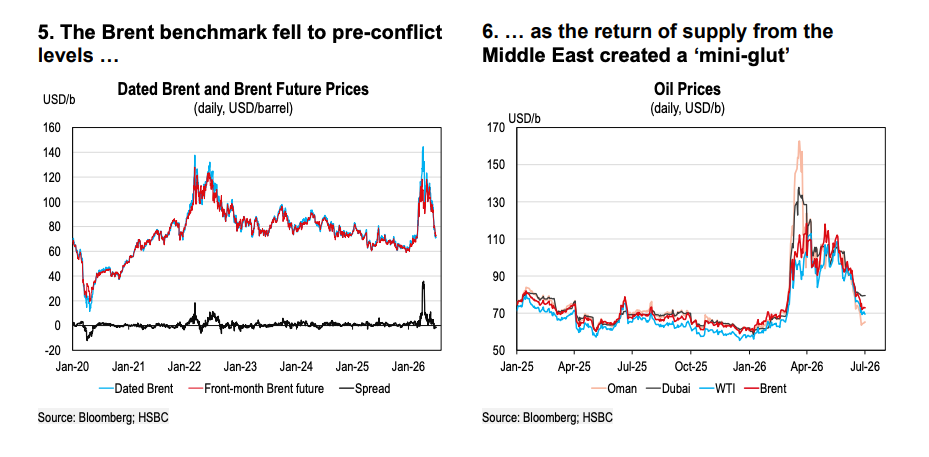

In commodities, Brent extended declines, falling 1% to $72.20 a barrel. US negotiators held positive discussions in Qatar and progress is being made on technical talks with Iran, according to a senior administration official, as the countries seek to turn an interim peace deal into a permanent end to the war. That’s been of little support to European government bonds, however. UK and German 10-year borrowing costs rise 2 basis points each. Precious metals decline, with spot silver down over 1%.

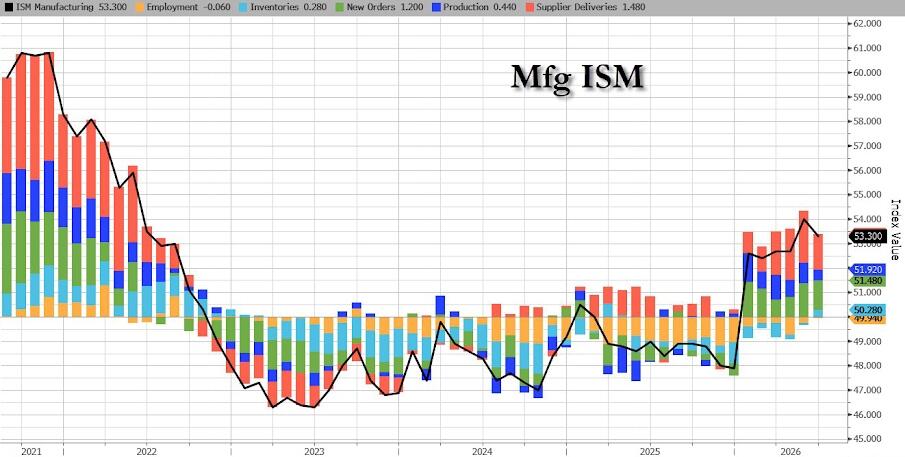

US economic data calendar includes June ADP employment change (8:15am), June final S&P Global manufacturing PMI (9:45am) and June ISM manufacturing (10am). Fed speaker slate includes only Warsh, participating in an ECB panel in Sintra, Portugal at 9am New York time

Market Snapshot

Top Overnight News

- Iran and U.S.-allied Oman are moving forward with plans to collect payment for ships transiting the Strait of Hormuz, despite public American objections. NYT

- US negotiators Steve Witkoff and Jared Kushner held positive discussions in Qatar and progress is being made on technical talks with Iran, according to a senior administration official, as the countries seek to turn an interim peace deal into a permanent end to the war. BBG

- The US removed foreign access restrictions on Anthropic’s Fable 5 AI model. The company said it will restore global access across its platforms starting today. BBG

- Xi Jinping signaled China’s ambition to play a more high-profile role, a strategy that involves rallying developing nations as a counterweight to what he views as fading US influence. BBG

- The yen pared some losses after Japan’s top FX official said past intervention efforts were successful, adding that Washington remains in close communication with Tokyo over FX policy. South Korea’s won slid toward its weakest level since the global financial crisis. BBG

- Euro-area inflation eased more than anticipated in June. Consumer prices rose 2.8% from a year ago, down from 3.2% a month earlier. BBG

- President Trump has weighed a return to all-out war with Iran, holding multiple conversations in recent days with Defense Secretary Pete Hegseth and Chairman of the Joint Chiefs of Staff Gen. Dan Caine on more strikes, but has decided to stick with diplomatic talks for now, according to U.S. officials familiar with the discussion. WSJ

- Microsoft plans thousands of job cuts, impacting less than 2.5% of workforce. Business Insider

- Republicans’ cash advantage just got a lot more powerful thanks to the Supreme Court — and the Democratic National Committee’s fundraising struggles just got a lot more concerning for their party. Democrats argue that the court’s Tuesday decision, which allows political parties to freely coordinate with candidates, will give the GOP the ability to offset Democratic candidates’ fundraising lead in battlegrounds. Politico

- The value of global M&A rose around 30% year-on-year to $2.6 trillion in the first half, on course to potentially pass 2021’s record haul. Companies struck 38 deals valued at $10 billion or more, the most ever in a six-month period. BBG

- US Challenger Job Cuts (Jun) 45.849K (Prev. 97.006K); cuts remain concentrated in tech, with AI continuing to reshape how companies think about headcount.

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks were mixed, in which bourses partially sustained the positive momentum from the tech-led gains on Wall St, where the S&P 500 and Nasdaq posted their best quarter in six years. The region also digested a slew of data, including the stronger-than-expected BoJ Tankan survey and numerous PMIs. ASX 200 was dragged lower by weakness in the consumer, financial, tech and telecom sectors, while sentiment was also not helped by a surprise contraction in Building Approvals data. Nikkei 225 rallied following the stronger-than-expected Tankan survey, which showed Large Manufacturing Sentiment was at the highest in 8 years, although the index gradually wiped out the majority of its gains amid intervention risks and as the data supported the case for the BoJ to continue normalising policy.

KOSPI pared opening gains and lingered in the red as SK Hynix and Samsung Electronics retreated. Shanghai Comp was underpinned on the 105th anniversary of the founding of the Communist Party of China, and as participants digested the latest RatingDog Manufacturing PMI, which remained in expansion territory, while Hong Kong markets were closed for a holiday.

Top Asian News

- Japanese top FX diplomat Mimura said they are in touch with US counterparts more than most imagine and that a US official made supportive remarks about FX action, while he also commented that recent intervention had meaning.

- BoJ official noted regarding the recent Tankan survey that most firms replied before the US-Iran peace deal on June 15th, so the impact of the deal is likely not reflected much in the Tankan outcome.

European bourses (STOXX 600 -0.1%) start Q3 on a softer footing, with Germany's DAX 40 (+0.4%) the only index printing modest gains; perhaps welcoming recent pension reform progress and the possible involvement of the Bundesbank. Final manufacturing PMI figures were broadly positive, with the majority of PMIs being revised higher. Commentary was relatively upbeat, with S&P stating that the sustained growth was accompanied by a welcome cooling of cost pressures. European sectors tilt to the negative side. Industrial Goods & Services (+0.5%), Technology (+0.5%) and Optimised Personal Care (+0.5%) are the top 3 sectors. To the downside lies Media (-1.7%), Consumer Products & Services (-1.5%) and Travel & Leisure (-0.1%).

Top European News

- French Presidential vote to be held on April 18th and May 2nd next year, with the official announcement expected on Wednesday, according to AFP citing sources.

- UK Labour MPs reportedly want Burnham to appoint McFadden as Chancellor, in order to block Miliband, Huffington Post reported citing sources.

FX

- Snapshot: G10s are mostly lower against the USD this morning, with clear underperformance in the Aussie, whilst the Kiwi fares a little better vs peers. USD/JPY continues to hold at elevated levels beyond the 162.50 mark, with further jawboning attempts seen overnight.

- DXY is firmer this morning and trades at the upper end of a 101.21-101.39 range (WTD peak at 101.43). The strength which comes amidst the markets’ continued hawkish shift at the Fed, seen following the last FOMC meeting. Markets also appear to be positioning for a hawkish commentary from Chair Warsh today, and then the NFP report on Thursday. On that note, Treasury Sec Bessent said he expects a strong jobs number, though clarified that he had not seen the report. Key releases today include: US ADP Employment, Challenge Job Cuts and ISM Manufacturing PMI.

- EUR and GBP have both been weighed on by the USD strength. The single currency has had a number of ECB members to digest, who are currently hosting the Sintra conference. Broadly speaking the remarks have been balanced, and with policymakers stressing data dependency heading into the July/September meetings. On the inflation front, today’s HICP release from the EZ saw the headline Y/Y cool from the prior (2.8% vs exp. 3%, prev. 3.2%). The Services figure also edged lower to 3.2% (prev. 3.5%). Some very mild pressure was seen in the EUR, and plays in favour of a hold in July. On the activity side of things, today’s Manufacturing PMI finals were subject to mild upward revisions, and the accompanying commentary was upbeat.

- JPY continues to remain in focus, with another jawboning attempt proving impotent. The latest attempt was by Top FX Diplomat who stated that Japan is in touch with US counterparts more than most imagine and that a US official made supportive remarks about FX action. This spurred some very mild pressure in the pair (05:30 BST / 00:30 EDT), falling from 162.79 to 162.56, before retracing about half of that move. A breach beyond the 163.00 mark could be difficult, given expectations that Japan may use the low-volume / holiday-thinned conditions on Friday (US Independence Day) to deliver effective intervention. Nonetheless, a hawkish Warsh and a strong NFP report on Thursday pose risk to the 163.00 level, which some have touted as the new “line in the sand”.

Fixed Income

- Global fixed income benchmarks are softer across the board, given Tuesday's post-settlement selloff. However, price action across the board has been range-bound, as markets look ahead to Fed Chair Warsh's first public appearance and updates from the US-Iran indirect Doha talks.

- Bunds (-18 ticks) have found support at the 127.00 handle, finding some stability after Tuesday's weakness, which was primarily driven by USTs. EZ inflation printed cooler than expected, with the headline figure at 2.8% Y/Y from 3.2% (exp. 3.0%) and ex-E, F, A & T dipping to 2.4% Y/Y from 2.6% (exp. 2.6%). Bunds did see some fleeting upside following the data, notching a new session high of 127.23 before falling back into the prior established daily range. ECB policymakers should find some comfort from the report, with some GC members starting to sound a bit more cautious on further rate hikes. On the supply front, a 2032 Bund auction was weak, with a poor b/c, though the average yield was less than the prior outing.

- USTs (-8+ ticks) oscillate in a narrow 109-18 to 109-23 band ahead of comments by Fed Chair Warsh at Sintra and the US jobs report on Thursday. Since his first remarks at the FOMC press conference, core PCE printed at 3.4% Y/Y, consumer confidence has surprised to the upside, and May payrolls printed strong (June payrolls due on Thursday). Given the backdrop, it would be hard for Warsh to soften his hawkish tone.

- OATs (-21 ticks) follow their European peers, but will come into greater focus as we near the Presidential elections in 2027. A date for the first round of elections has reportedly been set for April 18th, 2027, with a run-off set for May 2nd. The current President, Macron, cannot run in this election.

- Germany sells EUR 2.673bln vs exp. EUR 3.5bln 2.50% 2032 Bund: b/c 1.15x (prev. 2.4x), avg. yield 2.68% (prev. 2.8%), retention 23.6% (prev. 23.94%).

- UK sells GBP 1.25bln 0.125% 2031 I/L Treasury Gilt: b/c 4.26x (prev. 3.75x), real yield 0.933% (prev. 0.651%).

- Australia sells AUD 800mln 4.25% December 2035 bonds b/c 4.34, avg yield 4.748%

Commodities

- A contained start for the energy complex, but with modest pressure emerging across the European morning. As the benchmarks pullback from the highs in yesterday’s session and the brief, but within existing ranges, uptick seen in the US late-afternoon as tensions flared somewhat. Currently, the waiting game continues amid the Doha gathering, but there is a positive skew to current expectations as the US and Iran are expected to hold in-direct talks and after President Trump’s openness to extending deadlines over taking military action.

- As the morning progressed the downside extended with participants looking to the Doha indirect meeting, and indeed sources since suggest that has commenced, no move on that latest report. Kushner and Witkoff are reportedly not involved in the technical exchange.

- Action that pushed Brent to a USD 71.62/bbl base, printing a fresh WTD low and falling below the USD 71.93/bbl trough. The next leg higher/lower will potentially be determined by the readout and/or sources around the talks, before we look to possible comments from President Trump or others on the state of relations.

- Spot gold saw pressure overnight, moving below the USD 4k/oz handle once again. The yellow metal is currently trading at the bottom-end of a USD 3,960-4,018/oz range, with the trough approaching the WTD low at USD 3,942/oz range. The recent pressure has been attributed to the markets’ continued hawkish shift at the Fed, stronger USD and rising US yields. Price action for the remainder of the day will be dictated by key US data (ADP/ISM Manufacturing) and Fed Chair Warsh.

- Base metals are entirely in the red, following the subdued risk sentiment seen in Asia, which has filtered through into the London session. 3M LME Copper (-1.67%) has traded lower throughout the day, and currently holds at the bottom end of a USD 13,134.08-13,384/t range.

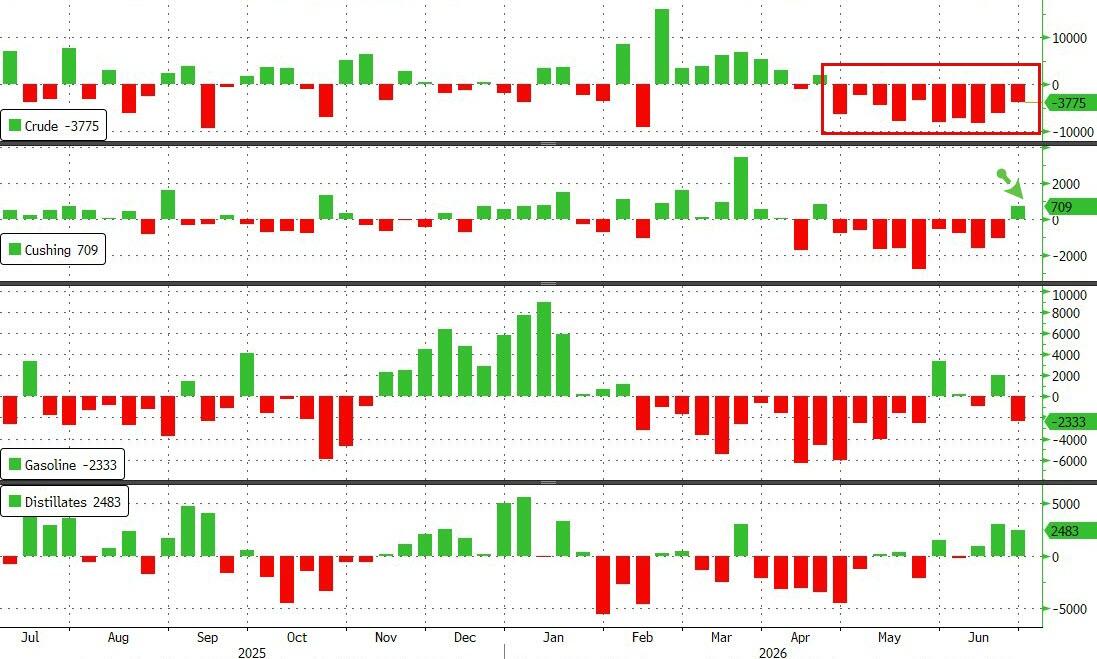

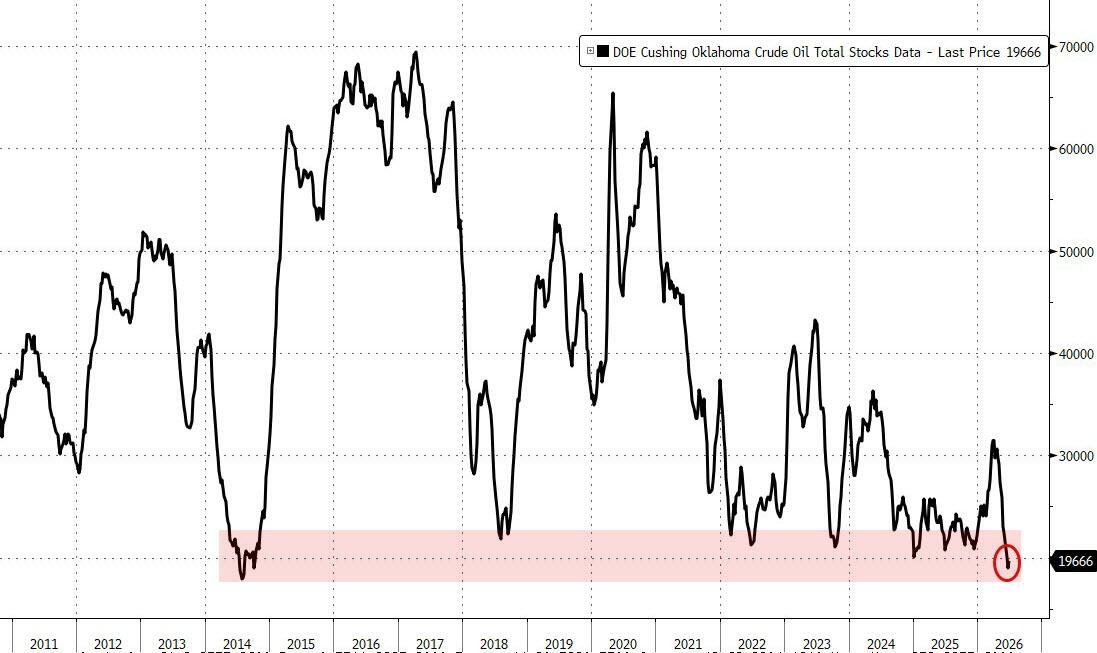

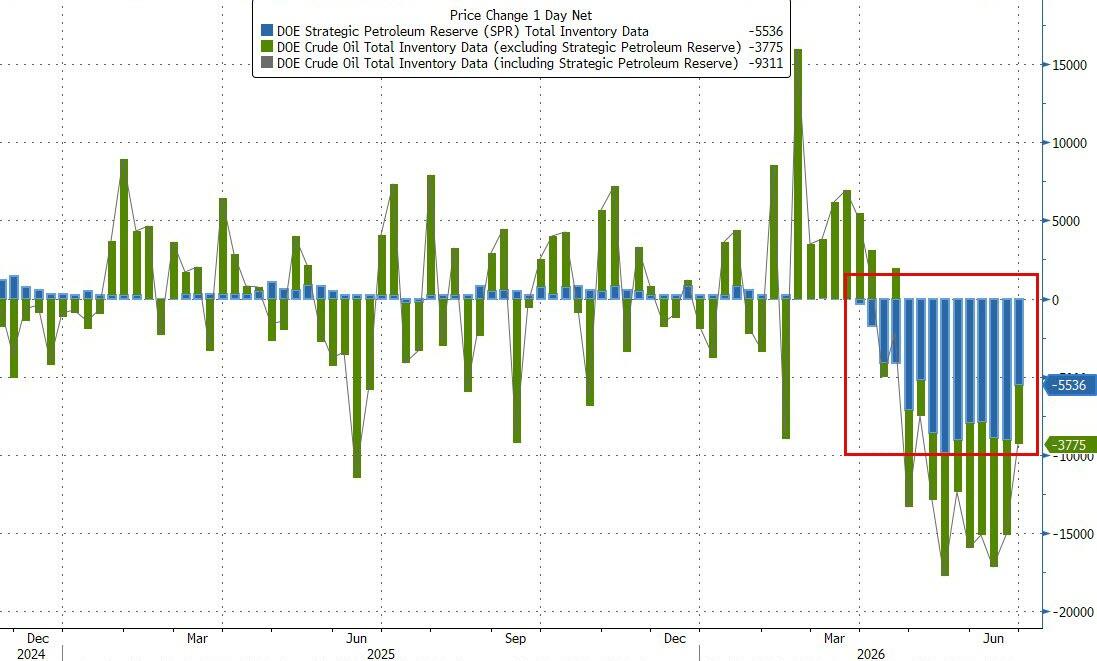

- US Private Inventory Data (bbls): Crude -6.1mln (exp. -4.1mln), Distillates +2.9mln (exp. -0.9mln), Gasoline -2.1mln (exp. -0.9mln), Cushing +0.5mln.

- Petrobras executive said they will cut diesel prices beginning July 1st.

Central Banks

- ECB's Nagel pushed back on a "insurance hike" narrative in an interview with Bloomberg TV. He added that inflation will stay high in 2026 and remain above target in 2027, while stressing data dependency and a meeting-by-meeting approach. On the future rate path, he kept options open for July and September. He finished by stating that the first round effects continue, which increases the chance of second round effects and that he is currently seeing pass-through of first round effects on wages.

- ECB's Wunsch told Econostream that the case for further tightening is receding and any surprise in EZ inflation before the July meeting is more likely to be on the downside. He added he would need stronger second-round effects to justify further tightening and that one hike could suffice if shock fades before significant second-round effects. More than one hike to depend on more persistence and stronger second-round effects.

- ECB's Demarco said the ECB should not rush into a further rate hike after the decline in oil prices, while he added the central bank can wait until next projections to decide if further hikes are needed, and that there are no signs of second-round effects, excessive wage pressures, or unanchored expectations.

Geopolitics

- Indirect US-Iran technical talks are reportedly underway in Doha, with Qatar and Pakistan acting as mediators. The sessions are to involve chief negotiators and specialist teams, sources suggest, however US envoy Witkoff and Kushner will not be attending the talks themselves.

- Iran is reportedly insisting on retaining control over the Strait of Hormuz, according to sources citing a senior Iranian official. Could see a recommence charging ships to transit from mid-August and are not going to discuss other points until Hormuz is agreed.

- US President Trump was briefed on all-out war options on Iran, but opted to stick with talks, while he told aides he's okay if talks go past the August 18th deadline, according to WSJ.

- US VP Vance said President Trump is ready to drop bombs again, while he added that they have two options, which are either to pursue a long-term agreement with Iran on the condition that it changes its behaviour, or consolidate the gains that they made. Furthermore, he said Trump asked them to use the memorandum of understanding to resupply the global economy with oil, then they will see how things develop, and they want permanent, verifiable commitments from Iran regarding its nuclear disarmament.

- US admin official said the US has not released any of the USD 6bln in Iranian frozen funds, and won’t until Tehran “performs”, according to NY Post's Doornbos.

- US official said ships are transiting the Strait of Hormuz at higher levels.

- Iran State Media said that a foreign container ship ran aground in the Strait of Hormuz after using a route which was undesignated by Iran.

- Oman presented a proposal regarding the future administration of the Strait of Hormuz to the US and other allies, while the proposal outlines a system for shipping companies to pay "service fees" for using the waterway, though sources differ on whether Oman is actively pushing for a fee-based structure, according to CNN citing sources.

- Qatar's PM and Foreign Minister met with US envoys Witkoff and Kushner, while they discussed the latest developments in the ongoing talks between the US and Iran, according to Qatar's Foreign Ministry.

- Israeli Broadcasting Authority cited a source that stated the start of the pilot phase in Lebanon has been postponed until a monitoring mechanism is reached between the Lebanese and Israeli armies.

- Israeli Defence Minister Katz said the IDF will remain in the security zones in Lebanon, Syria and Gaza.

- UKMTO said it received a report of an incident 76NM south of Yemen; the vessel being approached by multiple small craft but the crew reported safe.

- North Korean leader Kim pledged to deepen ties with China on shared socialist values and dispatched a congratulatory message to Chinese President Xi, on the Chinese Communist Party's founding anniversary, according to KCNA.

- Pakistan's air defence system shot down four rudimentary drones launched by Afghanistan's Taliban regime, while Pakistan's armed forces warned that continued provocation by the Taliban would be met with a befitting response that would cost them heavily.

US Event Calendar

- 7:00 am: Jun 26 MBA Mortgage Applications, prior 1%

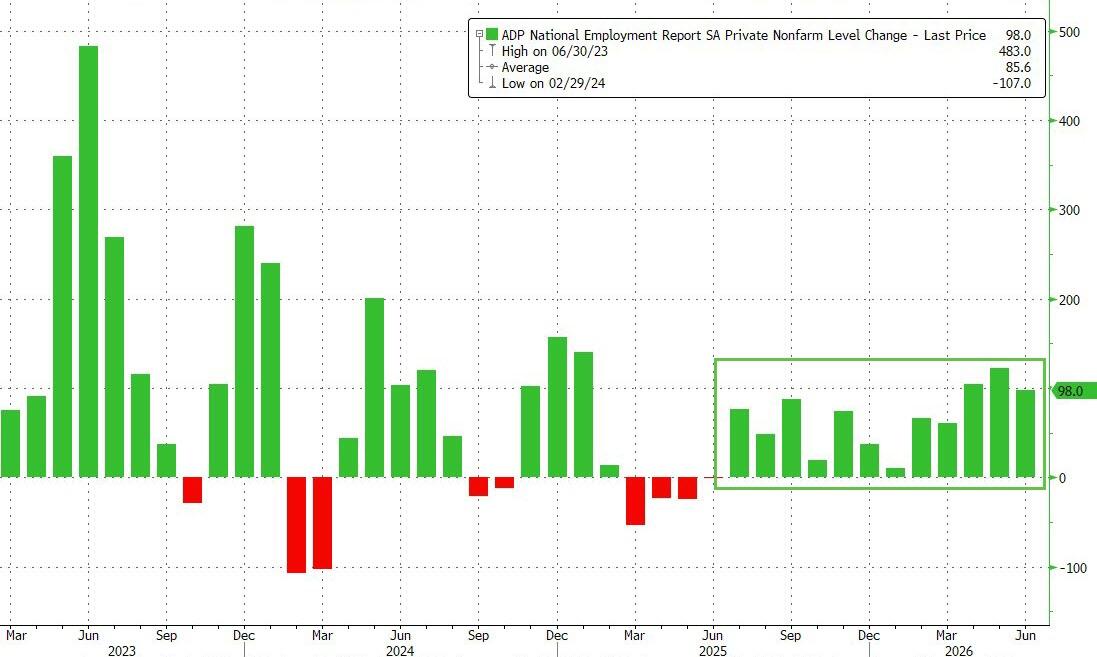

- 8:15 am: Jun ADP Employment Change, est. 120k, prior 122k

- 9:45 am: Jun F S&P Global US Manufacturing PMI, est. 55.7, prior 55.7

- 10:00 am: Jun ISM Manufacturing, est. 53.85, prior 54

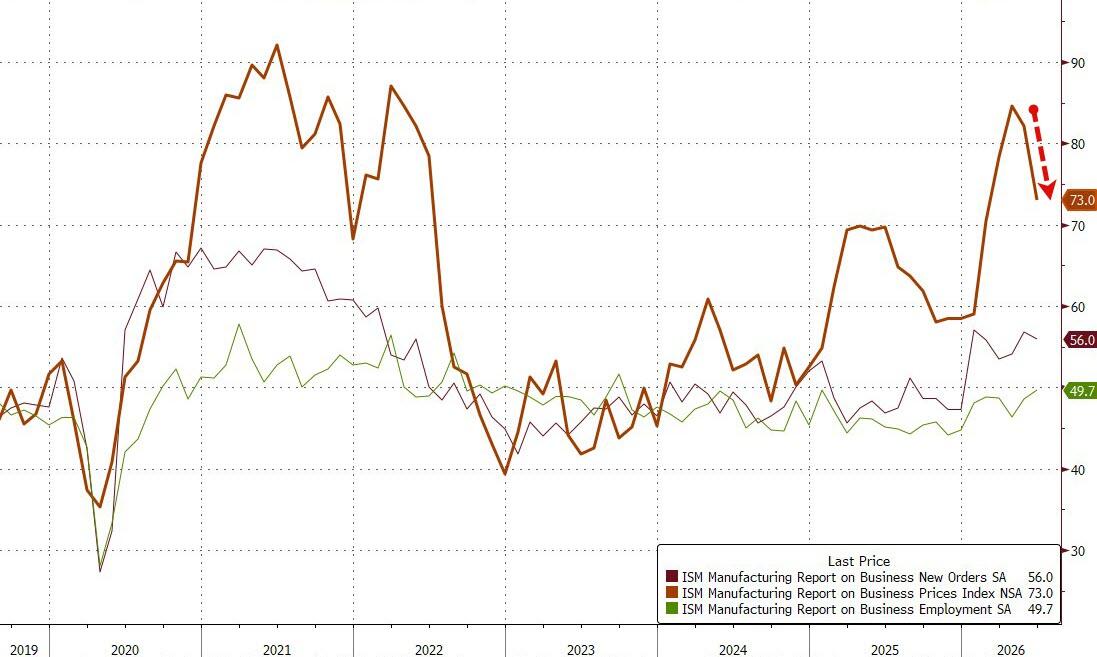

- 10:00 am: Jun ISM Prices Paid, est. 77.5, prior 82.1

- 10:00 am: May Construction Spending MoM, est. 0.1%, prior 0.4%

Central Banks

- 9:00 am: ECB’s Lagarde, Fed’s Warsh, BOE’s Bailey, BOC’s Macklem

- 9:00 am: Fed’s Warsh Appears on Panel at ECB Forum

DB's Jim Reid concludes the overnight wrap

There must be a lot of illness going round our floor today — looking at the team diary, an awful lot of people seem to be seeing a doctor. In fact, at 5pm sharp, it looks like everyone’s booked in with Dr Congo… let’s hope we all get a positive result.

As it’s the start of the new quarter, Henry will shortly release our regular performance review for Q2 and indeed H1. The main headline was the signing of the interim US-Iran deal, which meant Brent crude oil prices (-38.4%) saw their biggest quarterly decline since the start of the pandemic in Q1 2020. So that meant stagflation fears receded, supporting bonds and equities across the board. In fact, the S&P 500 saw its best quarter since the post-pandemic rebound in Q2 2020, with a +15.2% gain in total return terms. That included an exceptional performance for chip stocks, with the Philly semiconductor (+88.0%) posting its best quarter since the index started in the early 1990s. See the full report in your inboxes shortly.

Risk assets largely finished Q2 on a strong footing yesterday, with the S&P 500 (+0.79%) gaining for a second consecutive day. The biggest factor was the recovery in tech stocks, with the Mag 7 (+1.30%) up for a third consecutive day, whilst the Philly semiconductor index (+3.92%) posted another large gain. The rally was somewhat narrow with a majority of S&P 500 constituents lower on the day and just 8 of the 25 industry groups gaining. This left the equal-weighted S&P 500 -0.12% lower, while the small cap Russell 2000 underperformed (+0.46%) its large cap peers.

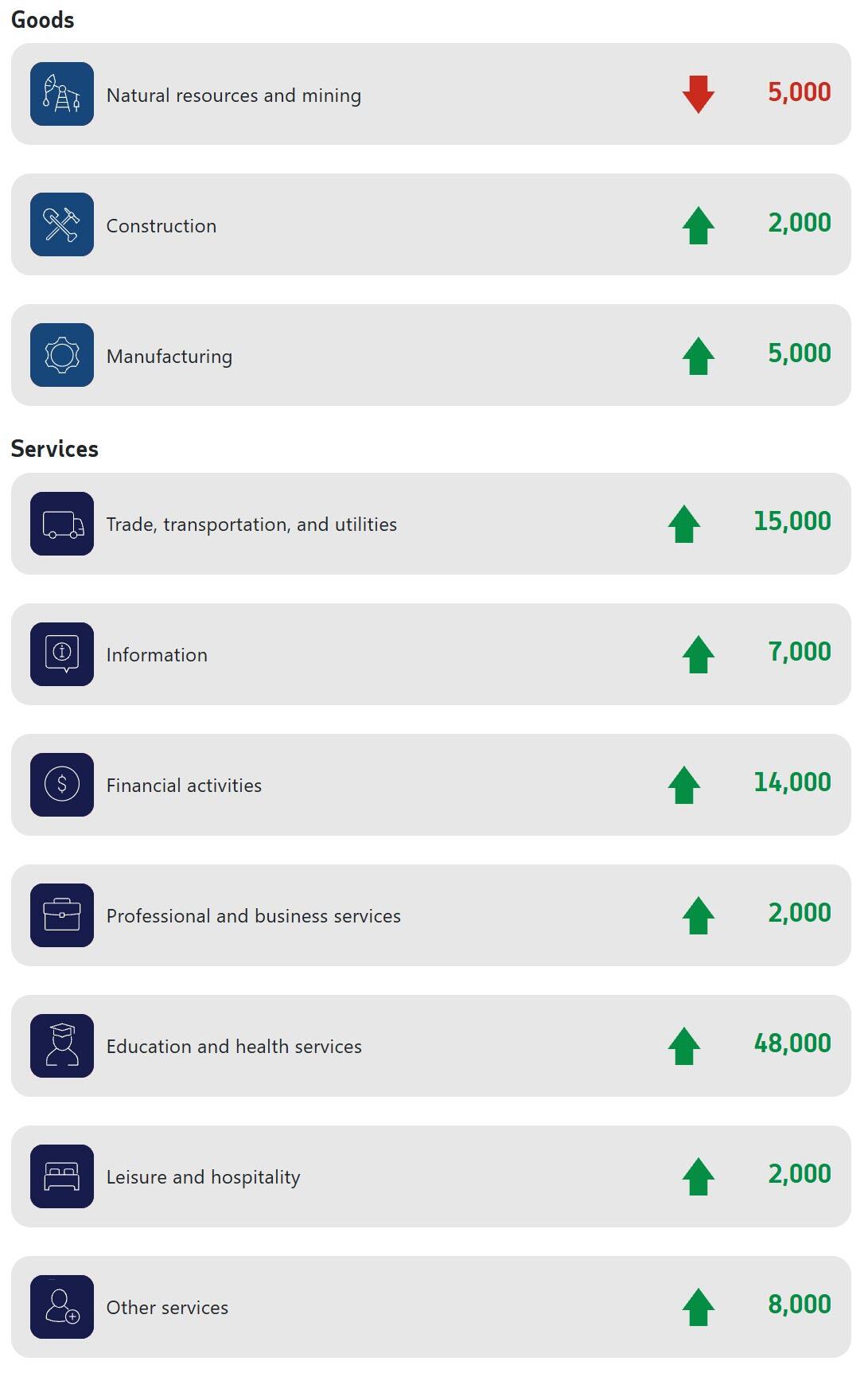

US data was mixed yesterday as strong job opening numbers were matched with weak housing and sentiment data. The JOLTS report for May added to the picture of labour market resilience from other recent releases. Job openings surprised on the upside, with 7.594m openings in May (vs. 7.296m expected). So that meant that the ratio of job openings per unemployed individuals reached 1.039, which takes it to the highest reading since January 2025. Moreover, the quits rate of those voluntarily leaving their jobs (a good barometer for tightness in the labour market) held steady at 1.9%. And yet the Conference Board’s consumer confidence reading missed expectations, coming in at 91.2 (vs. 94.4 expected), with the present labour market sentiment the weakest since 2021. Moreover, the overall present situation indicator fell to 116.4 (vs. 123.0 expected), marking its lowest level since February 2021 when the economy was still coming out of the pandemic. Consumer sentiment/confidence numbers have long decoupled from economic growth so we can't read too much into it, but the data is still striking. On housing, the FHFA House Price index showed a month-on-month decline in house prices (-0.1% vs +0.2% expected), with year-over-year home price appreciation now near its lowest levels since 2012.

However, the market keyed in on the strong job openings number and hawkish comments from Cleveland Fed President Hammack shortly after their release. She said in a CNBC interview that the US may “need higher interest rates to bring inflation back down to target”, and when asked about a July hike, said she was keeping an open mind at every meeting. So that raised speculation about a rate hike in just 4 weeks’ time, and market pricing for a July hike ticked up a bit to 34% by the close, up from 32% the previous day. Stand by for both Warsh and Lagarde speaking at Sintra today.

Ahead of that, the hawkish newsflow led to a fresh selloff for US Treasuries, with the 2yr Treasury yield (+6.8bps) rising to 4.17%, whilst the 10yr yield (+9.1bps) hit 4.465%. There was a more muted reaction for European government bonds as yields on 10yr bunds (+0.3bps), OATs (+1.3bps) and BTPs (+4.8bps) all moved higher. This followed comparatively dovish European newsflow, with the flash CPI prints surprising on the downside in several member states. So the German print fell more than expected to +2.4% on the EU-harmonised measure (vs. +2.5% expected), whilst the French print also fell more than expected to +2.0% (vs. +2.3% expected).

So that raised hopes that today’s Euro Area-wide print might surprise on the softer side, and investors also dialled back expectations for ECB rate hikes this year, with just 23bps priced by the December meeting at the close, down from 27bps the previous day. Here in the UK however, 10yr gilt yields (+4.1bps) rose by more than elsewhere, which came as BoE Governor Bailey warned that inflation could still rise later this year. Otherwise in Europe, equities advanced across the board, with the STOXX 600 up +0.88% to a new all-time high. The move was clear across the continent, with gains for the DAX (+1.50%), the CAC 40 (+0.44%) and the FTSE MIB (+1.01%) as well.

Alongside the lower inflation prints, sentiment was also supported by oil prices holding steady, with Brent crude (-0.31%) down slightly on the day. This came as Bloomberg reported that US officials held positive discussions with GCC leaders in Qatar on Tuesday. There was further reporting from the Wall Street Journal overnight that President Trump had been briefed on potential war options but was opting to stay in talks and that he told aides that he was ok with talks continuing past the initial August 18th deadline. The dovish mood from the White House continues as the President seems reticent to restart the kinetic action and risk higher energy prices ahead of the November midterms.

Asian equity markets have started H2 on a mixed footing this morning. The KOSPI (-0.70%) is leading regional declines, coming off one of its strongest quarterly runs in recent years. By contrast, improved manufacturing activity in Japan and China is supporting gains in Tokyo and mainland markets. The Nikkei (+0.63%) is moving higher, alongside both the CSI (+0.44%) and the Shanghai Composite (+1.08%), while Hong Kong markets are closed for a public holiday. S&P 500 (-0.23%) and Nasdaq (-0.24%) futures are both edging lower.

Early data suggested that China’s manufacturing activity moderated slightly in June relative to May, although robust export performance helped keep overall activity in expansionary territory. The RatingDog Manufacturing PMI edged down to 51.7 from 51.8, a three-month low, but still capped the strongest quarterly performance for the sector since Q4 2020.

In South Korea, exports surged by +70.9% year-on-year in June, accelerating from +53.4% in May and comfortably exceeding expectations. The increase was largely driven by strong semiconductor demand amid the global AI investment boom, reinforcing the Bank of Korea’s increasingly hawkish stance ahead of its July 16 decision. Separately, while factory activity expanded for a seventh consecutive month, the pace of growth eased slightly, reflecting softer export demand at the margin.

Elsewhere, the yen weakened to its lowest level against the dollar since 1986 overnight, currently at 162.72 (-0.10%) and fuelling speculation that Tokyo may be nearing direct intervention.

To the day ahead now, data releases include the US June ISM manufacturing index, ADP report, and May construction spending, along with the Euro Area flash CPI print for June. Central bank speakers include the Fed’s Warsh, the ECB’s Lagarde, Vujcic, Cipollone and Lane, the BoE’s Bailey, and the BoC’s Macklem.

Tyler Durden

Wed, 07/01/2026 - 08:35

via Atlantic Council

via Atlantic Council

Vadym Iermolaiev, via X

Vadym Iermolaiev, via X

Source: White House/Getty Images

Source: White House/Getty Images

File image: UBN

File image: UBN

Recent comments