Futures Rebound On Fresh Bout Of Iran Optimism As Hyperscaler Earnings Loom

US equity futures rebound from Friday's selling, indicating a firmer start to the week with S&P futures rising 0.5% at 8.00am ET, and Nasdaq futures up 1% after a sluggish start to the session, after Iran’s Foreign Ministry said it had received proposals from mediators about the conflict with the US. In premarket trading, semis are higher as are Mag7 names; the AI theme is bid across sectors. Cyclicals are leading Defensives; both are higher in absolute terms, pointing to an ‘Everything Rally’ today. According to JPM, the US / Iran escalation is being faded with WTI lower pre-market and Brent off its highs. Bond yields are flat to up 1bp s the yield curve twists steeper. Commodities are mixed but net higher with US crude/natgas lower. The update from Iran has seen energy prices reverse gains with Brent now down 0.3% and on an $87/bbl handle. European stocks are now a touch higher with the Stoxx 600 up 0.1% Asian stocks were more mixed as a 4.5% plunge in the Kospi was offset by advances in China after two major state funds showed fresh purchases of domestic stocks. Bonds are still down but off session lows with Treasuries off by 3 ticks and yields up around 1bps across the US curve. The Bloomberg Dollar Spot Index has been choppy but ultimately flat with the greenback mixed versus G10 peers. Spot gold is up 0.1%, while silver rises 1.5%. Bitcoin has been on the back foot, down 0.5%. This week is a light macro data with the next Fed mtg on July 29, today we receive the Leading Index.

In premarket trading, Mag 7 stocks are mixed (Nvidia +1.1%, Alphabet (GOOGL) +0.3%, Tesla (TSLA) +0.8%, Amazon (AMZN) -0.01%, Apple (AAPL) -0.6%, Microsoft (MSFT) -0.6%, Meta Platforms (META) -0.3%

- AMC Entertainment (AMC) gains 16% after the theater operator posted revenue for the second quarter that beat the average analyst estimate. Shares of peer Imax (IMAX) climbs 3%.

- Domino’s Pizza (DPZ) rises 7% after the restaurant chain reported second-quarter revenue that beat analyst estimates. Chief Executive Officer Russell Weiner said the company “drove meaningful order count growth” during the period.

- Fervo Energy (FRVO) rises 4% as Jefferies upgrades to buy following the stock’s recent pull-back from its IPO highs.

- Global Payments (GPN) gains 1.7% as Morgan Stanley upgrades to overweight, citing constructive checks on Genius and Worldpay businesses.

- Hut 8 (HUT) rises 13% after the data center operator and Bitcoin miner announced a second 15-year lease for its Beacon Point data center campus in

- Nueces County, Texas, that’s valued at $9.8 billion.

- Iren (IREN) climbs 8% after the owner and manager of data centers powered by renewable energy raised its year-end AI cloud annualized run-rate revenue target to more than $4 billion.

- LXP Industrial Trust (LXP) climbs 3% as Brookfield Asset Management and CPP Investments agreed to buy the company in an all-cash deal valued at about $5.2 billion.

- Urban Outfitters (URBN) rises 4% as Goldman Sachs upgrades to buy noting upside to the stock as the UO brand recovery bolsters profitability.

- Yeti Holdings (YETI) is up 4% as Goldman Sachs upgrades to buy, saying the outdoor coolers and insulated bottle maker’s growth outlook is becoming more durable.

Futures are pointing to a positive start to cash trading as markets head into a week of contrasts: as Bloomberg notes, the economic calendar is sparse, but a deluge of earnings reports will test whether company results can match high expectations. S&P 500 futures were 0.5% higher as geopolitics once again dominated weekend news as fighting between the US and Iran escalated. Trump has remained silent so far on his next move, while average gas pump prices climbed back above $4 a gallon — a painful level for consumers. The next 2 weeks we get hyperscaler earnings, which are viewed as the next positive catalyst. As noted above, over the weekend US / Iran escalation is being faded with WTI lower pre-mkt and Brent off its highs, now below $90.

Investors “still think the US and Iran will go back to the negotiation table,” said Joachim Klement, head of strategy at Panmure Liberum. “Only once the US is no longer willing to negotiate do we expect markets to price higher oil prices for longer... The sentiment among investors remains positively biased, despite the setbacks in the tech space last week. This bodes well for renewed market stability this week.”

Still, stock index volatility is creeping higher as it catches up to much higher single stock vol, and demand for hedging is rising, with a measure of Skew jumping to its highest level since April — threatening to pull other volatility measures higher. Meanwhile, as Goldman noted overnight, extreme stock swings are tempting funds into reverse dispersion trades.

High volatility in AI stocks, a plunging momentum factor, and ultra-low correlations across S&P 500 stocks are reasons for renewed interest in investment themes outside AI, according to Goldman.

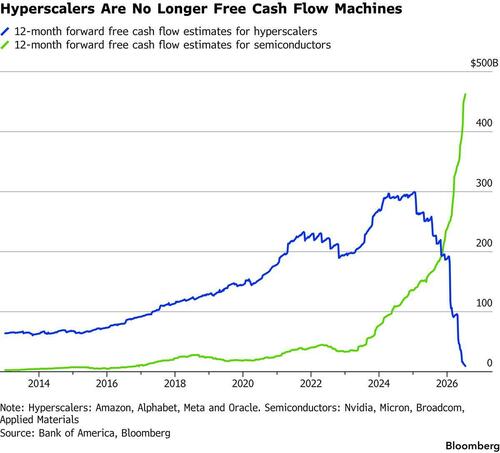

Meanwhile, pressure is building for the biggest spenders on AI to justify their expenditures to traders, with earnings reports over the next two weeks to be scoured for evidence that the investments are generating bigger returns. Ever the permabulls (since Kolanovich quit), JPMorgan strategists see AI-linked stocks as unlikely to remain under pressure for long, expecting strong earnings growth and improving valuations to reignite demand, led by semiconductor companies.

Meanwhile, last week's release of Moonshoot Kimi K3 AI model late last week was followed by Alibaba’s Qwen 3.8-Max preview over the weekend — suggesting competition in advanced AI models is broadening beyond US frontier labs.

Alphabet will kick off quarterly earnings from AI hyperscalers on Wednesday. The report comes at a time when chip stocks, the S&P 500’s biggest driver of 2026, have entered a bear market over worries that the likes of Alphabet won’t sustain vast outlays on the global buildout of AI infrastructure. “This week, we wait for the hyperscalers to report and especially pay attention to their monetization efforts and their capex intentions,” said Andrea Gabellone, head of global equities at KBC Securities. “This could calm the market.”

uropean stocks recoup initial losses with the Stoxx 600 little changed at 641.78 as Brent crude advances with the US and Iran engaged in a series of tit-for-tat attacks. Ryanair is one of the day’s biggest laggards, falling as much as 6.9% after the airline’s results were hit by rising oil prices and fare reductions. Here are the biggest movers Monday:

- Lagercrantz rallies as much as 5.9%, the most in two months, as the industrial conglomerate receives upgrades from SEB Equities, Pareto and Handelsbanken following its first-quarter result

- Munters advances as much as 6.3% after SEB and DNB Carneige upgraded their respective views on the Swedish industrial heating and air company to buy, while Jefferies reiterated its buy rating

- DocMorris rises as much as 5.1%, the most in nearly a week, after the stock was upgraded to neutral from sell at UBS, which cited “a more constructive view” on the online pharmacy’s margin prospects

- PolyPeptide gains as much as 5.8% to CHF44.15 after Samsung Biologics agreed to acquire the Swiss contract drugmaker in an all-cash deal, with analysts saying the deal is fairly valued overall

- Fresenius shares advance as much as 2.5% as Deutsche Bank sees potential for an upgrade to earnings guidance when the German health-care company reports results next month

- Prysmian rises as much as 2.8% after the Italian company signed a 10-year agreement with Koch Inc.’s Molex to supply optical cables to data centers. Such a deal had been long awaited and is likely to reassure investors, analysts say

- Ryanair shares drop as much as 7.6%, the most since March, after a significant dip in first-quarter profit compared to the previous year as conflict in the Middle East lifted oil prices and impacted demand

- Nokian Renkaat falls as much as 10% after Nordea cut the tiremaker to sell from hold following its recent strong run. Analysts said the 10% year-on-year volume increase for the second quarter “cannot be maintained for long”

- Belimo shares drop as much as 9%, hitting a two-month low, after strong results from the heating and ventilation specialist were offset by its failure to explicitly reiterate its revenue guidance

- Segro shares fall as much as 1.9% to 880p each after the UK warehouse landlord rejected a third proposal from Prologis, which valued the stock at 993p, or about £13.5 billion for the whole company

- Corbion shares fall as much as 5.4% after Oddo BHF cut the food and chemicals ingredients producer to neutral. Analyst Robert Jan Vos said he sees a “real risk” of a profit warning at the July 31 earnings announcement

- Clariant shares fall as much as 5.2% after Morgan Stanley cut its recommendation on the Swiss chemicals company to underweight from equalweight, seeing continued pressure on earnings due to the Middle East conflict

Asian stocks were mixed as South Korean equities were led lower by chip stocks, while Chinese equities were bolstered after state funds revealed fresh purchases. The MSCI Asia Pacific Index swung between small gains and losses. Korea’s Kospi slid as much as 5.1% after being closed on Friday for a public holiday, with chipmakers Samsung Electronics and SK Hynix the biggest contributors to its decline. Chinese shares rose following last week’s rout, after two major state funds said they made fresh purchases and as regulators are set to meet with key industry participants. Japanese markets are shut for a holiday. Korea’s sharp swings “show that AI and semiconductor de-risking is not over,” said Charu Chanana, a chief investment strategist at Saxo Markets. “China tech is offsetting some of the regional weakness, but this is not a broad Asia risk-on move.” “Cheaper and more efficient Chinese AI is raising the bar for US Big Tech ahead of earnings: talking about another increase in capex may no longer be enough.” Asian sectors to watch

- Chinese coal and oil stocks jumped as the US and Iran continued to escalate back-and-forth attacks, heightening to the need to secure energy supplies outside the Strait of Hormuz.

- Kweichow Moutai’s shares rise as much as 2.6% after the liquor maker announced price increases, a move that analysts say is intended to defend margins and spur more direct-to-consumer sales.

- Chinese optical stocks rally after several major companies delivered solid 1H preliminary earnings.

- Chinese molybdenum stocks jump after CCTV reports on surging prices, tight supply and potential growth outlook.

- Shares of Alibaba gain as much as 5.4% in Hong Kong after releasing a preview version of its flagship Qwen3.8 Max model, describing it as second only to Anthropic’s Fable 5.

- Shares linked to Chinese battery makers mostly decline after the nation said it plans to impose a consumption tax for products including lithium-ion batteries and solar cells.

- Asian energy shares follow oil higher after fresh attacks across the Middle East resulted in the US announcing the death of a third service member in the past two days.

In FX, the Bloomberg Dollar Spot Index has been choppy but ultimately flat with the greenback mixed versus G10 peers.

In commodities, news that Iran’s Foreign Ministry said it had received proposals from mediators about the conflict with the US sent energy prices lower with Brent now down 0.3% and on an $87/bbl handle. Bonds are still down but off session lows with Treasuries off by 3 ticks and yields up around 1bps across the US curve. Spot gold is up 0.1%, while silver rises 1.5%. Bitcoin has been on the back foot, down 0.5%.

The only item on today's economic calendar is at 10:00 am when we get the June Leading Index, est. -0.09%, prior 0.1%.

Market Snapshot

Top Overnight News

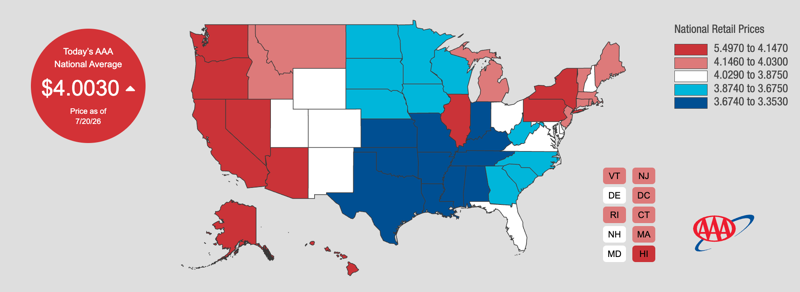

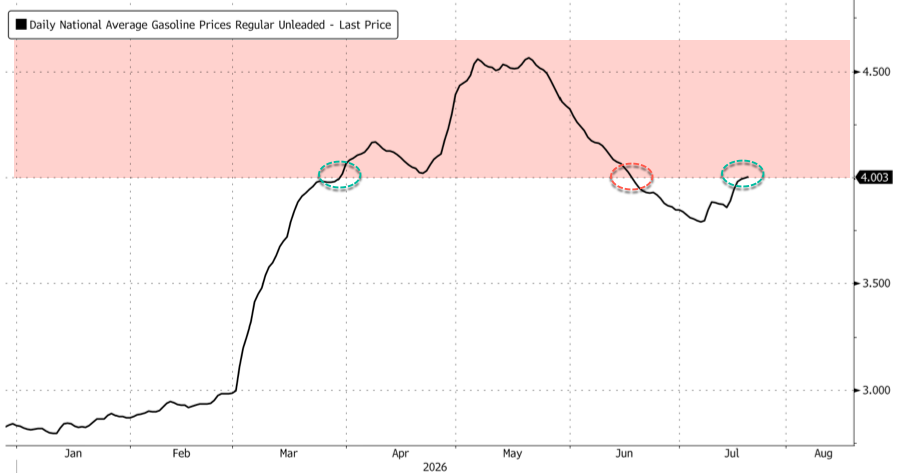

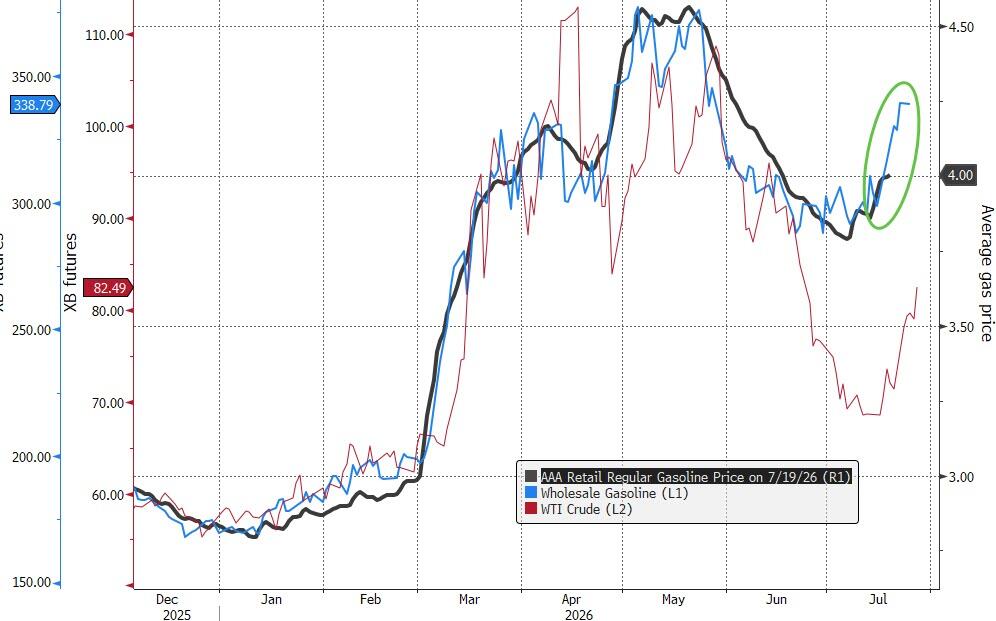

- U.S. gasoline pump prices crossed the $4 a gallon mark on Monday as renewed hostilities between the U.S. and Iran further disrupt energy flows through the Strait of Hormuz, a critical route for global oil supplies. National average retail gasoline prices have climbed more than 30% since the U.S. and Israel attacked Iran at the end of February. The average pump price on Monday was $4.0030 a gallon, according to AAA data. ReutersChina’s “national team” of funds stepped into the equity market and made sizeable purchases in an attempt to bolster prices following last week’s slump. FT

- Chinese officials will contemplate stimulus measures, including accelerating bond issuance, after GDP fell below the government’s target range in Q2. FT

- Iran’s currency has sunk to record low levels vs. the USD as the country’s economy comes under further strain. FT

- Iraq is using a vast fleet of trucks to carry fuel oil through Syria and reroute flows away from the Strait of Hormuz. BBG

- Moonshot is getting ready for a Hong Kong IPO in as early as the next six months as it looks to tap capital markets after wrapping a fundraise that may value it at more than $30 billion BBG

- Hong Kong is considering extending equity trading hours to align with most global markets, including a proposal to eliminate the lunch break. BBG

- Andy Burnham was named the UK’s Prime Minister today, the country’s seventh premier in just over a decade. BBG

- TSMC is adding $100 billion to its investments in Arizona to meet strong US demand and ward off rivals, CFO Wendell Huang said, after beating profit expectations last quarter. BBG

- US President Trump posted "Wonderful news! I have just been informed that Giant Eagle, a GREAT American Grocery Company, will be lowering prices, by a lot, across more than 300 products this Summer, through Labor Day, to help hardworking American families".

Top Iran News

- US and Iran engaged in another exchange of strikes after an Iranian attack on Jordan killed two US service members on Friday, while Tehran said it was suspending its commitments under the interim peace deal as strikes ramped up.

- US President Trump said we hit Iran very hard again tonight and hit Iran in honour of probably three patriots who died, adding we are ending any chance of Iran having a nuclear weapon.

- US Central Command announced the ninth consecutive evening of strikes against Iran, in which targets included Iranian military command centres, air defence and coastal surveillance sites, maritime capabilities, missile and drone launch sites, and communication networks, to further diminish Iran's ability to attack commercial vessels and civilian mariners transiting the Strait of Hormuz. CENTCOM also announced it redirected 6 commercial vessels and disabled 1 to ensure full compliance, as of July 19th.

- Explosions were heard in Iran's Tabriz and the city of Jask in the Hormozgan province in southern Iran, while explosions were also reported in Sirik and Khormoj, southern Iran. Furthermore, there were explosions in Delijan in the southern Markazi province and Arak in western Iran, while air defences were activated in Konarak city, Sistan and the Baluchestan province in southeastern Iran.

- Iran launched missiles from its Lorestan province in western Iran towards enemy targets, and blasts were reported at US bases in Kuwait and Bahrain, while explosions were also reported in the UAE's Ras Al-Khaimah.

- US is said to be planning for a wider war, according to a US official familiar with internal administration discussions, cited by The Washington Post.

- US Secretary of State Rubio said the US remains open to a diplomatic resolution regarding Iran, while Rubio also stated that his meeting with the Lebanese President was very positive.

- Iran’s nuclear agency condemned a US attack on the site of the nuclear power plant under construction in Darkhovin, which it said violated international law, according to Mehr News Agency, although it didn’t mention when the strike took place.

- Iran's Deputy Foreign Minister Gharibabadi said the US strike on the under-construction power plant was a dangerous attack on Iran's peaceful infrastructure, and the US must bear full responsibility for any escalation and the resulting insecurity and instability.

- IRGC said it destroyed 20 warehouses used by US forces in the Azraq region of Jordan, resulting in the deaths of dozens of soldiers, according to Al Jazeera Mubasher.

- IRGC said two ships were involved in an “accident” after attempting to transit the Strait of Hormuz via an unsafe route, and that two other vessels abandoned the route, while it warned that vessels influenced by the US and entering unsafe routes will certainly face accidents. It was later reported that IRGC said two oil tankers were blown up after attempting to transit the southern route in the Strait of Hormuz.

- UKMTO said it has received a report of the incident eight nautical miles northwest of Oman's Khumsar, with a vessel on fire, but the cause has not been verified yet.

- Tehran Times noted reports of an unprecedented rise in opposition to the war within various ranks of the US military, while it noted that refusals by US personnel to carry out orders from superiors are increasing at an unprecedented rate, citing multiple intelligence sources.

- Kuwait's Defence Ministry said Iran conducted sustained strikes against civil and critical infrastructure on Kuwaiti territory, which caused multiple fires and severe damage.

- Iranian Foreign Ministry spokesperson Baghaei said negotiations with the US could be pursued based on national interests and that intermediaries have shared messages with Tehran in recent days. Mediators are continuing their efforts to prevent escalation, and we have received proposals from them, but we will not go into details now. He added that they will not abandon talks with the US but Iran's sovereign rights over the Strait of Hormuz are non-negotiable.

- Al Jazeera source in Pakistan's Interior Ministry said the Iranian Interior Minister arrived in Pakistan's capital Islamabad today. Iran and Pakistan will hold extensive consultations on border management, cross-border security and the implementation of the Islamabad MoU, alongside other issues of mutual concern, Journalist Mallick reported.

- The Yemeni Armed Forces said an announcement of an important position to be released at 3pm Sana'a time (13:00BST).

- Explosions were sounded in Isfahan, however reports state they were caused by controlled explosions. Additionally, Iran's Bushehr Governor said Bushehr was targeted twice by the American enemy.

- Unofficial reports indicate that one drone struck the grounds of Kuwait's main power plant, Tasnim reported

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded somewhat mixed following the US-Iran escalation over the weekend, in which the sides ramped up their strikes after two US service members were killed during an Iranian strike on Jordan, while key participants were away owing to the holiday closure in Japan for Marine Day. ASX 200 was rangebound with light pertinent catalyst and a lack of data releases overnight. KOSPI underperformed as the tech-related losses late last week caught up with the index on return from a 3-day weekend, while South Korea had temporarily banned new listings of single-stock leveraged ETFs tied to tech companies like Samsung Electronics and SK Hynix to curb extreme market volatility. Hang Seng and Shanghai Comp rallied with strength seen in energy and tech-related stocks amid higher oil prices and reports that launched a preview of its flagship Qwen3.8 Max model, which is said to be comparable to leading frontier AI models. Furthermore, the PBoC maintained its benchmark LPRs for the 14th consecutive month, while China’s leaders are expected to decide on additional stimulus measures at the Politburo meeting this month.

Top Asian News

- HKEX is reportedly mulling longer stock trading hours, and scraps lunch break.

- China’s top leaders are expected to decide on additional stimulus measures this month following a sharp slowdown in Q2 GDP, with leaders expected to focus on speeding up bond issuance at their next Politburo meeting, expected to take place during the final week of July, according to FT.

European equity futures are mixed, following on from a similar theme seen across APAC indices. Early morning action saw indices broadly subdued, reacting to the latest round of US-Iran strikes, where Iran officially suspended its cooperation in the Islamabad MoU. However, the Iranian Foreign Minister lifted sentiment after he stated that negotiations with the US could be pursued, based on national interests; he added that intermediaries shared messages with Tehran in recent days. This spurred some mild upticks across European indices. European sectors hold a very slight negative bias. Energy unsurprisingly takes the top spot, given the aforementioned geopolitical developments. Tech and Media complete the top three. The tech strength comes in contrast to the underperformance seen in APAC trade, whereby the likes of Samsung (-4.3%) and SK Hynix (-4.2%) both extended lower. No particular driver for the strength seen across European tech names, but potentially some positioning into a busy tech-earnings slate this week. To the downside, Travel & Leisure has been dragged down by a) elevated energy prices, b) Ryanair earnings. On the latter point, Ryanair extends lower by c. 5.9%, after reporting a miss on its headline metrics and sees lower summer fares citing waning demand. It also suggested that it has no visibility for H2, amidst the ongoing Iran uncertainty.

Top European news

- UK’s Andy Burnham is to drop plans for a digital ID in a ‘reset of priorities’ and will focus on cost-of-living policies, when he becomes PM on Monday.

FX

- 2G10s are mixed, but mostly firmer against the Buck with FX-specific catalysts light, and geopolitics not giving much of a bias. Antipodeans lead after reports of potential Chinese stimulus, GBP performs well into Burnham's appointment as PM.

- USD continues to be driven by geopolitics, with the Greenback reversing earlier gains in tandem with energy benchmarks after Iran’s Foreign Ministry noted the nation is open to returning to talks. Aside from this, fresh drivers are light with last week’s inflation (PPI/CPI) in focus ahead of PCE, with the data slate light in the remainder of this week. DXY saw a modest bid at the Sunday re-open to a 100.80 peak, though reversed as mentioned, to a 100.65 trough.

- Burnham is set to become UK PM after midday today. The main focus for GBP is whether he confirms Mahmood as Chancellor, after UK press widely reported last week that she would take the job, alongside any remarks around public control in the water/energy sector, and how this would be funded. Sterling is one of the best G10 performers today, sitting around 0.85 in the EUR cross and below 1.35 in Cable. The UK calendar today is light; the week sees LFS and Inflation data.

- Antipodeans are the best performers alongside a broad bid in Chinese assets, where its leaders are expected to decide on additional stimulus measures at the Politburo meeting this month. AUD/USD, NZD/USD +0.3%.

Fixed Income

- Global fixed income benchmarks are softer across the board, but are off their worst levels following recent remarks by the Iranian Foreign Ministry spokesperson Baghaei, who noted that negotiations with the US could be pursued based on national interests, that intermediaries have shared messages with Tehran in recent days and that Iran will not abandon talks with the US. This constructive rhetoric by the spokesman comes amid a ninth straight day of strikes between the US and Iran. Iran killed two service members in Jordan and one in Iraq over the weekend, while the US continued to target Iranian military capabilities.

- Gilts (-16 ticks) are in focus today as Labour leader Burnham is set to become PM. He is to meet the King around noon to accept his appointment and then give his first speech between 12:30-13:00BST in front of 10 Downing Street. Although this will be widely watched, the key will be on who he appoints as the Chancellor. It has been widely touted that the current Home Secretary, Mahmood, will be given the role of Chancellor. Analysts see the 2s-30s curve flattening if Burnham's choice of chancellor aligns with market expectations, given Mahmood is seen as fiscally prudent.

- Bunds (-8 ticks) follow the broader space higher, given the recent fall in energy prices. This week's focus will be on the ECB policy announcement on Thursday, in which the Bank is expected to keep rates steady at 2.25%, with only a 16% chance of a hike in July. However, analysts continue to see further hikes in 2026, with 22bps priced in for a hike in September.

- USTs (-3 ticks) have returned to their opening price, trading at the upper end of their 109-00+ to 109-06 range. Not much on the docket this week, given Fed officials are on blackout ahead of their policy meeting.

Commodities

- WTI and Brent Front-month futures are off their best levels after opening higher overnight in reaction to the military escalation, before waning in early European hours on continued efforts for diplomacy. To recap, the US and Iran ramped up their exchange of strikes following the death of a couple of US service members due to Iran attacking Jordan on Friday, while CENTCOM announced the 9th consecutive night of strikes against Iran, and Iran continued to retaliate against US interests and allies. Thereafter, initial weakness this morning emanated from reports that Pakistan's Interior Ministry says the Iranian Interior Minister arrives in Pakistan's capital, Islamabad, today. The downside was further exacerbated by commentary from Iranian Foreign Ministry spokesperson Baghaei, who said negotiations with the US could be pursued based on national interests; Intermediaries have shared messages with Tehran in recent days. Further, the Iranian Foreign Ministry said it will not abandon talks with the US, but Iran's sovereign rights over the Strait of Hormuz are non-negotiable.

- Price action this morning has largely followed headlines. Brent Sep’26 hit an overnight peak of USD 91.42/bbl before moving back to lows of USD 87.72/bbl. Similarly, WTI Sep’26 notched a current high at 84.60/bbl before falling to a USD 81.11/bbl trough at the time of writing. Ahead, there could be some risk around 13:00BST as the Yemeni Armed Forces said “an announcement of an important position” will be made at that time.

- Precious metals remain in a narrow range but have lifted off worst levels in tandem with the Dollar easing in lockstep with oil. Spot gold resides in a USD 3,982-USD 4,030/oz range. Spot silver has picked up momentum in recent trade, back on a USD 57/oz handle vs lows of USD 55.50/oz.

- Base metals are mixed and continue with similar price action seen during APAC hours. Copper futures eke out mild gains alongside the outperformance in red metal's largest buyer overnight.

- Iraq's SOMO is reportedly looking to buy Aug-Sep gasoil deliveries, according to documents.

- Syria has emerged as a regional hub for Iraqi fuel oil exports, with more than a quarter of Middle East fuel oil shipments transiting Syrian Mediterranean ports, according to the Syrian state news agency.

- Oil loadings at the Caspian Pipeline Consortium’s terminal on the Black Sea coast were suspended following a drone attack.

Trade/Tariffs

- US President Trump said maybe Canada should pay some damages for wildfires, and that he spoke with Canada's PM Carney regarding the fires, while Trump added that they have a good relationship with Canada and have no tension with anybody regarding trade.

- UK trade negotiators made last-minute concessions to India that could undermine Tata Steel UK’s Llanwern plant in Newport, to secure a much-lauded trade deal, according to some industry insiders cited by FT.

Geopolitics

- Russia and Ukraine exchanged fresh strikes on warehouses and ports over the weekend.

- Ukrainian President Zelensky said that they struck three oil depots in Russia’s Stravpol region, while Foreign Minister Sybiha said Russia conducted its largest ballistic missile barrage against Kyiv since the beginning of the Russia-Ukraine war, involving around four dozen ballistic missiles.

- Moscow's Mayor reported overnight drone incidents, and TASS estimated that the attempted drone attack on Moscow is one of the largest in several years, while Russian authorities said that 400 marches were launched towards Moscow although most were neutralised.

- Russia's Salavat refinery has reportedly restored some of its damaged capacities following a drone strike.

- EU is facing a collapse in support for new economic sanctions against Russia, with members refusing to back measures that could damage their corporate champions, according to FT citing diplomats.

US Event Calendar

- 10:00 am: Jun Leading Index, est. -0.09%, prior 0.1%

DB's Jim Reid concludes the overnight wrap

From the World Cup to "Mapping the World’s Prices 2026", released last week and already attracting extensive global coverage along with more than 30,000 downloads. The standout theme from this year’s edition is just how inexpensive Japan has become, although the report is packed with data across 69 financially important cities worldwide. You can find the report here at the Deutsche Bank Research Institute.

Just as you thought it was safe to relax into the summer, last week brought a reminder that there remain some big unresolved themes that could become an issue in thin summer liquidity. Brent saw its largest weekly increase (+15.9%) since April as the US and Iran continued to exchange blows, with European natural gas seeing its highest close since March.

Over the weekend, the conflict has intensified markedly, with a fresh wave of tit-for-tat attacks underscoring how quickly the situation is deteriorating. Three US service members were killed in separate incidents in Jordan and Iraq, while US strikes hit targets including Qeshm Island and multiple locations in southern Iran. At the same time, Iran broadened its retaliation beyond military sites, targeting critical infrastructure across the Gulf, including power and desalination facilities in Kuwait, as well as launching drone and missile attacks towards US bases and regional allies. And prospects for any diplomatic breakthrough remained dim, with Iran’s Foreign Minister Araghchi suggesting that some nuclear issues may “remain unresolvable”.

Tensions also escalated further in the Strait of Hormuz, with Iran signalling a far more assertive stance over shipping flows and claiming to have intercepted vessels attempting to transit the waterway.

In response, this morning Brent is up +2.45% to $90.26/bbl after a ninth consecutive night of US strikes against Iran. Given the escalation US futures are performing relatively well with S&P (+0.15%) and Nasdaq (+0.47%) contracts higher. In Asia markets are generally higher but the KOSPI (-3.22%) continues its wild ride, though has improved from being down -5% as I’ve been writing this.

Chinese related equities are strong, with the Hang Seng (+2.04%), CSI 300 (+1.55%) and Shanghai Composite (+1.18%) all higher. Elsewhere the S&P/ASX 200 (+0.17%) is edging higher, and Japanese markets are closed today for the Marine Day holiday. This means no cash US Treasury trading but bond futures are down on the higher oil prices.

Staying in Asia, concerns continued to mount over the competitive progress of China’s AI ecosystem last week. We’ve been tracking the rapid climb of Chinese models and token use in various CoTDs with data updated in the WOW! pack (link here) showing the intelligence vs cost comparison of US and Chinese models. Chinese labs are seemingly catching up fast.

The micro implications are as important as some Chinese models are being priced at levels broadly comparable to mid-tier US models (e.g. Anthropic Sonnet), despite performance that approaches higher-end systems, implying a materially lower cost-to-intelligence ratio. That challenges the economics of the current US-led AI stack, where frontier capability has been associated with very high compute and capital intensity. A key differentiator is approach: Chinese models are increasingly released as open-weight systems, allowing developers and enterprises to download, modify and run them locally, whereas US leaders have largely pursued closed, proprietary models delivered via APIs. This open approach accelerates adoption, innovation and cost competition, as it decentralises development and reduces reliance on a small number of providers, but also undermines pricing power and control. The immediate market reaction—pressure on AI and semiconductor names—reflects a reassessment of whether the industry’s current capex trajectory is sustainable if similar performance can be delivered more cheaply. More broadly, successive Chinese releases are eroding the scarcity premium embedded in proprietary models, accelerating a shift toward commoditisation, tighter margins and faster global diffusion as open-weight systems lower barriers to entry.

At the macro level, this could encourage faster, wider and cheaper adoption of AI which will be more positive for productivity. However, it also raises the risk of a capex overcycle in the US if returns on AI infrastructure come under pressure, while also intensifying geopolitical fragmentation as competing technology stacks evolve. So an absolutely fascinating development to watch. It’s hard to underestimate its importance.

Back to the more mundane, and for the week ahead, the ECB decision on Thursday and the global flash PMIs on Friday will be the main macro highlights. Alongside this, a new Prime Minister in the UK today, and a heavy run of global earnings will keep markets busy, with key reports from Alphabet, Tesla, Intel, SK Hynix and SAP, among others, offering an important read on tech as we see a major wobble in the sector.

In the US, the calendar is comparatively quiet, with Fed officials in blackout ahead of the upcoming FOMC meeting next week. Thursday brings initial jobless claims, which we expect to continue signalling a stable labour market, consistent with the recent downward trend in both initial and continuing claims. This week’s release coincides with survey week for payrolls, which gives it slightly more importance. On Friday, the July flash PMIs will be the main focus.

The week begins today with the UK seeing a change in leadership as Andy Burnham takes office as Prime Minister, with ministers beginning to be appointed, and policy plans starting to take shape. Tomorrow, UK labour market data will be released, followed by Wednesday’s June inflation report, where our UK economist expects headline CPI to ease to 2.70% year-on-year, core CPI to 2.55%, and services inflation to moderate to 3.45%. The UK week concludes on Friday with retail sales, the GfK consumer confidence index, and the Bank of England’s DMP survey, all of which will provide further colour on the consumer backdrop. Elsewhere in Europe, tomorrow sees the release of the German and Eurozone ZEW surveys, while Thursday’s ECB decision is the key focal point. Markets are currently pricing a hold, which aligns with our European economists’ expectations, with a further rate increase more likely in September. The ECB will also publish its bank lending survey tomorrow and its consumer expectations survey on Friday, offering additional insight into credit conditions and inflation expectations.

In Asia, the main focus will be on Japan, where Wednesday’s trade balance will provide an update on external dynamics, followed by Friday’s national CPI. Our Japan economist expects core CPI to rise to 1.7% year-on-year, with core-core inflation edging up to 1.9%, pointing to a gradual firming in underlying price pressures. Elsewhere, Australia’s labour force survey on Thursday will be the key regional release.

Finally, the Q2 earnings season accelerates significantly over the week. Momentum gets going tomorrow with a broad set of financials and industrials reporting including Novartis, Charles Schwab and General Motors. Wednesday is one of the busiest days, with major technology names such as Alphabet and Tesla reporting alongside IBM, ServiceNow and Texas Instruments, as well as a range of European corporates including Banco Santander and Deutsche Boerse. Thursday continues the heavy flow with Intel, SK Hynix and SAP among the highlights, alongside a wide range of US and European names including Roche, Nestlé, Lockheed Martin and BNP Paribas. The week concludes on Friday with results from American Express, NextEra Energy and Verizon, among others.

Recapping last week now, geopolitics remained top of the agenda for markets, with a sharp rise in oil prices as the strikes between the US and Iran showed no sign of easing. Indeed, Brent crude oil prices ended the week up +15.91% (+4.59% Friday) at $88.10/bbl, marking their biggest weekly jump since April. So that revived fears about a more persistent inflation shock, particularly with European natural gas prices also rising, and the front-end future rose +19.95% last week (+5.79% Friday) to its highest level since March at €58.01/MWh.

Geopolitical fears also interacted with fresh concerns around the AI trade, which meant that equities took a hit around the world. That was particularly clear for chip stocks, with the Philly semiconductor index down -9.97% last week (-1.63% Friday), marking its biggest weekly decline since the week of the Liberation Day tariff announcements last year. Moreover, that meant the index moved into a bear market, having now shed -20.23% since its closing peak back on June 22. In turn, that coincided with other equity declines, with the S&P 500 down -1.55% (-1.01% Friday), and Japan’s Nikkei also had its biggest decline since the week of Liberation Day, falling -6.44%. However, European equities were relatively resilient, with the STOXX 600 up +0.07% over the week (-0.34% Friday).

As all that was going on, US Treasuries rallied last week thanks to a softer than expected US CPI print. So that meant investors priced out the chance of a July rate hike, which fell from 34% to 14% over the course of the week. Meanwhile, the 2yr Treasury yield fell -2.9bps (+3.8bps Friday) to 4.18%, and the 10yr Treasury yield fell -1.3bps (-0.5bps Friday) to 4.55%. But whilst inflation fears fell back in the US, they returned strongly in Europe thanks to the rise in energy prices, with the 1yr Euro inflation swap up +46.9bps last week to 2.50%. So sovereign bond yields moved higher across the continent, with the 10yr bund yield up +6.0bps (-0.8bps Friday) to 3.12%.

Finally, the dollar index weakened -0.19% last week, as investors dialled back the prospect of an imminent Fed rate hike, while gold fell below $4,000 for the first time this year before ending the week at $4,017/oz (-2.49% on the week). Otherwise, credit spreads mostly widened, with US IG (+1bps) and HY (+2bps) spreads rising marginally, along with Euro IG (+1bps) and HY (+3bps).

Tyler Durden

Mon, 07/20/2026 - 08:33

President Donald Trump speaks at the White House in Washington on July 6, 2026. Anna Moneymaker/Getty Images

President Donald Trump speaks at the White House in Washington on July 6, 2026. Anna Moneymaker/Getty Images

A home for sale in Alhambra, Calif., on Aug. 28, 2025. Frederic J. Brown/AFP via Getty Images

A home for sale in Alhambra, Calif., on Aug. 28, 2025. Frederic J. Brown/AFP via Getty Images

Reuters: Smoke billows after Ukrainian drone attacks in Podolsk, Moscow Region.

Reuters: Smoke billows after Ukrainian drone attacks in Podolsk, Moscow Region. via Middle East Eye

via Middle East Eye

Recent comments