Futures Slide After Google Earnings, Oil & Bond Yields Jump On Houthi Escalation

US equity futures are lower as WTI breaches $90/bbl and Brent approaches $100/bbl (Houthi escalation in the Red Sea as two Saudi tankers were struck), pushing bond yields higher with longer-dated yields seen making new highs, globally. But, Alphabet's underwhelming results - while dragging down Mag7 names - are boosting Semis / AI (CapEx spend) which may mean the market is returning to its barbell of longs in AI / Semis plus Energy versus shorts in Rate-sensitives.

* * *

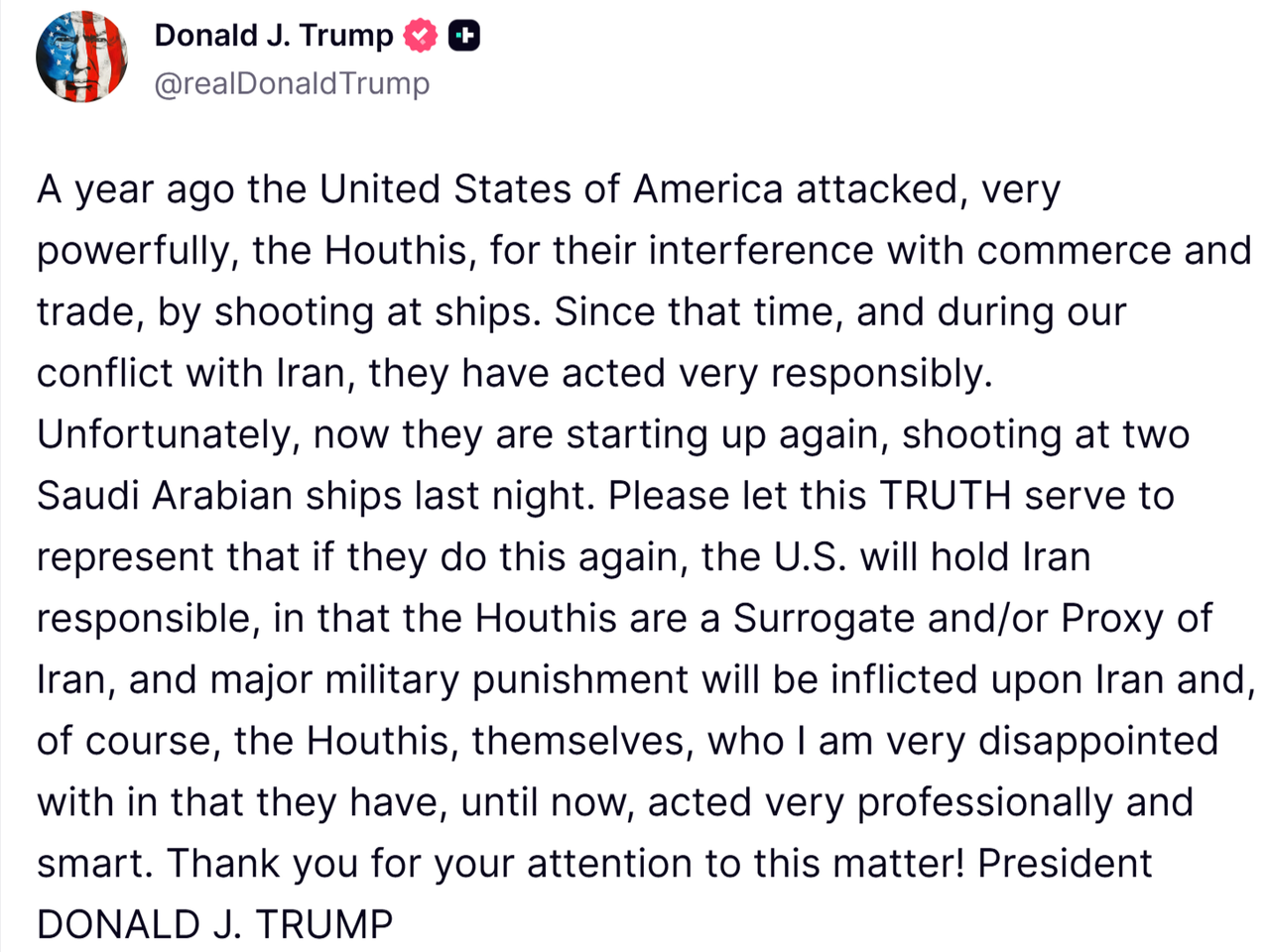

Overnight saw oil prices extend their recent resurgence with WTI crude topping $90/bbl. The Iran-aligned Houthis said they targeted two oil tankers in the Red Sea, potentially opening up another front in the war.

US forces struck Iranian military targets including maritime capabilities, missile and drone storage facilities, coastal surveillance sites, and air defense assets, Centcom said.

Commodities are led by the Energy complex; Base is higher, Precious is lower, and Ags mixed.

Pre-mkt, US yields are up 3-4bps across the curve with USD flat.

The surge in crude prices has dragged rate-hike odds higher (July very much back on the table)...

In Equities, Mag7 is weaker with all 7 names lower with GOOGL, TXN, TSLA, and IBM all lower following earnings.

Semis / Memory are bid. Defensives and Energy are higher with Cyclicals mostly lower ex-Industrials which are being boosted as part of the AI theme.

Utils are bid with AI outweighing higher yields.

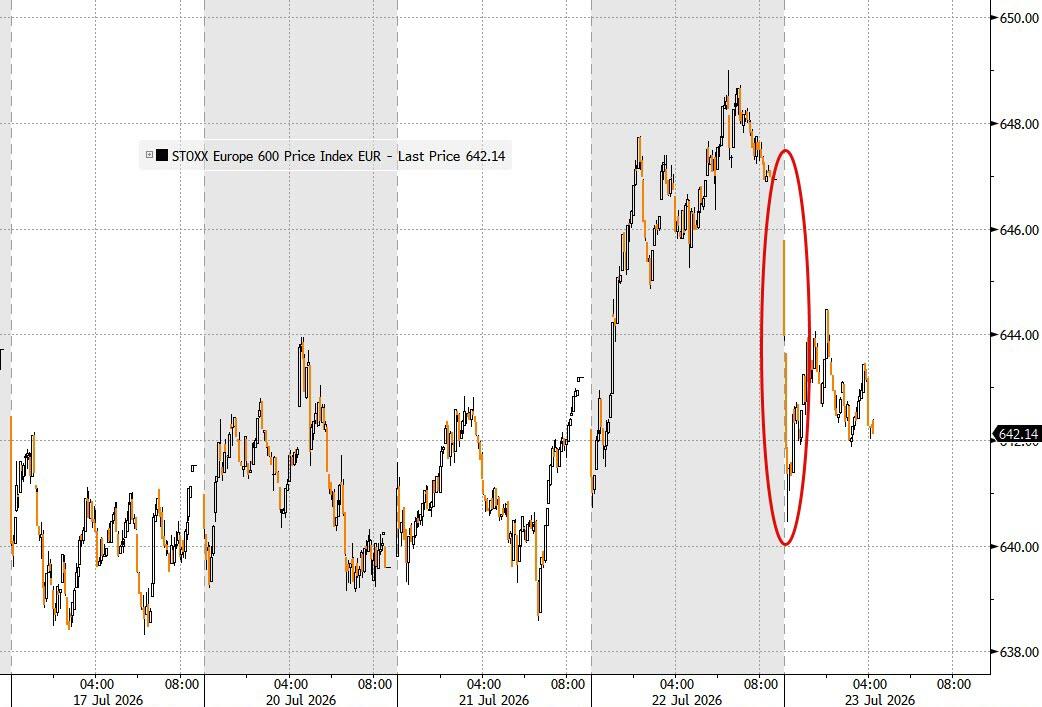

European stocks fall as technology shares are dragged lower by STMicroelectronics, which slumped 17% after disappointing with its sales outlook.

Elsewhere, Nestle posted its biggest intraday drop since 2020.

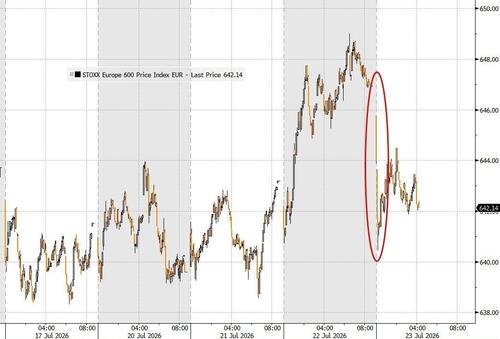

Stoxx 600 falls 0.6% to 642.78 with 405 members down, 184 up, and 11 unchanged.

Asian shares rose as sentiment improved on expectations that regional tech hardware companies will benefit from Alphabet’s plans for more AI spending.

The MSCI Asia Pacific Index climbed as much as 1.4%, led by Samsung and SK Hynix.

A Bloomberg gauge of Asian chip shares advanced as much as 1.7%, extending its gains for a third session after tipping into a bear market last week.

Gains in artificial intelligence and semiconductor shares pushed the benchmarks in South Korea and Japan higher.

Thursday’s moves across Asian markets reflect investors’ willingness to prioritize AI enthusiasm, earnings and capital spending plans in the short-term over geopolitical tensions that linger, primarily from the Middle East.

Top Overnight News

-

The ECB is expected to maintain interest rates at 2.25% today, buying time to assess the fallout from renewed Middle East hostilities.

-

A rally in Indonesian stocks put the nation’s benchmark index on track for a bull market, helped by a rotation into market laggards as well as a recent credit-rating announcement.

-

The oil price has risen above $98 a barrel for the first time since early June after Iran-backed Houthi militants said they had attacked two Saudi Arabian tankers in the Red Sea.

-

The U.S. is surging forces, medics and weaponry to the Middle East to give President Trump more muscular military options as he considers expanding the conflict against Iran, according to people familiar with the matter.

-

The U.S. military used a B-1 long-range bomber on Tuesday to strike Islamic Revolutionary Guard Corps targets in Iran, U.S. officials said. It was the first time the U.S. conducted a B-1 mission since fighting with Iran resumed 12 days ago.

-

Russia is set to receive a shipment of fuel from India, as Moscow is forced to import petrol after Ukrainian drone attacks destroyed parts of its major refineries.

-

A rare surge in Latin American currencies is squeezing exporters by reducing the value of US dollar-denominated revenue. Coffee growers, banana producers and manufacturers face shrinking margins despite stronger investor confidence.

-

Allies of Donald Trump have discussed whether an external review of the Silicon Valley Bank collapse might justify removing Fed Governor Michael Barr over his role overseeing bank supervision at the time, people familiar said.

-

Private equity takeovers of software groups are at a turning point as investors hunt for bargains among companies at risk of being disrupted by AI.

A more detailed look at global markets courtesy of Newsquawk

EQUITIES

- European bourses (STOXX 600 -0.6%) started Thursday's busy earnings day in the red, with higher energy prices and disappointing earnings weighing on indices. On the geopolitical front, the US and Iran exchanged strikes for the 12th consecutive night, while US President Trump said Iran is getting hit so hard and that they want to make a deal. Additionally, Yemeni Houthis targeted two Saudi oil tankers in the Red Sea, while reports noted that at least 9 ships have stopped passing through Bab al-Mandeb, following the blockade on Saudi ports by Houthis.

- Sectors highlight the negative bias. Energy (+1.6%) tops the sector pile, with Real Estate (+0.8%) also printing decent gains. Food, Beverages & Tobacco (-2.9%) is the sector laggard, following Nestle earnings in which RIG missed estimates. Consumer Products & Services (-2.0%) and Travel & Leisure (-1.5%) rounds out the key underperformers.

- A lot of big European earnings this morning, with focus concentrated on STMicroelectronics figures. Its Q2 metrics beat estimates; however, its guidance and commentary have driven the biggest drop in shares since October 2025 (-13.8%). The Co. guided Q3 net revenue of "about" USD 3.7bln, which missed analysts' expectations, and raised its revenue ambition for data centres due to continued strong demand. Citi analysts say that shares already reflect a recovery across its end markets and acceleration in revenue from data centres. Additionally, analysts say that shares may struggle in the near-term.

- US equity futures are softer across the board, with downside in tech-heavy NQ weighed on by STMicroelectronics earnings. Mag-7 earnings kicked off yesterday after the bell, with Alphabet and Tesla reporting Q2 metrics. For GOOGL (-3.9% pre-market), it sharply raised its AI capex forecast (which benefited Asia-Pac chip names overnight). For TSLA (-5.6% pre-market), Q2 figures disappointed, as adj. EPS missed estimates.

- Alphabet Inc. (GOOGL) Q2 2026 (USD): EPS 9.11 (exp. 2.88), Revenue 119.8bln (exp. 117.00bln), Operating income 40.77bln (exp. 40.55bln), Capex 44.92bln (exp. 44.15bln). Raises FY26 capex view to USD 195bln-205bln (prev. 180bln-190bln).

- Tesla Inc. (TSLA) Q2 2026 (USD): Adj. EPS 0.33 (exp. 0.52), Revenue 28.2bln (exp. 25.99bln), Gross margin 16.8% (exp. 19.4%), Automotive revenue 20.52bln (exp. 18.68bln).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed after initial losses for the Greenback were reversed as energy prices continue to determine bias. Action which has benefitted energy exporters CAD and NOK, the sole currencies firmer against the Buck.

- USD erased earlier modest losses as energy lifted to session highs with the Brent Sept’26 contract approaching levels not seen since May. Geopolitics remains constructive for the Buck, and there are no signs of immediate de-escalation - focus on Houthi attacks on Saudi Arabian vessels alongside flows through Bab al-Mandeb. Elsewhere, US earnings after the NY close were received poorly, with Google and Tesla slipping between 3-5% premarket, hitting indices and potentially increasing appetite for the Buck’s haven status. DXY rose from beneath the 21DMA @101, to mark a high at recent resistance near 101.20/1.

- EUR is lacklustre against the Buck ahead of the ECB meeting, where just 4bps of tightening is implied by markets. The Governing Council is likely to convey a hawkish message after the recent energy pressures. Should the bank stand pat on rates as analysts/markets expect, focus will be on guidance which could spur a move above two fully priced 25bp hikes by year-end. EUR/USD is well off highs made early in the domestic session, though found support towards 1.14. ING says this morning its near-term bias is tilted to the downside, noting if Gulf newsflow lacks signs of de-escalation, it looks for the pair to slip towards 1.1380 in the coming days.

- AUD is resilient against the Buck after strong jobs numbers overnight. The data saw headline Employment Change smash estimates at 76.3k (exp. 15k), and the Unemployment Rate remained at 4.4% despite higher Participation. It appears NZD is used as a funder to express AUD hawkishness given USD swings on geopolitics, with AUD/NZD +0.4%, while AUD/USD is flat.

- TRY looks to the CBRT meeting, where analysts have shifted calls for easing in exchange for a hold amid the recent energy pressures. Turkish inflation eased to 32.1% Y/Y in June from 32.6% in May, as energy prices fell following the US-Iran MoU, which has since broken down. Despite the softer print, most analysts still forecast year-end inflation above the CBRT’s 26% target (incl. GS, MUFG at 30%), suggesting rates will remain higher for longer, particularly after the recent resurgence in Gulf tensions. Banks mostly expect the bank to stand pat on its key rate; HSBC said it could instead adjust its funding policy, lowering the average funding cost for commercial banks without formally changing the policy rate; JPMorgan expects the CBRT to resume one-week repo auctions, while Garanti BBVA, which recently shifted its call, expects a hold, but does not rule out easing. USD/TRY is lacklustre ahead of the decision.

FIXED INCOME

- A bearish start for fixed income as energy climbed overnight and into the European morning after the 12th consecutive evening of action by the US in the Middle East. Action that has taken Brent above USD 98/bbl and weighed on global yields.

- Overnight, JGBs reacted to the above and also a Reuters source report from Wednesday that the BoJ is alert to inflationary risks that could result in tightening taking place faster than the market is pricing. JGBs down to a 127.04 base, lower by just over 20 ticks.

- USTs hold at a 108-09 low, with downside of just a few ticks on the day. Today’s docket features weekly claims (initial claims coincide with the BLS survey window), before a 10yr TIPS auction and the latest Chicago Fed.

- Bunds under pressure as above, down to a 124.17 base at worst but currently holding around 15 ticks clear of that but still lower by over 20 ticks on the day. Action that has pushed the 10yr yield to a 3.2% peak, just above May’s best to a new YTD high, a dynamic that is also reflected at the short-end, where the 2yr has notched a new YTD peak of 2.88%.

- Energy has driven much of this, but the short-end is also likely being spurred further by the associated implications for the ECB. While a hold is the base case today, the accompanying guidance may well be more hawkish and explicit than the usual no-signal, data-dependent and meeting-by-meeting approach we have become accustomed to. Note, given the moves in recent days, more hawkish guidance may only spark a modest hawkish reaction, while a reiteration of the above non-committal language could see a relatively more pronounced dovish move. However, again, any such reaction would likely be limited in nature as geopolitics and, by extension, energy dictate the narrative.

- Gilts opened lower and underperformed, in the typical action seen when energy is bid. Opened with losses of 15 ticks and then slipped to an 86.07 base, just above the 86.03 low from April but some way clear of May’s 84.98 contract trough. No real reaction to commentary from UK Chancellor Healey this morning, who stuck with familiar language. The day ahead for UK rates may take direction from the ECB as outlined above, as any hawkish nod from Europe would be in contrast to the on hold for the foreseeable narrative which remains around the BoE, despite the dissenters and clearly contrasting views on Threadneedle Street.

COMMODITIES

- Middle Eastern geopolitics continues to dominate price action, with the US and Iran exchanging strikes for the 12th consecutive night, whilst US President Trump said Iran is getting hit so hard and that they want to make a deal. He added that Iran will be ready very soon but is not ready for a deal yet. Hostilities across the region have also expanded, as Yemeni Houthis targeted two Saudi oil tankers in the Red Sea, while reports noted that at least 9 ships have stopped passing through Bab al-Mandeb, following the blockade on Saudi ports by Houthis. On that note, Pakistan's Foreign Ministry, on the Yemeni Houthi threat, said, "If our ships are attacked, it will be treated as an attack on Pakistan, and we will retaliate”. As a reminder, Pakistan and Saudi Arabia signed a mutual defence pact in September 2025. The treaty states that an attack on one nation is considered an attack on both. If the Houthis launch severe ballistic missile strikes on Saudi territory or fully disrupt its vital energy exports, Riyadh could formally trigger this pact. This could further complicate the picture as Pakistan is the main mediator in US-Iran talks. Further on this front, Pakistani PM Sharif held a call with Saudi Crown Prince MBS; the two condemned the Houthi militia’s attacks against Saudi oil tankers in the Red Sea; and reaffirmed Pakistan's "complete solidarity" with Saudi Arabia. Elsewhere, reports noted the sound of an explosion was heard in Qatar and Jordan, whilst an explosion was also heard in Iran around Qeshm city near Konarak. Elsewhere in geopolitics, US Secretary of State Rubio said he had a good and frank conversation with the Russian Foreign Minister; the US is prepared to take a constructive role to end the war in Ukraine. Meanwhile, EU Ambassadors have reached a political agreement on the 21st sanctions package against Russia, according to diplomats; additionally, the bloc is to freeze the oil price cap for a 12-month period.

- WTI and Brent futures at session highs. WTI Sep’26 trades beyond the USD 90/bbl mark, currently at the top end of its USD 87.32-90.35/bbl range. Brent Sep’26 resides near USD 98.50/bbl in a USD 94.89-98.75/bbl range. Dutch TTF prices have waned after hitting resistance near EUR 64/MWh before dipping sub-62.50/MWh. This morning, sources reported that buyers of LNG from Qatar and the UAE are seeking lower prices and stronger supply guarantees as risks to shipments through the Strait of Hormuz increase.

- Precious metals are softer as rising oil prices once again hit by the rising oil prices. Spot gold trades in a USD 4,087-4,141/oz range, within yesterday’s USD 4,076-4,166/oz range. Spot silver briefly dipped under yesterday’s 58.73/oz low to currently trade towards the bottom end of a USD 58.66-60.07/oz range.

- Base metals are mostly lower amid the inflationary impact of higher oil prices. 3M LME copper trades towards the lower end of a USD 13,709.00-13,873.70/t range.

- Buyers of LNG from Qatar and the UAE are seeking lower prices and stronger supply guarantees as risks to shipments through the Strait of Hormuz increase, according to sources.

- Kazakhstan's daily oil production fell after loading operations were suspended at the CPC export terminal on the Black Sea, sources say, output down 21% on Wednesday vs July average

TRADE/TARIFFS

- China's MOFCOM said China and the US are working towards the tariff cut plan; to maintain close communication.

- UAE Foreign Trade Minister said imports of high-end US AI chips expected soon, Bloomberg reported.

NOTABLE EUROPEAN HEADLINES

- The UK PM announced that pubs, clubs and live music venues are set to receive a 20% cut to their business rates bills, saving the typical pub an estimated GBP 1,100/yr.

- UK Chancellor Healey said he is as concerned about the cost of business as the cost of living.

NOTABLE US HEADLINES

- US President Trump said the government will face a shutdown in September.

- Some Trump admin officials and allies have privately discussed whether an external review of the 2023 failure of Silicon Valley Bank could provide a legal basis to remove Fed Governor Barr, according to Bloomberg.

- US is investigating Chinese AI firm Moonshot over chip access, with the BIS probing if the Co. used US chips for model training, according to The Information.

- Trump admin is reportedly divided about restricting Chinese AI models, with the White House mulling preventing Chinese labs from distilling US models, and Commerce Department favours incentivising US companies to develop open models to counter China

GEOPOLITICS

MIDDLE EAST

- US Secretary of State Rubio said Iran was intending to double missile stockpile and that it looks like Iran is not ready to make a deal. He added that the price on Iran will get higher every night until they come to their senses but that Iran is begging to reach a deal.

- US CENTCOM said the US completed the 12th consecutive night of strikes against Iran, in which the US struck Iranian military targets including maritime capabilities, missile and drone storage facilities, surveillance sites and defence assets.

- US military has started using B-1 long-range bombers in its strikes against Iran, according to i24's Stein citing a source that stated the first strike using the bomber was conducted on Tuesday.

- A senior US official said negotiations continue but the decisive moment for expanding hostilities is rapidly approaching, N12 reported.

- There were several explosions heard in Kuwait, Qatar and Jordan while sirens were sounded in Bahrain. In Iran, explosions were heard in Bushehr, Bandar Mahshahr, Sirik, Konarak City and Ramshir. Additionally, Iranian media reported that a power station was hit by a missile near the Bushehr nuclear power plant in the south of the country, according to Sky News Arabia.

- IRGC said one of three offending ships attempting to pass the Strait of Hormuz caught fire and the other two quickly turned back, while it also targeted US bases in Jordan, and declared the Strait of Hormuz closed. Additionally, the IRGC said it targeted US military in Kuwait's Al-Adiri camp and Ali Al-Salem Airbase.

- Yemen's Houthis announced they targeted two Saudi oil tankers in the Red Sea. In other reports, at least 9 ships have stopped passing through Bab al-Mandeb, following the blockade on Saudi ports by Houthis.

- Two Chinese supertankers carrying Saudi crude are heading to Bab al-Mandeb, according to reports citing data.

- Pakistani PM Sharif held a call with Saudi Crown Prince MBS. The two condemned the Houthi militia’s attacks against Saudi oil tankers in the Red Sea and reaffirmed Pakistan's "complete solidarity" with Saudi Arabia.

- Pakistan's Foreign Minister, on US-Iran talks, said they can not confirm 10-15 days or anything because these are confidential communications but they have not lost hope even during the darkest days of this escalation cycle.

- Pakistan's Foreign Ministry, on the Yemeni Houthi threat, said that if Pakistani ships are attacked, it will be treated as an attack on Pakistan and will retaliate.

- UKMTO said it received a report of an incident 70NM of Al-Shuqaiq, Saudi Arabia, with a tanker reported to have been struck by an unknown projectile, causing a fire on board.

- Oman’s Foreign Ministry said it is working with Saudi Arabia and Yemeni parties and the UN special envoy to resume the political process aimed at achieving regional security and stability.

- The US is on course to get no new military spending before the election and they are warning it could be a huge problem for them amidst the war with Iran, according to Semafor.

RUSSIA-UKRAINE

- US Secretary of State Rubio said he had a good and frank conversation with the Russian Foreign Minister and the US is prepared to take a constructive role to end the war in Ukraine.

- Russia's Foreign Minister Lavrov confirmed that Russia is prepared to resolve the conflict in Ukraine through political and diplomatic means, according to the Russian Foreign Ministry.

- EU Ambassadors have reached a political agreement on the 21st sanctions package against Russian, according to diplomats. Additionally, to freeze the oil price cap for a 12 month period.

OTHER

- China is conducting live fire, military drills in some areas of the Taiwan Strait on Thursday and Friday.

CRYPTO

- Bitcoin continues to pare back Tuesday's gains but remains firmly above the USD 65k mark.

APAC TRADE

- APAC stocks were predominantly in the green as semiconductor strength helped the region shrug off the lacklustre lead from Wall Street and the widening geopolitical escalation in the Middle East.

- ASX 200 was lifted amid outperformance in the commodity-related and materials sectors, while sentiment was also helped by strong jobs data.

- Nikkei 225 rallied at the open but is well off today's best levels amid higher oil prices and after hitting resistance around the 67,000 level.

- KOSPI remained driven by semiconductor advances with both Samsung Electronics and SK Hynix in the green, while chaebols dominated the list of biggest gainers and participants also digested stronger-than-expected South Korean GDP data.

- Hang Seng and Shanghai Comp were mixed, with Hong Kong led higher by strength in mining names, while the mainland was lacklustre as trade-related frictions lingered, with the US investigating Chinese AI firm Moonshot over chip access and whether the Co. used US chips for model training.

Deutsche Bank's Jim Reid concludes the overnight wrap

Inflation has remained top of the agenda for markets this morning, with Brent crude moving up to almost $96/bbl overnight as the Middle East escalation continues. Indeed, the strikes between the US and Iran show no sign of easing, and the Houthis said they targeted two oil tankers in the Red Sea yesterday, raising fears that the conflict is widening. So that’s pushed oil prices up to a 7-week high, and has also fuelled speculation about more rate hikes. For instance, futures are currently pricing in a 36% probability of a Fed rate hike as soon as next week, and bond yields jumped as well, with the US 30yr real yield (+0.4bps) closing at a post-2008 high of 2.93% yesterday. So it was a tough backdrop, and equities struggled to gain traction too, with the S&P 500 down -0.14% yesterday, whilst futures are down another -0.13% this morning following earnings from Alphabet and Tesla.

We’ll start with the geopolitics, as the US-Iran conflict has shown no sign of easing, and there’s still no indication of any emerging peace deal either. In fact, President Trump posted yesterday that if Iran shoots at a ship in the Strait of Hormuz, then the US would “bomb and destroy ONE BRIDGE OR POWER PLANT”. And shortly after, Trump said in person that Iran would pay a big price after US troops were killed, whilst Iran’s foreign minister Abbas Araghchi posted that aggression against Iran “will compel a powerful and decisive response”, and that those “who contribute to such aggression, whatever the kind of support, will also be considered as legitimate targets”. Overnight, US Central Command confirmed that they’d completed another round of strikes against Iran, whilst oil markets have come under fresh pressure given the news about the Houthis targeting two oil tankers in the Red Sea. So that’s raised fresh supply fears given Saudi Arabia has redirected oil exports to the Red Sea port of Yanbu.

That backdrop drove a fresh jump in commodity prices, with oil prices continuing to move higher. So Brent crude jumped +3.36% to $94.07/bbl by yesterday’s close, and is up a further +1.96% this morning to $95.94/bbl. Moreover, investors also priced in a longer period of high oil prices, and the 6-month Brent future (+0.59%) hit a one-month high of $81.74/bbl yesterday as well. And elsewhere, the energy shock was extending beyond oil prices, with European natural gas futures (+4.82%) exceeding their recent high back in March yesterday, closing at levels last seen in early 2023, at €62.54/MWh.

The latest rise in energy prices led to fresh concerns about a more prolonged stagflationary shock, with investors pricing in more inflation as a result. In fact, the 1yr Euro inflation swap (+4.7bps) was up for an 8th consecutive day to 2.64%, whilst the 1yr US inflation swap (+1.2bps) also rose to 2.05%. Unsurprisingly, that also saw investors price in a more hawkish path for central banks. So Fed futures are now pricing in a 36% chance of a rate hike next week, having now unwound most of the moves after the downside CPI surprise last week. And over in Europe, investors are now pricing in 48bps of further hikes by year-end, on top of the 25bps we had last month. Indeed, that’s the most hawkish path priced for the ECB in the last couple of months.

With markets expecting more inflation and more rate hikes, that meant sovereign bonds took a fresh hit on both sides of the Atlantic as well. So US Treasury yields moved higher, with the 2yr yield (+3.5bps) up to 4.30%, its highest since February 2025, whilst the 10yr yield (+2.7bps) hit its highest since May, at 4.66%. In addition, there were some fresh milestones for real yields, with the 2yr real yield (+3.0bps) up to its highest since September 2024, at 2.34%, whilst the 10yr real yield (+1.6bps) hit its highest since October 2023, at 2.36%. Over in Europe there were more marginal increases, but yields on 10yr bunds (+0.7bps), OATs (+0.6bps) and BTPs (+0.8bps) all moved higher as well.

As all that was happening, equities have put in a much more mixed performance over the last 24 hours. In the US the tone has been more negative, with the S&P 500 down -0.14%. But in other regions things have been much more positive, and overnight we’ve seen the KOSPI (+3.98%), the Hang Seng (+1.34%) and the Nikkei (+0.52%) all advance. The main exception has been in mainland China, where the CSI 300 (-0.20%) and the Shanghai Comp (-0.19%) are both lower. But the European indices put in a solid performance as well yesterday, with the STOXX 600 up +0.58%.

US equity futures have continued to lose ground overnight following Alphabet and Tesla’s earnings after the US close. Alphabet delivered a solid earnings and revenue beat, reporting 82% yoy growth in cloud revenue in Q2 ($24.8bn vs $22.5bn est.). But its shares fell by over -3% in after-hours trading as the company increased its 2026 capex plan to a range of $195-205bn (vs. $186bn est.). And Tesla fell by over -4% after-hours after the company reported its first negative quarter of free cash flows in over two years, as solid auto sales were outweighed by a 47% yoy surge in operating costs. So futures on the S&P 500 are down another -0.13% this morning.

In general however, the equity picture has been pretty resilient over the last 24 hours, despite the latest uptick in oil prices, with fresh gains in Asia overnight. That might seem striking, but we’ve written before (link here) how oil prices beneath $100/bbl haven’t been enough to cause a meaningful dent in risk assets. Indeed, if you look earlier in the year, it wasn’t until they got to around $110/bbl that you saw meaningful vulnerabilities for equities and credit. Likewise, back in the 2022 energy shock, it was a similar real-terms threshold for Brent (above $110/bbl in today’s prices) that started to cause meaningful stress, which we’re still some way from right now. So for now at least, the current pattern is still consistent with what we saw earlier in the year.

Elsewhere in Asia, the yen did briefly strengthen yesterday after a Bloomberg report said that BoJ officials were open to faster rate hikes than the consensus expected. According to the report, it said officials were aware of expectations for hikes roughly every six months, but they were open to earlier moves instead. Moreover, the article said there were signs of inflation becoming more entrenched, whilst the yen’s decline meant there were further inflationary pressures. Those gains were then pared back, and this morning the yen is still trading at 163.06 per US dollar. However, front-end yields have continued to climb, with Japan’s 2yr yield (+2.5bps) at a post-1995 high of 1.48% this morning.

Otherwise overnight, the Australian dollar has strengthened +0.28% against the US dollar after the latest employment data for June led to mounting expectations of another RBA rate hike this year. The data showed employment up by +76.3k in June (vs. +15.0k expected), which was the biggest monthly jump in 14 months.

Looking forward, today’s main highlight will be the ECB’s policy decision at 13:15 London time. It’s widely expected they’ll keep rates on hold, after hiking at the last meeting in June. But given the latest surge in oil and gas prices, the focus will be on what they signal ahead, with markets pricing almost two further hikes by year-end. Our European economists think the ECB will maintain neutral communications in the press conference. So no explicit forward guidance, with an emphasis on a data-dependent, meeting-by-meeting approach that avoids pre-committing to a specific path. However, they do think the ECB will convey a hawkish stance on inflation, consistent with another 25bp hike in September being highly probable. For more info, see their full ECB preview here.

Otherwise in Europe, UK gilts saw a very marginal outperformance after the June CPI data surprised on the downside. It showed headline inflation falling more than expected to +2.6% in June (vs. +2.7% expected). However, some of the details weren’t quite as dovish in their implications, with core CPI actually remaining at +2.6% (vs. +2.5% expected). So 10yr gilt yields were still up up +0.5bps on the day, only slightly beneath the +0.7bps increase for 10yr bunds.

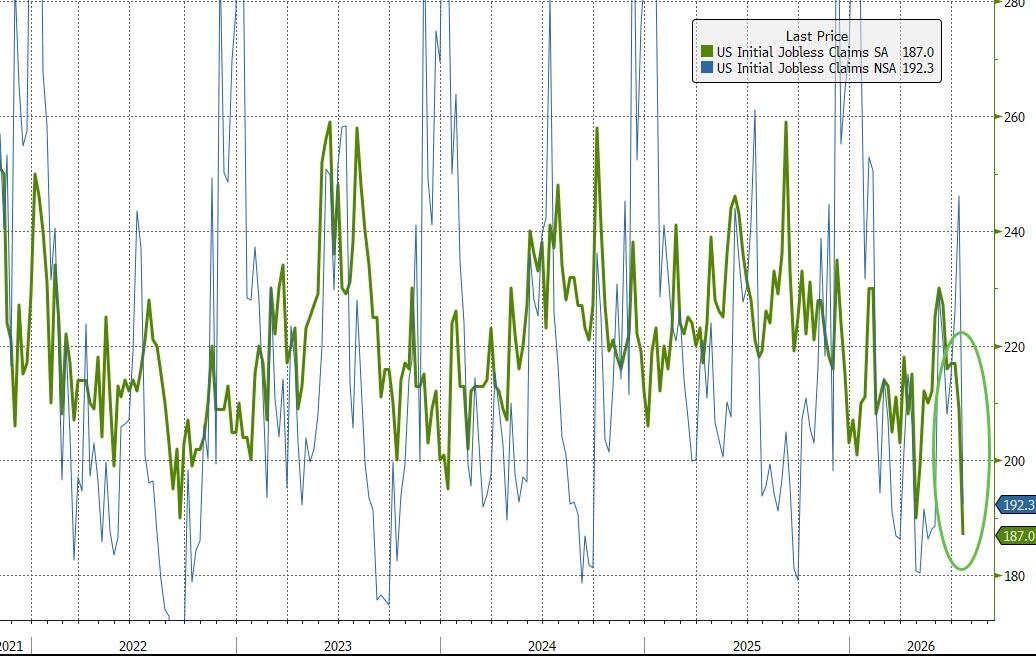

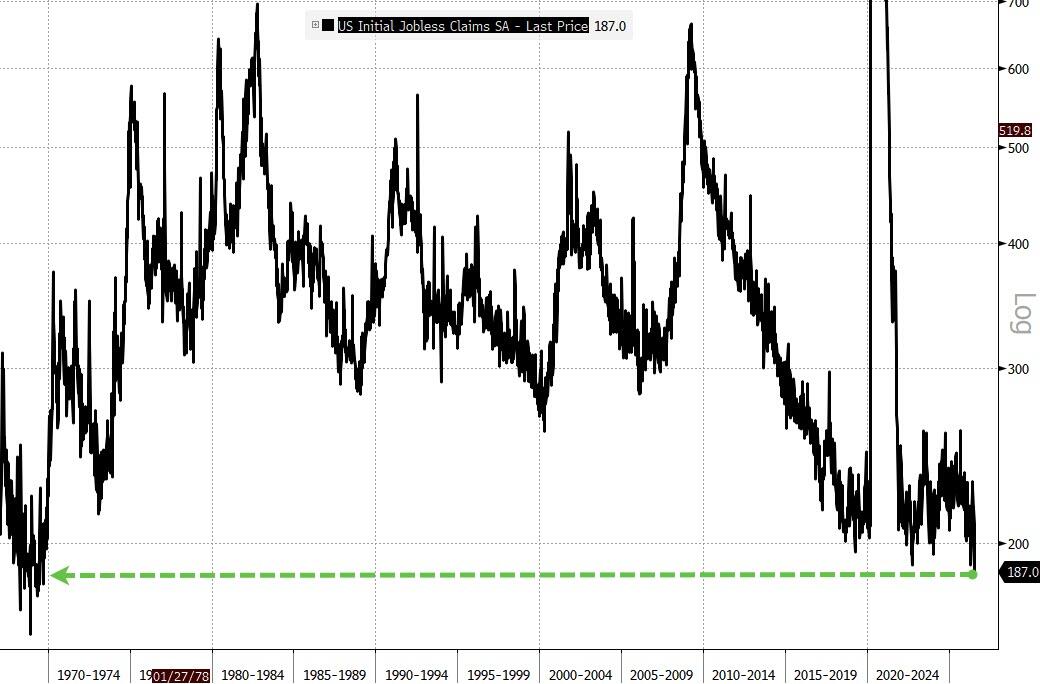

Looking at the day ahead, the main highlight will be the ECB’s monetary policy decision and President Lagarde’s subsequent press conference. Otherwise, data releases include the US weekly initial jobless claims, and the European Commission’s advance consumer confidence indicator for the Euro Area in July. Finally, today’s earnings releases include Intel.

Tyler Durden

Thu, 07/23/2026 - 08:05

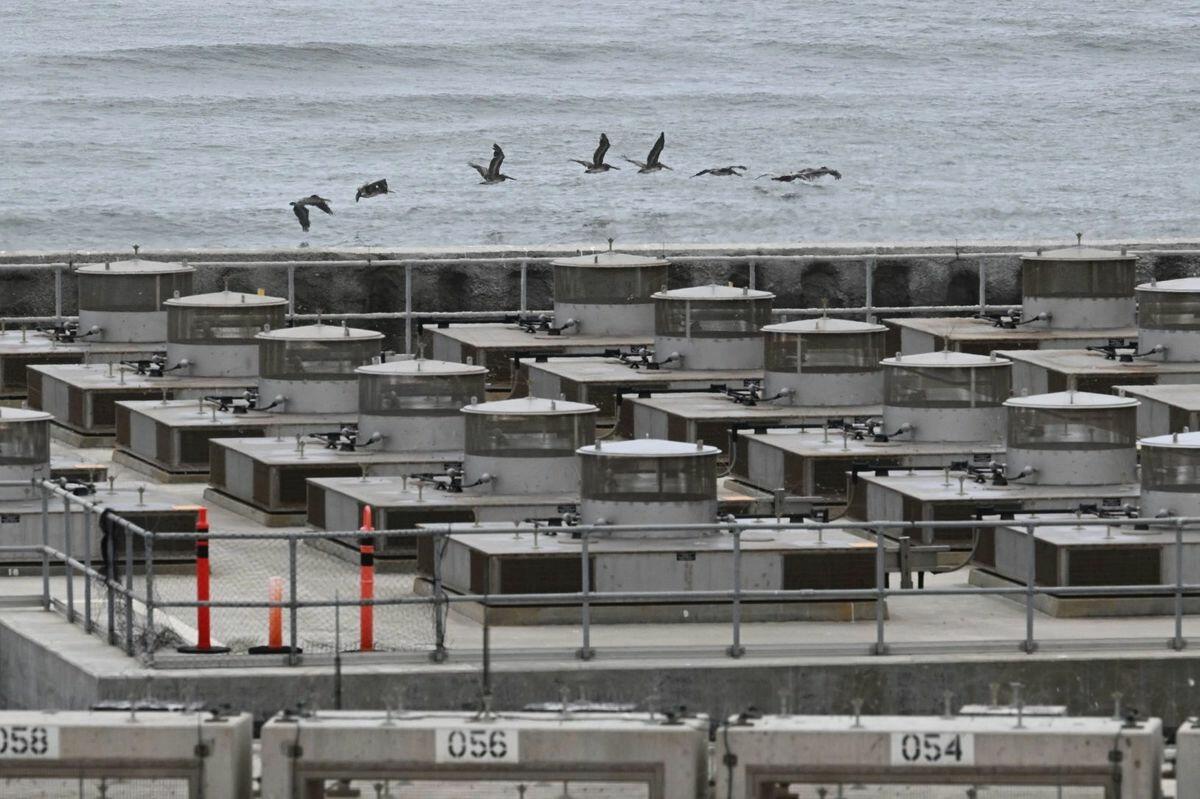

Birds fly along the Pacific Ocean near the dry fuel storage of canisters containing spent nuclear fuel at the San Onofre Nuclear Generating Station (SONGS) along the Pacific Ocean south of San Clemente in San Diego County, Calif.., on June 9, 2023. Patrick T. Fallon/AFP via Getty Images

Birds fly along the Pacific Ocean near the dry fuel storage of canisters containing spent nuclear fuel at the San Onofre Nuclear Generating Station (SONGS) along the Pacific Ocean south of San Clemente in San Diego County, Calif.., on June 9, 2023. Patrick T. Fallon/AFP via Getty Images A technician monitors Natura Resources’ MSR-1 molten salt research reactor in Lockhart, Texas, in 2024. The reactor is the first liquid-fueled advanced reactor ever licensed and the first university research reactor approved in more than 30 years. Courtesy of Natura Resources

A technician monitors Natura Resources’ MSR-1 molten salt research reactor in Lockhart, Texas, in 2024. The reactor is the first liquid-fueled advanced reactor ever licensed and the first university research reactor approved in more than 30 years. Courtesy of Natura Resources New York Gov. Kathy Hochul in New York City on March 19, 2026. Michael M. Santiago/Getty Images

New York Gov. Kathy Hochul in New York City on March 19, 2026. Michael M. Santiago/Getty Images People look at a BYD Seagull car by Chinese electric vehicle (EV) manufacturer BYD Auto at the Bangkok International Motor Show in Nonthaburi on March 27, 2024. Lillian Suwanrumpha /AFP via Getty Images

People look at a BYD Seagull car by Chinese electric vehicle (EV) manufacturer BYD Auto at the Bangkok International Motor Show in Nonthaburi on March 27, 2024. Lillian Suwanrumpha /AFP via Getty Images Polestar 4 (via Top Gear)

Polestar 4 (via Top Gear) Electrical transmission poles and lines in Commerce, Calif., on Aug. 7, 2025. Mike Blake/Reuters

Electrical transmission poles and lines in Commerce, Calif., on Aug. 7, 2025. Mike Blake/Reuters

A voter arrives at the Moorestown Township Fire Station to cast a ballot in the 2025 general election. (Emma Lee/WHYY)

A voter arrives at the Moorestown Township Fire Station to cast a ballot in the 2025 general election. (Emma Lee/WHYY)

via Middle East Institute (MEI)

via Middle East Institute (MEI)

via Associated Press

via Associated Press

Recent comments