Futures Jump As Chipmakers Surge After Japan , Korea Bounce

US stock futures are higher led by Tech after a strong bounce in chip stocks in Japan (memory stock Kioxia traded limit up after trading limit down on Friday and Monday was a holiday) and Korea, as evidence mounts that Momentum / Semis pullback have bottomed, with supportive price action elsewhere in Asia and Europe, though the JPM EU Trading Desk is not yet seeing follow-through buying in Semis. As of 7:20am ET, S&P futures are 0.5% higher, lagging the 1.4% bounce in Nasdaq futures helped by a report that TSMC is planning price hikes, although it is unclear if the early ramp will persist amid the re-escalating war with Iran which overnight saw Houthis impose a blocakde on Saudi Arabia. In premarket trading, most Mag 7 names are higher with semis leading (SOXX +4%). Cyclicals ex-Energy are leading Defensives with both Staples and HC net lower and AI boosting Industrials and Utils. WTI crude is trading near its highs, boosting Energy as all 3 commodity complexes move higher with silver the standout which has traded in tandem with the AI theme. The yield curve is twisting steeper with yields ranging from -1bp to +1bp with USD flat. Today’s macro focus is on the weekly ADP number and regional Fed activity. US economic data calendar includes ADP weekly employment change (8:15am) and July Philadelphia Fed non-manufacturing index (8:30 am). Fed speaker slate is blank during July 18-30 external communications blackout period around the July 28-29 FOMC meeting.

In premarket trading, chipmakers and other AI-related firms rebound after the sector suffered some recent weakness. Movers include Intel (INTC +5.5%), Sandisk (SNDK +8.1%), Micron (MU +6.8%), CoreWeave (CRWV +3.8%), GE Vernova (GEV +2.5%) as the entire trillion-dollar sector continues to trade like a rabid pennystock.

- Tesla and Nvidia are leading Magnificent 7 stocks higher during the AI rebound (Tesla +1.2%, Nvidia +1.1%, Alphabet +1%, Meta +0.4%, Amazon +0.2%, Apple -0.4%, Microsoft -0.7%).

In corporate news, BlackRock’s coming debt sale of more than $12 billion for a Meta Platforms data center is the result of years spent transforming a public investments giant into a heavy hitter in private markets too.

- The Paramount-Warner deal, paused Monday by a federal judge, faces a legal hurdle that risks putting the deal on hold for months at a cost that could quickly climb to billions of dollars.

- Nike’s soccer boss said the World Cup ending “was not what we dreamed,” as Spain and Argentina — both Adidas teams — faced off in the final after beating Nike-clad teams in the semifinals.

Chipmakers are leading the gains in premarket trading, along with associated memory storage and semiconductor equipment names, helped by a report that TSMC is planning price hikes. Tech was also buoyed by upbeat Taiwan and South Korean export data, supportive Wall Street commentary (virtually every bank is begging for a momentum bounce knowing well that if one doesn't come it will get very ugly) and an absence of new geopolitical flashpoints. Even so, nagging worries about margin debt and inflation loom for the AI trade. To wit, according to the trading desk at UBS, the sharp selloff in momentum stocks may be nearing its end, creating an opportunity for investors to start rebuilding positions in AI and semiconductor shares.

“While volatility is likely to remain high given the elevated concentration still present in parts of the market, the correction has been both deep and lengthy enough to alleviate some valuation concerns,” said Santiago Mateo Yanguas, head of equity at CaixaBank AM.

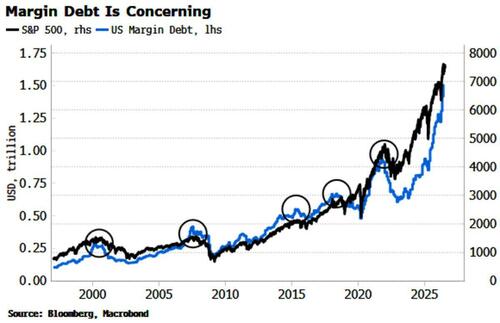

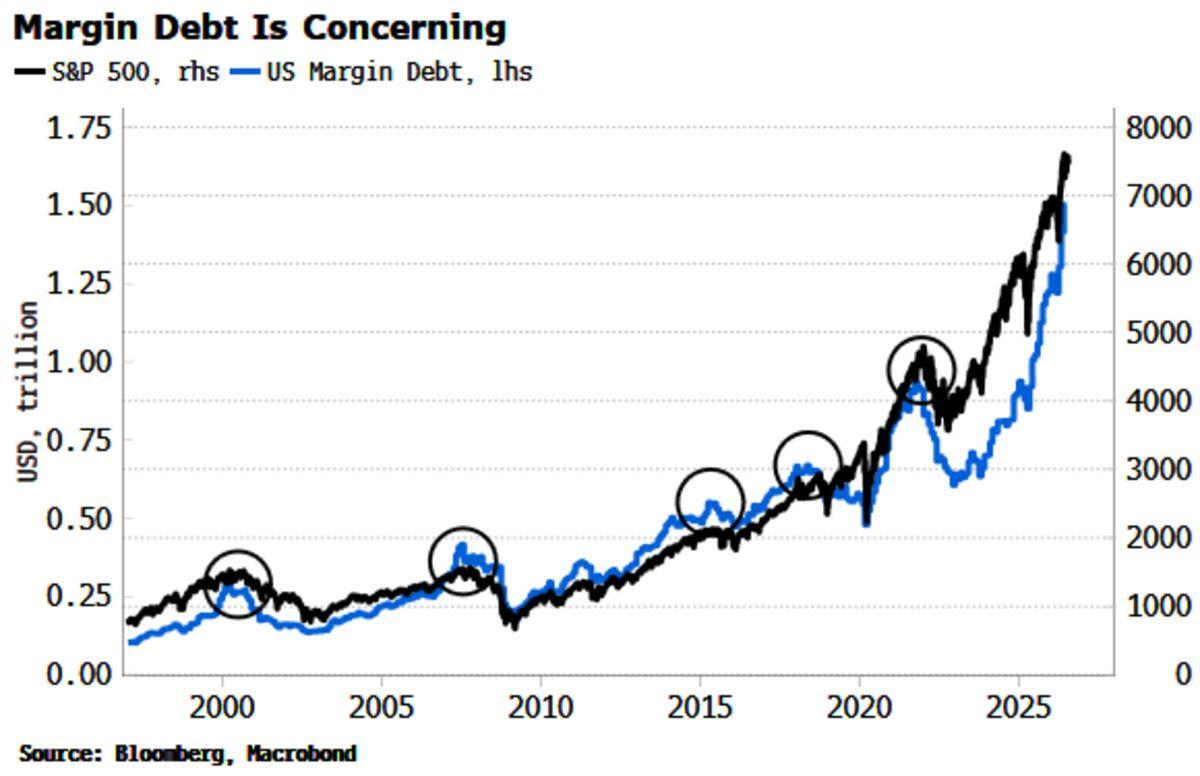

South Korea’s exports data adds further support for chips, with semiconductor exports climbing by a perfectly sustainable about 181% YoY for the first 20 days of July. Taiwan’s June export orders from the US rose nearly 84% year-on-year, the fastest pace on record. Whether the AI rally can extend will depend heavily on the reporting season and, as Bloomberg highlights, the biggest concern is leverage with US margin debt rising 49% year-on-year in June to a record high. AI capex “has stretched hyperscalers to the edge of acceptable investor limits,” notes JonesTrading chief strategist Mike O’Rourke.

Others were more bearish: equity investors should look to reduce some exposure after this earnings season, according to HSBC’s Max Kettner, who warns that stretched sentiment, a fading fiscal impulse, and US midterm election uncertainty could trigger a pullback.

TSMC is set to raise prices for advanced and mature chip production services by up to 10% in 2027 to reflect rising costs, Nikkei Asia reports. It follows a report last week of ASML raising prices for its equipment, for which TSMC is ASML’s largest customer. While price increases underpin the demand story, it will stoke concerns of inflationary pressures and traders will be on watch for corporate margin hits from memory costs during this earnings season.

Focus will soon shift to the start of the reporting season for Big Tech firms, where AI hyperscalers will update investors on their capital spending plans. Alphabet Inc. reports on Wednesday, while Microsoft Corp., Meta Platforms Inc. and Amazon.com Inc. are due next week. “The next test is no longer whether AI demand exists, but whether pricing, margins and cash flow can justify the capex bill,” said Florian Ielpo, head of macro at Lombard Odier Investment Managers. “If they can, the rebound should broaden. Otherwise, volatility remains the regime.”

A question that investors are asking themselves is whether now is the time to sell chips and rotate toward hyperscalers, which have underperformed semiconductors this year, according to Alexandre Drabowicz, chief investment officer at Indosuez Wealth Management in Paris. “Our view is that one needs to be invested in both,” Drabowicz said. “Alphabet’s earnings this week will be a real bellwether for the industry and its capacity to monetize AI. We believe the market underestimates how fast these companies will be able to monetize.”

Global trade faces a fresh headache as the Panama Canal moves to curtail some vessel-booking slots because of water-supply challenges. Overnight, the Trump admin vowed to impose a fresh 50% tariff on some Canadian goods over what it said was unfair treatment of American alcohol, cars and dairy.

In politics, Defense Secretary Pete Hegseth is set to testify before lawmakers to defend the Trump administration’s request for billions of dollars in additional money for the Iran war. Trump met with a pair of key Republican senators on Monday evening to discuss a path forward on legislation that would override state laws on AI. A federal appeals court denied Joe Biden’s request for a temporary block to stop the Justice Department from turning over tapes and transcripts to the Heritage Foundation. Seperately, the DOJ has launched a new investigation into Harvard University, alleging that some of its financial aid programs violate civil rights law by excluding American citizens.

European stocks are up too, the Stoxx 600 rising 0.2%, also being led by the technology sector. After two days in the red, as gains in the technology sector and a slew of robust earnings counter news about the continuing US-Iran clashes. Here are the biggest movers Tuesday:

- Mitie Group shares surge as much as 42% after agreeing to a takeover by OCS Group at a big premium to Monday’s close. The facility management company’s shares remain below the offer price

- Babcock rises as much as 8.3%, leading gains amoung European defense stocks on Tuesday after the UK’s new prime minister Andy Burnham told NATO Secretary General Mark Rutte that John Healey’s appointment as Chancellor was a “signal of his intent” on defense

- Var Energi shares gain as much as 5.9% and BlueNord rises as much as 6.7% after the former made a $1.3 billion offer to acquire the latter; Var Energi also reported 2Q results and reaffirmed its production forecast

- Bossard shares jump as much as 11%, hitting their highest level since October 2024, after first-half results from the maker of fastening devices beat expectations, which analysts said provides better visibility on the full-year outlook

- Genuit Group gains as much as 3.2% after analysts at Stifel initiated coverage on the maker of plastic piping systems with a buy rating and said they see an inflection point coming, driven by regulatory and structural drivers

- Basic resources stocks gained the most in the Stoxx 600 index as copper headed for its highest close since mid-June on signs that supply conditions in China are continuing to tighten. Gold touched its highest level in a week on dip-buying

- Boliden drops as much as 7.6%, to the lowest since May 5, after the mining company delivered revenue and operating profit below expectations in the second quarter, along with negative free cash flow

- Wartsila shares drop as much as 4.6% as JPMorgan flags the company lowering its demand outlook for the Energy division. That’s overshadowing the company’s strong beat on orders in the second quarter

- Schindler shares fall as much as 6.1%, the most in five months, after second-quarter revenues missed estimates, offsetting a better-than-expected margin performance

- Julius Baer shares declined as much as 5.3% as beats on net income and assets under management were overshadowed by the lack of update on a regulatory review and any subsequent share buybacks

- Jungheinrich shares drop as much as 5.5% after Germany’s financial regulator BaFin opened an accounting review on whether the company breached financial-reporting rules in connection with the planned sale of the company’s Russian business

Asian stocks rose for the first time in four sessions as investors rush back into chip stocks after a recent rout. The MSCI Asia Pacific Index jumped as much as 2.3%, the most since July 15, led by TSMC, Samsung and SK Hynix. South Korea and Taiwan led the gains in the region, with most other markets also climbing higher as investor sentiment improves. Taiex’s 3.6% rise was the most in three weeks. Japan’s Nikkei 225 rose 2.7% after slipping into correction territory on Friday. While investors continue to debate whether AI spending is justified, the recent tech selloff has drawn some back to hunt for bargains. Several megacap earnings due later this week, including Tesla and Alphabet Inc., will shed further light on whether the AI-driven rally can regain momentum. “The market has already undergone a fairly substantial correction,” said Ikuo Mitsui, a fund manager at Aizawa Securities. “At the same time, corporate earnings have held up reasonably well and have proved more resilient than expected.”

In FX, the dollar is fluctuating, albeit in a narrow range. The yen is lagging, while the Norwegian krone and Aussie dollar are stronger.

In rates, treasury yields are little changed in early US trading with the yield curve steeper, tracking similar price action across most developed sovereign bond markets, with oil prices and stock index futures higher inside Monday’s ranges. Tiny overnight yield ranges included less than 2bp for 10-year. US session has no major calendar events. Yields across tenors remain within about a basis point of Monday’s closing levels, the 10-year just under 4.60%. Treasury futures volumes through 7am New York time were 60% to 90% of 20-day average level. IG credit new-issue calendar includes is blank so far, but at least one potential borrower stood down Monday as three issuers raised a combined $4.5 billion, and may return. Treasury coupon auctions this week include $13 billion 20-year reopening Wednesday and $21 billion 10-year TIPS new issue Thursday. Germany is underperforming at the long end in Europe. UK government bonds ticked higher as investors awaited fresh policy details from new Prime Minister Andy Burnham. Weak economic data dimmed bets on higher interest rates.

In commodities, oil prices have been mostly lower for the session so far and Brent is sitting a little short of $89/barrel, while gold has come off its high but is still in the green and above $4,000/oz.

The US economic data calendar includes ADP weekly employment change (8:15am) and July Philadelphia Fed non-manufacturing index (8:30 am). Fed speaker slate is blank during July 18-30 external communications blackout period around the July 28-29 FOMC meeting.

Market Snapshot

Top Overnight News

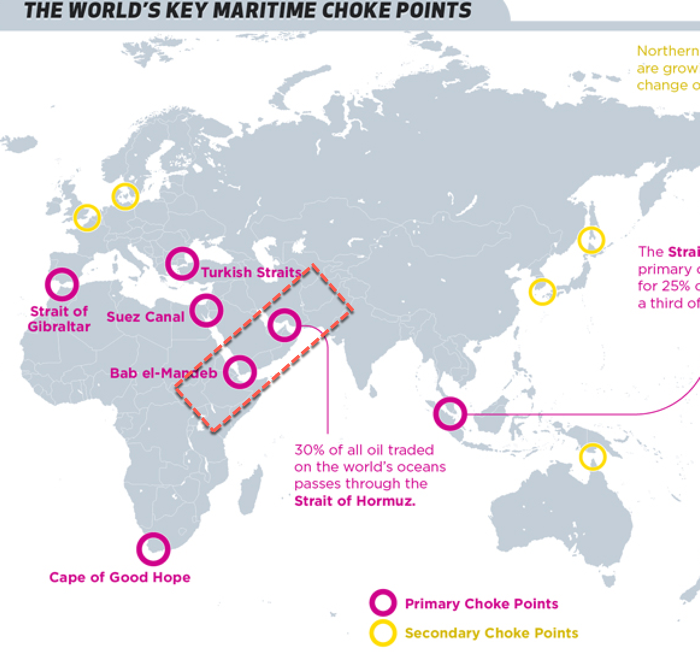

- President Trump is nearing a decisive fork in the Iran war, with U.S. and Israeli officials envisioning only two viable endgames: Option 1: Pursue a new 10-day ceasefire aimed at reopening the Strait of Hormuz. Option 2: Launch a massive joint military campaign with Israel to force Tehran's capitulation. Axios

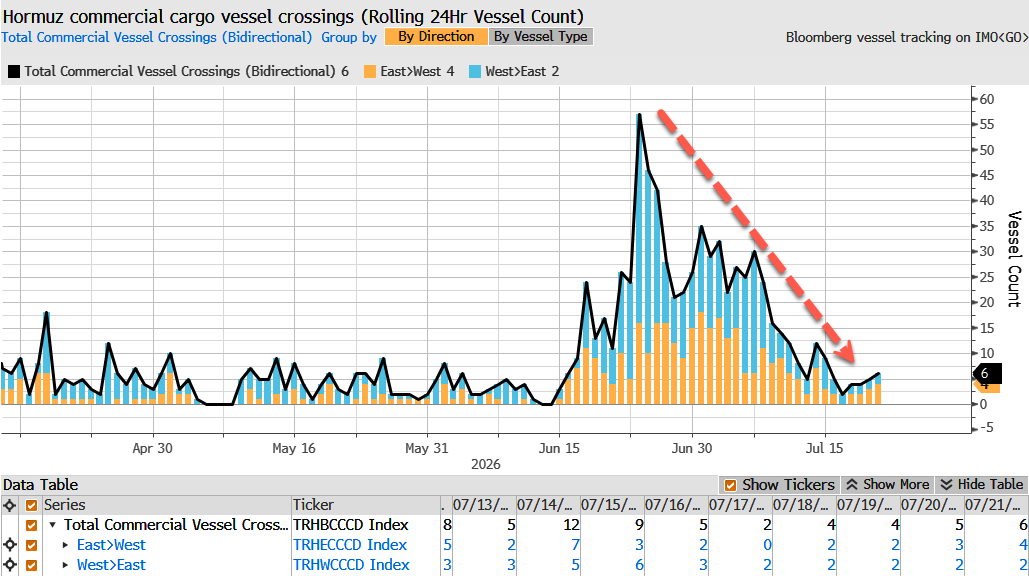

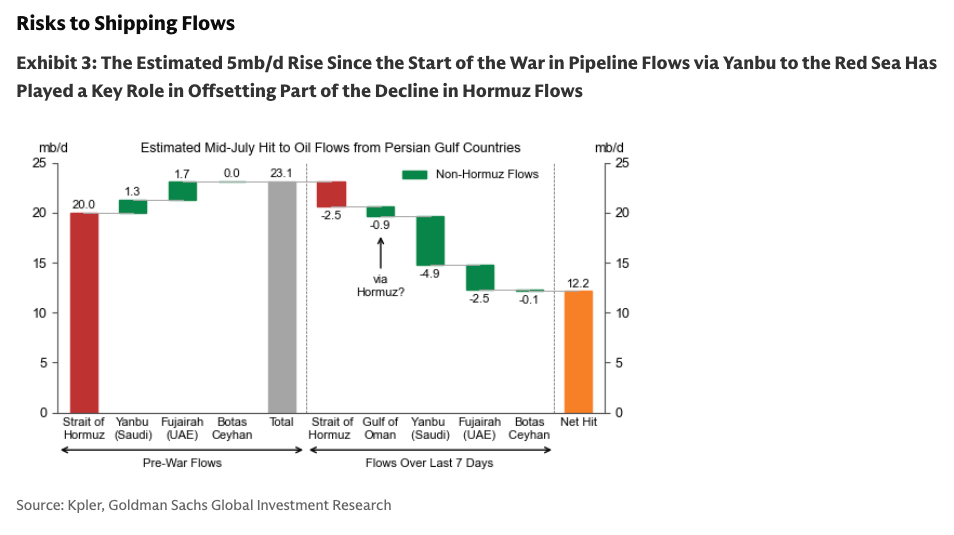

- Vessel traffic through the Strait of Hormuz has slumped since U.S. President Donald Trump’s blockade took effect last week, with shipowners increasingly avoiding one of the world’s most important energy corridors as fighting between the U.S. and Iran intensifies. CNBC

- China is mounting one of its broadest efforts in years to steady the stock market, with regulators, state-backed investors, insurers and asset managers all moving to shore up confidence after a selloff in tech shares. BBG

- China’s cabinet pledged to ensure the country will meet its full-year economic goal and to forge ahead with implementing policies, after growth slipped below the official target range in the second quarter. BBG

- Chinese regulators are considering tightening export controls on artificial intelligence and semiconductor technologies, as the US-China rivalry intensifies in cutting-edge AI. FT

- The US vowed to impose a new 50% tariff on some Canadian goods, citing unfair treatment of American products. The levies would apply to items including milk and beer but exempt energy, potash and critical minerals. BBG

- London Stock Exchange plans to launch a 24/5 trading venue to support digital, algorithmic and agentic trading. It’ll operate separately from LSE’s Main Market, with ETPs set to debut next year. BBG

- OpenAI and Anthropic executives are sounding the alarm about the rise of cheap AI, particularly powerful new models produced in China, suggesting they will lead to a “dystopian” AI future and present unacceptable security risks without regulation. WSJ

- The cost of protecting Oracle Corp.’s debt against default reached a fresh multi-year high on Monday while its existing bonds sold off, as doubts grew over whether the company’s massive investments in artificial intelligence will pay off. BBG

- US President Trump signed an order to identify and fix potential national security vulnerabilities by requiring defence contractors to screen their supply chains, aiming to stop weapons makers from working with certain foreign suppliers including China.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the subdued handover from the US, where most major indices declined as oil prices and yields climbed amid the ongoing geopolitical backdrop, although the Nasdaq showed some resilience amid a bounce in tech and telecommunications. ASX 200 lacked firm direction with price action contained within relatively tight parameters in the absence of notable data or key macro drivers. Nikkei 225 rallied on return from the long weekend, with some bargain-hunting after last Friday's slump. KOSPI shrugged off earlier indecision and rallied amid a tech rebound, with notable strength seen in Samsung Electronics and SK Hynix shares. Hang Seng and Shanghai Comp were mixed with price action range-bound as they took a breather after rallying yesterday amid stimulus hopes and China’s “national team” buying close to USD 9bln in equities.

Top Asian News

- Japan's Cabinet approved an economic framework policy document including fiscal plan, which cites BoJ autonomy and lacked sales tax decisions.

- Japan is reportedly to relax rules surrounding bank lending for M&A and incentivise pension funds to invest more in alternative assets.

- New Zealand Inflation Rate QoQ (Q2) Q/Q 1.5% vs. Exp. 1.4% (Prev. 0.9%).

- New Zealand Inflation Rate YoY (Q2) Y/Y 4.1% vs. Exp. 4% (Prev. 3.1%).

- South Korea July 1st-20th Exports rose 52.3% Y/Y, Imports rose 20.0% Y/Y and Trade Balance is at a provisional surplus of USD 12.2bln.

- Taiwan Export Orders (Jun) Y/Y 59.4% (exp. 47.3%).

european bourses are mixed and ultimately trading on either side of the unchanged mark. Tentative action which is encapsulated by the tumultuous geopolitical environment and a number of earnings from within the region. European sectors hold a slight negative bias. Tech outperforms followed by Basic Resources, whilst Optimised Personal Care and Media reside at the bottom of the pile. The Tech sector continues to bounce back from recent losses, following a similar theme seen in the APAC session, where the KOSPI gained c. 3.5%.

Top European News

- UK government to remove VAT on electricity bills from October 1st, funded by cancellation of the Digital ID programme, as part of new tax cut measures.

- UK PM Burnham reportedly to slash business rates for the hospitality sector by 20% within days, Huffington Post reported. Additionally, a GBP 2 cap on bus fares is also set to be unveiled as soon as Wednesday.

- Worldpanel announced grocery inflation and sales (w/e 12th July): Grocery Inflation 2.6% (prev. 3%).

FX

- G10s are mixed against the Buck. Antipodeans lead after a hotter-than-expected NZ CPI; JPY underperforms after the Japanese cabinet excluded a sales tax decision from its fiscal plan.

- DXY is a touch lower today, with oil prices softer but lacking direction as we await further geopolitical updates. Overnight, Axios reported that senior US and Israeli officials are claiming Trump’s options were to either promote a new 10-day ceasefire or launch a full-scale war on Iran. Elsewhere, Fox reported Trump will decide in the coming days whether to expand military operations against Iran. ING opines USD risks remain to the upside, given the aforementioned factors. Given the above, focus remains on incoming Gulf newsflow with a light calendar ahead of the Fed’s meeting next week. DXY remains below the 21DMA at 100.05, currently between 100.90 and 101.

- GBP in focus today after UK PM Burnham appointed former Defence Minister Healey as Chancellor (see 09:50 analysis for more detail). Elsewhere, UK jobs saw the unemployment rate remain steady at 4.9%, whilst the Employment Change topped expectations, while the wages components were flat/very slightly firmer. Overall, a report which will have little impact on the BoE, ahead of CPI on Wednesday and Flash PMIs on Friday. GBP takes a breather just above 1.3420 in Cable, and a little weaker just above 0.85 in the EUR cross.

- JPY is on a weaker footing despite the aforementioned subdued Dollar and softer oil prices. Overnight, Japan's Cabinet approved the economic framework policy document, including a fiscal plan, which cited BoJ autonomy but lacked a sales tax decision. Amid the uncertainty given the lack of a funding plan, USD/JPY resides towards the upper end of a 162.43-162.70 range.

- Antipodeans hold on to the spoils of the prior day's outperformance, with Aussie propped up by firmer metals whilst the Kiwi is leading after firmer-than-expected New Zealand CPI data. AUD/NZD is a modest touch lower, Aussie and Kiwi both +0.4% against the Buck.

Fixed Income

- Global fixed income benchmarks trade range-bound, in line with energy prices, despite the risk-on tone seen across the equity space. Equities seem to enjoy the reporting around a possible 10-day ceasefire, with recent reporting hinting that the US is demanding a longer ceasefire.

- Gilts (+1 tick) trade higher, despite the announcement of former Defence Secretary Healey as Chancellor. Thus far, gilts have taken this as fairly positive, possibly taking comfort in the fact that he used to work in the Treasury in past governments. In terms of Burnham's policy, Bloomberg reported that the UK government will remove VAT on electricity bills from October 1st, funded by cancellation of the Digital ID programme. There have been contradictory reports over whether this measure will be fully funded. The Times reported that this will be fully funded; however, the OBR said the GBP 1.8bln figure for the ID scheme was unfunded, while former UK minister Jones suggested that Burnham's cut is also unfunded. More recently, the Huffington Post reported that Burnham is to slash business rates for the hospitality sector by 20%, while a GBP 2 cap on bus fares is also set to be unveiled soon.

- On the data front, the ONS released its May employment report; employment change 147k (exp. 85k, prev. 100k), unemployment change 4.9% (exp. 4.9%, prev. 4.9%). Despite the strong labour report, gilts have failed to react, given the focus on politics.

- Bunds (-10 ticks) rotate in a 124.59-124.81 range. Focusing on the short-end, the yield currently trades outside of the 2.52-2.76% range, driven by the recent leg higher in energy prices. Brent has recently returned above the USD 90/bbl mark, resurfacing worries of an energy pass-through into inflation. ING says that rates can take a hawkish view, with the 2yr euro swap rate touching 3%, because the EZ growth picture continues to recover. Additionally, implied bond volatility is at lower levels, compared to the early stages of the Middle East conflict.

- USTs (+1 tick) lack direction given the quiet docket this week, heading into the Fed policy announcement next week.

- Germany sells EUR 4.553bln vs exp. EUR 6bln 2.90% 2031 Bobl: b/c 1.48x, average yield 2.89%, retention 24.1%.

- The UK sells GBP 5bln 4.00% 2029 Gilt: b/c 3.42x (prev. 3.35x), average yield 4.463% (prev. 4.238%), tail 0.3bps (prev. 0.2bps).

Commodities

- Geopolitics remain fluid with constructive and escalatory updates on the US-Iran front. On the former, a 10-day ceasefire proposal was pitched, while Iran confirmed ongoing mediation talks, which keeps alive the possibility of a return to the June interim MoU. On the other hand, last night was the 10th consecutive day of US airstrikes, whilst Iran continues targeting the region and reiterated that the Strait of Hormuz is closed. US President Trump is expected to decide in the coming days whether to expand military operations against Iran and return to full-scale combat, a senior US official told Fox News. Meanwhile, senior US and Israeli officials are claiming Trump only has two realistic options: either promoting a new 10-day ceasefire with the aim of reopening the Strait of Hormuz, or launching a full-scale war on Iran, Axios reported. Further, a US official said if US President Trump decides to expand the war, the strikes will include Tehran and nuclear sites, according to Al Arabiya.

- Crude oil futures are trading subdued as market participants weigh emerging diplomatic de-escalation signals against ongoing military exchanges in the Middle East. Brent crude futures fell to the bottom end of a USD 88.08-89.45/bbl range while WTI similarly waned to the lower end of a USD 81.64-83.05/bbl range. Also on the supply side, NHC reported that Tropical Storm Bertha has strengthened, situated right in the Gulf of Mexico. Dutch TTF bucks the trend and has edged higher, back above the EUR 59.23/MWh mark, in the European morning, with analysts suggesting gas will be impacted more by the Middle East situation.

- Precious metals are on a firmer footing as the Dollar and inflation expectations ease with oil prices. Spot gold trades towards the upper end of a USD 3,999/oz to USD 4,084/oz range. Spot silver surges 4.5% at the time of writing as it rises above USD 59/oz vs Friday’s 54.77/oz base.

- Base metals also cheer the pullback in the Dollar alongside expectations of Chinese stimulus following recent weak economic data. 3M LME copper is firmer by 1.5% at the time of writing and towards the upper end of a USD 13,603.73- 13,840.00/t range.

- UAE's ADNOC has approved a USD 6.2bln project to boost natgas production, Bloomberg reported.

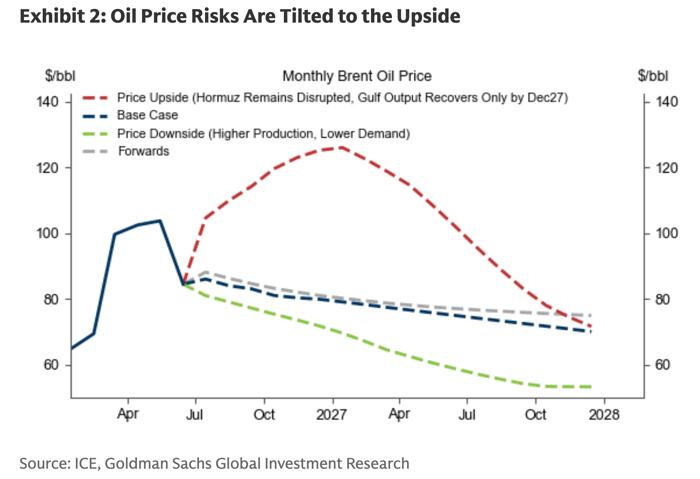

- Goldman Sachs said Brent may rise above USD 120/bbl in FY26 Q4 if Hormuz remains disrupted.

Trade/Tariffs

- The US is imposing an additional 50% tariff on certain products of Canada including some USMCA products, to counter Canadian bias against US commerce with respect to alcoholic beverages, dairy, motor vehicles. In response, Canadian PM Carney said Canada is ready to engage intensively to address issues with the US and said we're ready to talk with the US about modernising the USMCA. Additionally, the Ontario Premier said that Canada should impose retaliatory tariffs against the US.

- China is weighing tighter export controls on AI models and chips, according to FT.

Central banks

- ECB Bank Lending Survey (Jul): Euro area banks reported a moderate net tightening of credit standards for loans or credit lines to enterprises in Q2'26.

Geopolitics: Middle East

- It was Iran which proposed the 10-day ceasefire, i24's Stein reported, citing sources. The US said to be demanding a longer ceasefire and demanding even partial navigation of the Strait of Hormuz. The goal of these 10 days, according to the two sources, is to find a solution for the Strait of Hormuz. The mediators conveyed the proposal to the US and even added additional components to it during the talks they held with Washington and Tehran so that it would be between the territory controlled by Oman and the territory controlled by Iran and through which ships could pass.

- US Energy Secretary Wright said they will continue to attack Iran and are ensuring the flow of oil, gas and other products through the Strait of Hormuz with or without Iran's cooperation. Wright said they continue to undermine Iran's offensive military capabilities and that President Trump wants to end the conflict with a peace deal, but this will require cooperation from both sides.

- US CENTCOM announced another round of strikes against Iran in which US forces struck Iranian military command centres, maritime capabilities, missile and drone launch sites and air defence systems to degrade Iran's ability to continue attacking vessels.

- US airstrikes targeted the centre of Isfahan city and several explosions were heard in Bandar Abbas, Qeshm, Chabahar, Konarak and Shiraz, while air defence systems were activated near Iran's Bushehr nuclear power plant.

- US likely does not have enough munitions to sustain a prolonged all-out war with Iran — which is already adapting to bypass US defence systems in its attacks across the region, according to an expert cited by The New York Post

- Iran claimed a strike on a US military data centre in Bahrain and stated that US radar and defence systems in Bahrain were destroyed. Iran also targeted US military facilities at Kuwait's Ahmad Al-Jaber base, US missile systems at Kuwait's Arifjan base, while explosions were reported in the Ali Al-Salem Airbase in Kuwait. Additionally, a central data infrastructure of Amazon (AMZN) in Bahrain was attacked by several cruise missiles.

- More recently, there have been reports of sirens in Qatar while explosions were heard in Jordan.

- IRGC said two tankers were hit near the Strait of Hormuz, and that the Strait of Hormuz is closed, while the UKMTO said it received a report of an incident 8NM northeast of Oman's Limah and later announced the crew had abandoned the ship.

- Yemeni Houthi commander said Saudi Arabia faces two options: either lift the blockade and stop its intervention or continue escalating, which will cost it a lot, Al Mayadeen reported.

- Israeli Finance Minister Smotrich said "the State of Israel has no interest in joining the conflict between Iran and the US - the current situation is the best for us", Ynet reported.

- Israel conducted artillery strikes on southern Lebanon, while it stated that the programme of pilot zones in southern Lebanon began on Monday, which was carried out in cooperation with US military and Lebanese armed forces. Furthermore, it will respond forcefully to any violation of the agreement.

- The Lebanese army entered Zawtar al-Gharbiya as part of the first phase of the pilot zones, Al Hadath reported, while Israeli troops departed the area.

Geopolitics: Ukraine

- Russia’s Defence Ministry said its forces have struck infrastructure used by Ukraine’s military in the port of Odesa, IFX reported.

- Russia's Kremlin said that Russia will continue targeting vessels involved in supplying Ukraine’s military.

Geopolitics: Other

- US State Department said the US calls on China to immediately cease its destabilising conduct and condemns China's dangerous and aggressive actions against Philippine Navy personnel at the Second Thomas Shoal in the South China Sea on July 20th.

- North Korea's Foreign Minister met with Russian President Putin in Moscow on 19th July, according to KCNA.

US Event Calendar

- 8:15am: ADP weekly employment change

- 8:30am July Philadelphia Fed non-manufacturing index

DB's Jim Reid concludes the overnight wrap

Yesterday I discussed the huge developments at the end of last week with Chinese open-source AI sparking another potential “DeepSeek moment”. Overnight Adrian Cox has published a timely report explaining what all the fuss is about. “Open-source AI 101: the battle for the future of AI” is a great insight for generalists into what open models are, how they differ from proprietary models like Claude and OpenAI’s GPTs, and why they are key to the AI boom. It’s on the Deutsche Bank Research Institute website here.

I think that if the Chinese model of AI development continues to gain traction, it could have significant implications for the highly capital-intensive, capex-led US approach. As such, the piece is well worth a read.

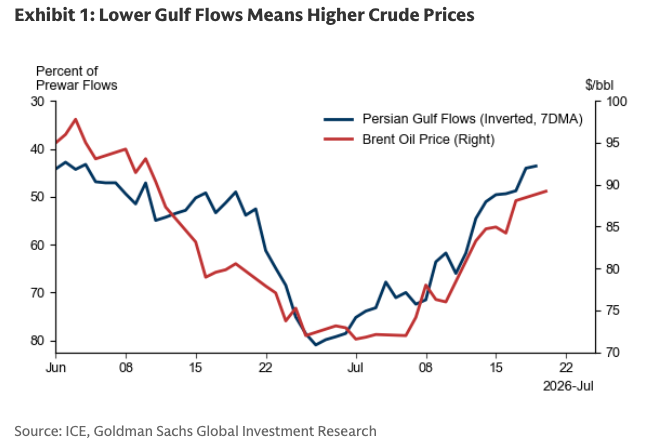

Onto markets, and they struggled to gain traction yesterday, with the S&P 500 (-0.19%) losing ground even as chip stocks stabilised after last week’s rout, while Middle East concerns lingered. There has been a recovery overnight though. On the Middle East conflict there was some hope as a spokesman for Iran’s foreign ministry said that “ideas from some mediators have been conveyed” to Iran, but escalating rhetoric from the Houthis in Yemen as well as from President Trump meant Brent crude still closed +1.27% higher at $89.22/bbl. Meanwhile, global bonds saw a broad selloff, with 10yr Treasury yields closing +4.4bps higher, in part due to a hint of looser fiscal policy from the new UK PM Burnham. 30yr US real yields also hit their highest since 2008.

Starting with Iran, we did see some improvement in sentiment yesterday as Reuters reported that a senior Iranian official had told them that mediators had passed a proposal to Iran, which would offer a 10-day ceasefire to try and revive the interim deal last month. But the headlines weren’t all positive yesterday, and shortly afterwards, oil prices pared back some of their decline after the Houthis said they’d impose a maritime blockade on Saudi Arabia, which risks adding to the oil supply disruption. The mood also wasn’t helped by Trump’s post that Iran “will pay… many times over” for the deaths of US soldiers, while the US has conducted a 10th consecutive night of strikes against Iran overnight. So with different counteracting forces, Brent crude settled +1.27% higher at $89.22/bbl, beneath its morning peak above $91/bbl but well off the lows just above $86/bbl. Overnight, Brent is -0.75% lower.

Back to the bond sell-off and the UK led the way with gilts seeing a sharp underperformance after new PM Andy Burnham said that he would use “any flexibility” within the country’s fiscal rules. Potential options for such flexibility include using up the available headroom under the fiscal rules and using off-balance-sheet structures to fund targeted capital investments. The latter may lie outside the current fiscal rules but would still add to the debt burden. So the comments were seen as opening the way for more borrowing and meant that the 10yr yield ended the day up +8.1bps at 5.03%, whilst the 30yr yield (+8.9bps) closed at 5.74%. This sell-off all happened after he spoke. We’re also expecting some further announcements from the new administration this week, and Burnham said in his first speech as PM that he’d be setting out more measures from today to support with the cost of living.

In a surprise move, we then learnt that Burnham had picked John Healey, the former Defence Secretary, as the new Chancellor of the Exchequer. Healey had been voted as one of the more investor-friendly options for Chancellor in a recent Bloomberg survey, though there’s little visibility on his fiscal views. Indeed, his highest-profile recent move was accusing the Treasury of underfunding defence as he resigned from Starmer’s government last month. In other appointments, Burnham picked Ed Miliband as foreign secretary and appointed a close ally, Louise Haigh, as first secretary of state. The latter pick coupled with Healey’s as Chancellor raises the possibility that under Burnham, Number 10 will look to exert more direct control over economic policy. The pound did recover a bit of yesterday’s earlier losses following the news of Healey’s appointment, but it was still down -0.16% against the dollar.

Whilst the UK saw the worst of the bond selloff, it was echoed around the world. In Europe, yields on 10yr bunds (+2.5bps), OATs (+1.9bps) and BTPs (+2.6bps) all moved higher, and for 10yr OATs, that took them up to a post-2009 high of 3.94%.

And over in the US, the 10yr Treasury yield (+4.4bps) was up to 4.59%. The sell-off in Treasuries was driven by real yields, with the 10yr real yield (+3.3bps) rising to 2.33%, while the 30yr real yield (+3.4bps) rose to 2.92%, its highest level since 2008. At the same time, investors priced in a more hawkish path for the Fed, with 34bps of hikes now priced in by the December meeting, up +2.3bps on the day. This has now retraced more than half of the declines seen since last week's soft CPI.

US equities struggled to recover amid the ongoing geopolitical uncertainty and rising real yields. The S&P 500 (-0.19%) retreated for a third consecutive session with two thirds of its constituents down on the day. The Philly semiconductor index (+0.60%) did see a modest recovery after its -9.97% slump last week, so it’s no longer more than -20% beneath its record high, as it was on Friday. However, the broader tech mood was still cautious, with the NASDAQ (-0.05%) and Mag-7 (-0.07%) inching lower. And over in Europe, the STOXX 600 was also down -0.30%, with the FTSE 100 (-0.71%) leading the losses amid the broader UK asset underperformance.

However there has been a bounce this morning in Asia with S&P (+0.42%) and Nasdaq (+1.03%) futures both comfortably higher. The tech recovery continues elsewhere as the KOSPI (+4.63%) is leading gains in the region after falling nearly 5% yesterday. Elsewhere, the Nikkei (+2.76%) is also firm after yesterday's holiday. In China, the CSI 300 (+1.76%) and Shanghai Composite (+0.62%) are posting solid gains, while the Hang Seng (+0.03%) is fairly flat alongside the S&P/ASX 200 (+0.08%).

Early-morning data showed that South Korea’s exports surged 52.3% year-over-year during the first 20 days of July, driven largely by semiconductor shipments, which nearly tripled amid sustained demand fueled by the ongoing artificial intelligence boom. This was one of the WOW! charts in my recent pack, with exports at over 50-year highs on a YoY basis. The trend continues.

In other overnight news, the US announced that it will impose a 50% tariff on some Canadian goods. The new tariffs were announced under Section 338 of the 1930 Tariff Act, which has never previously been used. This allows the President to impose duties of up to 50% in response to discriminatory treatment against U.S. commerce. According to US Trade Representative Greer, the new tariffs are due to take force in 30 days and will cover close to $20bn of goods, so a relatively small portion of the over $350bn of annual Canadian exports to the US. Note also that the US administration’s temporary Section 122 global tariff of 10% expires this Friday (July 24), so we may well see more US tariff announcements, especially ones justified by recent Section 301 investigations, in the coming days.

Otherwise, there wasn’t much data yesterday, but Canadian government bonds outperformed after the country’s latest CPI print surprised on the downside. So headline CPI fell more than expected to +2.8% in June (vs. +2.9% expected), and the two core measures followed by the Bank of Canada were also beneath consensus, with median core at +1.9% (vs. +2.1% expected), and trim core at +1.8% (vs. +2.0% expected). So the 10yr yield in Canada only rose +0.8bps on the day, a smaller increase than the +4.4bps jump for 10yr Treasuries.

Looking at the day ahead, it’s a quiet one, with data releases including UK unemployment for May and the German ZEW survey for July. Meanwhile from central banks, the ECB will release their Bank Lending Survey. Q2 earnings season will bubble in the background though.

Tyler Durden

Tue, 07/21/2026 - 07:39

American whiskey is seen on the shelves of a SAQ liquor store in Montreal on March 4, 2025. The Canadian Press/Christinne Muschi

American whiskey is seen on the shelves of a SAQ liquor store in Montreal on March 4, 2025. The Canadian Press/Christinne Muschi

Michigan Gov. Gretchen Whitmer speaks at an event in National Harbor, Md., on May 4, 2023. Kevin Dietsch/Getty Images

Michigan Gov. Gretchen Whitmer speaks at an event in National Harbor, Md., on May 4, 2023. Kevin Dietsch/Getty Images A cup of coffee in Culver City, Calif., in a file photograph. Kevork Djansezian/Getty Images

A cup of coffee in Culver City, Calif., in a file photograph. Kevork Djansezian/Getty Images

via Caspian News

via Caspian News

Recent comments