What's Behind The Plunging Won And Sudden Liquidity Collapse In Korean Markets

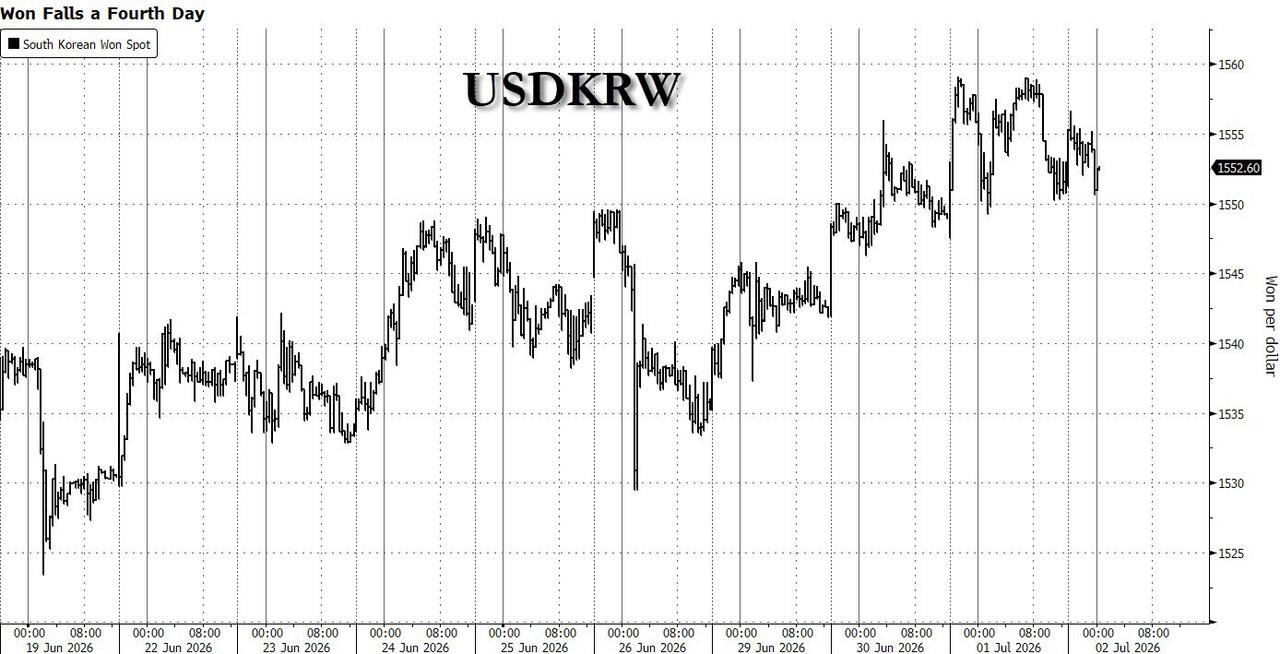

South Korea’s won weakened for a fourth day as overseas investors accelerated their relentless sales of local stocks.

In response, USD/KRW rose 0.1% to 1,552.60, extending its four-day gain to 1.2% (i.e. KRW drop).

According to Barclays, pressure from both resident outflows and more recently in the case of Korea, heavy foreign outflows, could pose further headwinds even as exports performance remains robust and domestic equities extend their bubble.

Let's take a closer look at what's driving the key moves in Korea.

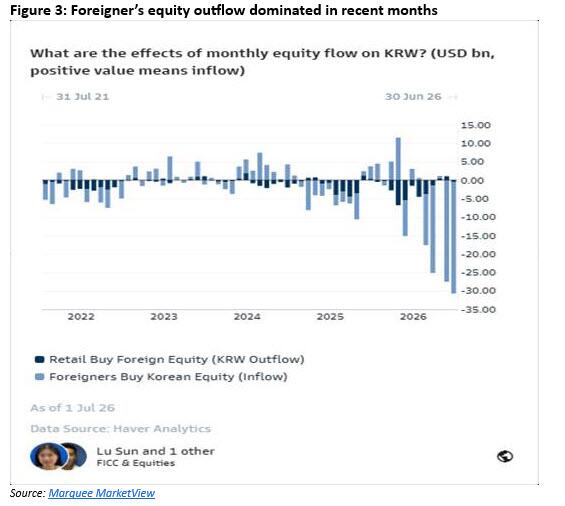

Why was USDKRW higher?Other than stronger USD, Goldman has been highlighting that rebalancing related equity outflow has been the dominating factor. Equity outflow from Jun 22nd till month-end amounted to US$18bn, bringing total Jun equity outflow to US$30bn. This follows the US$27bn outflow observed in May. As of today, Samsung and Hynix are 32% and 30% of MSCI Korea respectively, which are 7% and 5% above the 25% single stock limit. A combined 12% rebalancing effort would lead to another US$24bn outflow with US$200bn AUM (passive and active) estimated tracking MSCI Korea.

Additionally, other portfolio concentration limits such as UCITS and HF internal concentration limit rule are also likely to be driving the rebalancing related outflows. In terms of timing, some fast money rebalancing is relatively real time, while many real money and passive investors may rebalance at quarter-ends which led to more concentrated outflows.

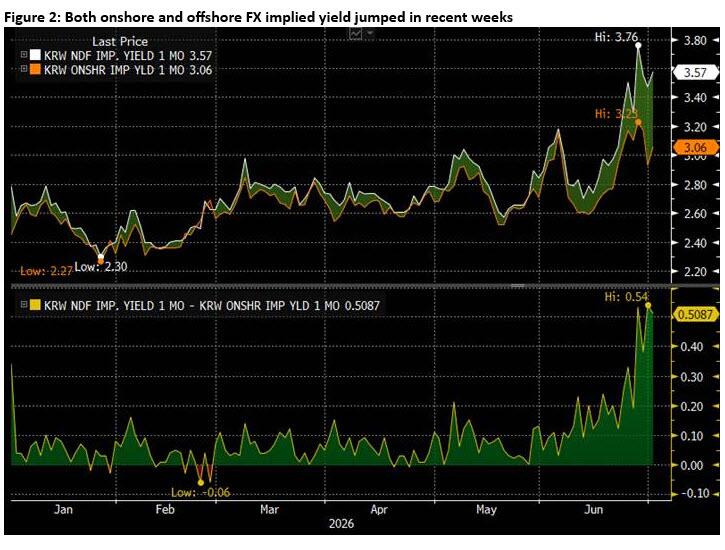

FX hedging need by foreign investors drove RHS USDKRW demand. Goldman estimates average foreigners’ FX hedging ratio for Korean equities to be 10-15%, and the hedging mainly happens in offshore NDF market. As of March-end, foreigners’ exposure to Korean equities was US$1tn. Due to the 68% expansion in market cap in KOSPI in Q2, the associated FX hedging need rose by an estimate of US$68-US$102bn (US$1000*68%* 10-15%) during the quarter. This has led to sharp increase in RHS NDF hedging demand, some of which concentrated at quarter end as well.

Other than above-mentioned hedging dynamics, FX hedging demand by USD-denominated total return swaps with leveraged equity underlying provided to offshore clients by local security houses via intermediaries also likely added to FX hedging demand in NDF market, especially as equity marketcap expanded quickly in Q2.

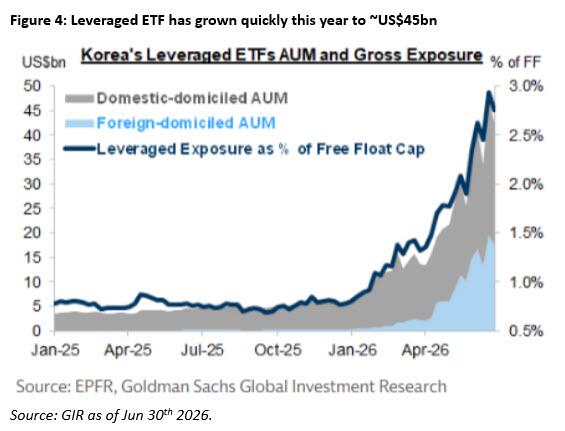

Why did liquidity tighten?- Sharp rise in borrowing by securities firm was likely the main driver behind tighter onshore liquidity. Surge in onshore retail margin trading and leveraged single-stock ETFs caused sharp rise in funding needs of local securities firms. In particular, with leveraged ETF, the need to post futures margin for hedging positions for securities firms drove the borrowing demand.

- Local news reported securities firms’ commercial paper and short-term bonds issuances exceeded KRW100tn each month and accounted for 80% of short-term bond issuance in recent months.

- Decline of collateral value for securities firms facing offshore counterparties worsens the liquidity situation. When local securities firms face offshore intermediaries on total return swaps, they not only have rising needs to post margins from underlying stock advance, but also from declining collateral value as KRW FX depreciated and KTB sold off. These dynamics further increased securities firms’ margin requirement in KRW terms, which in turn added to their local borrowing demand. Similar situation happened in late 2022 with KRW and KTB sold off sharply at the same time during BOK hiking cycle. Looking forward, local news reports Samsung securities plans KRW600tn short-term issuance in Jul, indicating such liquidity tightness is unlikely to ease.

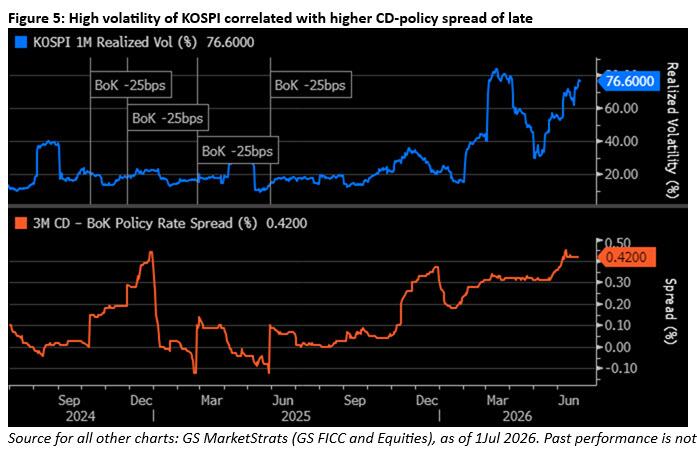

- Forthcoming BOK hike (starting in Jul per GIR base case) likely also added to the expectation of higher funding costs ahead.

- Goldman has observed widening of spread between NDF curve offshore and onshore FX swap. This could be a result of unwinding onshore-offshore arbitrage positions as RHS hedging demand caused sharp surge in NDF points.

Looking ahead, if Korean equity continues to charge higher in a volatile fashion, combined with likely BOK hikes, Goldman thinks such liquidity environment is likely to stay or tighten further. Thus NDF points are likely to stay elevated and the bank prefers pay on dip. In a strong USD environment, KRW FX pressure is unlikely to ease from external forces, which does not help NDF points to fall either. On the other hand, if Korean equities fall meaningfully, NDF points may retrace, as smaller notional exposure to Korean equities by foreigners (either direct or leveraged) would reduce the associated FX hedging.

On FX spot, it is much harder to see sustained equity inflow in the short term: If Samsung/Hynix continue to lead KOSPI higher, equity rebalancing related outflow would further dominate; if equities fall, broad-based outflow is likely to follow which is likely to offset the positive FX impact from unwind of RHS hedging. Only when equities fall substantially so that Samsung & Hynix’s market cap fall under the concentration limits, a recovery from there may attract inflows.

Thus equity outflow may continue to weigh on KRW in the near future.

As market unwinds debasement trades and USD remains resilient, Goldman expects USDKRW may further rise gradually, with authorities’ various smoothing efforts help to limit the speed of KRW depreciation. Although Korean exporter USD selling is expected to rise as export grows organically and domestic capex expands, given current exporter conversion is already relatively high, Goldman expects large and volatile equity related flows to remain dominant for USDKRW path ahead.

Tyler Durden Thu, 07/02/2026 - 00:41

Getty Images

Getty Images

Democratic socialist Melat Kiros (L) ousted 15-term Rep. Diana DeGette in Tuesday's Democratic primary

Democratic socialist Melat Kiros (L) ousted 15-term Rep. Diana DeGette in Tuesday's Democratic primary

via Atlantic Council

via Atlantic Council

Recent comments