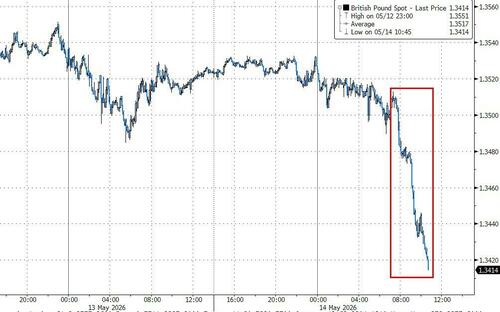

Cable Crashes As Burnham Signals Challenge To UK PM Starmer

Update (1345ET): Following Wes Streeting's earlier resignation "having lost confidence" in Starmer's leadership, the UK PM is now under further pressure as Andy Burnham opened a possible path to challenge Keir Starmer for the prime minister’s job, after a Labour member of Parliament resigned and urged the Greater Manchester mayor to run for his seat.

Andy Burnham

Bloomberg reports that the MP, Josh Simons, announced plans to step down from his Manchester area seat, freeing up a House of Commons constituency that Burnham would need to mount a bid to become leader of the governing Labour Party.

“I am standing aside so that Andy Burnham can return to his home, fight to re-enter Parliament, and if elected, drive the change our country is crying out for,” Simons wrote.

“Nothing short of urgent, radical, courageous reform will make a difference.”

With UK bond markets closed, the outlet for positioning after this headline (and the anxiety over "radical reform") was the FX market and cable plunged on the news...

Burnham separately said he would seek permission from Labour’s National Executive Committee, a panel dominated by Starmer loyalists that blocked a similar bid earlier this year.

“Much bigger change is needed at a national level if everyday life is to be made more affordable again,” Burnham said in a statement to Manchester Evening News.

“This is why I now seek people’s support to return to Parliament: to bring the change we have brought to Greater Manchester to the whole of the UK and make politics work properly for people.”

There will be several hurdles standing in Burnham’s way. Starmer’s allies on Labour’s governing body blocked him from contesting a seat in the Manchester area when it became vacant earlier this year, citing the need to avoid a costly election for the mayoral post he would have to vacate. They could do so again.

* * *

With UK PM Starmer's leadership under increasing scrutiny, UK Health Secretary, Wes Streeting, has issued a statement via social media that he is resigning his post.

Wes Streeting

Streeting says that while there are good reasons to remain in post, he has lost confidence in Starmer’s leadership:

"As you know from our conversation earlier this week, having lost confidence in your leadership, I have concluded that it would be dishonourable and unprincipled to [remain in post]."

He went on:

"It is now clear that you will not lead the Labour Party into the next general election and that Labour MPs and Labour unions want the debate about what comes next to be a battle of ideas, not of personalities or petty factionalism.

Setting out the reasons for his resignation, he pointed to last week's "unprecedented" local elections results, in which the government's "unpopularity" was "a major and common factor" across Britain, the threat of Reform UK as one of the key reasons for his departure from government, and policy "mistakes".

"Where we need vision, we have a vacuum. Where we need direction, we have drift. This was underscored by your speech on Monday," he wrote.

Streeting is widely thought to be planning to challenge Starmer for the Labour leadership, but he does not announce the start of a formal bid in his letter.

For now there is little to no reaction in GBP or gilts (as several market observers believe any new leadership will deliver more orthodox and less "free shit" fiscal policies) but Polymarket shows the odds of Starmer being gone by the end of May are soaring...

Allies of Mr Streeting, who handed in his resignation as the Health Secretary on Thursday, have made little secret that he is ready to become prime minister and has a comprehensive plan to change the country.

Here is The Telegraph laying out what a Streeting premiership look like?

The economy

Mr Streeting said last year that he was “really uncomfortable with the level of taxation in this country”, suggesting he would resist further increases. Speaking in December, he admitted the Government was “asking a lot” of individuals and businesses with historically high taxes. But he also warned Britain had “a level of indebtedness that we need to take very seriously”, indicating that tax cuts would also be unlikely. He has previously defended Labour’s decision to increase employers’ National Insurance, saying the raise had paid for more NHS appointments. Mr Streeting has previously proposed several radical changes to the tax system. In a 2020 interview, he suggested equalising capital gains tax with income tax, replacing inheritance tax with a “lifetime gifts tax” and increasing corporation tax. He also said all new tax and spending plans should be put through a “progressive impact test” to ensure they helped people on low and middle incomes. But unlike his Left-wing rivals, he has also long advocated that Labour should stick to strict fiscal rules, balancing day-to-day spending with tax revenues.

Defense

Mr Streeting caused a stir in Westminster last month when he suggested that savings should be found from the welfare budget to fund defence. The Health Secretary acknowledged that Britain needed to put more money into the military and that the cash “has to come from somewhere”. While he ruled out taking the money from the NHS budget, he signalled an openness to find it from other areas of spending, such as benefits. Other than on that issue, Mr Streeting has largely backed Sir Keir’s plans to boost defence spending to 3 per cent of GDP by the mid-2030s. Last month, he defended the Government’s handling of the military, insisting that Britain was still “the cornerstone of European defence and security”. Defending the repeated delays to the Government’s defence investment plan, he said Downing Street was taking the time to “get it right”.

Brexit

Mr Streeting is one of the most high-profile Remainers in the Cabinet and was a passionate campaigner for Britain to remain in the EU. Last year, he strongly suggested Labour should consider taking the UK back into a customs union with Europe, saying it would boost growth. But he did insist that the manifesto pledge not to return to freedom of movement with the Continent must stay, ruling out the single market. “The best way for us to get more growth into our economy is a deeper trading relationship with the EU,” he told The Observer in December. “The challenge is any economic partnership we have can’t lead to a return to freedom of movement.” Mr Streeting has long been an advocate of closer EU ties. In 2018, while a backbencher, he rebelled against then leader Jeremy Corbyn, calling for him to commit Labour to keeping Britain in the single market and a customs union.

Immigration

Mr Streeting is naturally a liberal on immigration and has repeatedly signalled his discomfort at the Government’s clampdown on visas and asylum. He criticised Sir Keir’s “island of strangers” speech and has previously said Britain relies on migrants to care for an ageing population. Last November, he admitted he was not comfortable with plans laid out by the Home Secretary to deport families who arrived in the UK illegally. In a 2018 speech, Mr Streeting argued that “we rely on attracting people from overseas, particularly with our ageing population and shrinking working-age population”. But as far back as then, the Health Secretary was stressing the point that Britain needed to increase education and training for its domestic workforce. It is a principle he has taken into government, criticising the health service’s reliance on foreign doctors and admitting voters had “lost confidence in the immigration system”.

The NHS

One of the most notable things Mr Streeting has done in his two years in post is abolishing NHS England, the world’s largest quango. The decision came as a surprise to Westminster and demonstrated that the Health Secretary was unafraid to make significant structural changes to government. It will also put him and his ministers back in direct control of the NHS, hinting at a hands-on approach and a willingness to take on personal responsibility. Waiting lists have fallen on Mr Streeting’s watch and pledges to further improve the health service would be a core part of his premiership. He has also shown himself willing to go to war with the medical unions, warning that their pay demands for junior doctors would “break the country”. But although he has repeatedly spoken of the need to reform the NHS, any change to its funding model would be off the table under Mr Streeting. The Health Secretary has attacked Nigel Farage, the Reform UK leader, for suggesting the UK should consider moving to a French-style public insurance model.

Streeting is only one of the party figures likely to throw their hats into the ring in the event of a formal leadership contest. Former deputy premier Angela Rayner said Thursday morning that she had been cleared of wrongdoing in a probe into her tax affairs, while there is a large faction on the party’s left working to secure a parliamentary seat for Manchester Mayor Andy Burnham, who can’t run without one.

For Starmer to face a formal leadership challenge, a potential successor would have to be nominated by 20% of Labour Members of Parliament. The party currently has 403 MPs, putting that threshold at 81. The ensuing contest would be decided by preferential votes by Labour Party members and affiliates, with precise voting eligibility set by Labour’s governing body.

Tyler Durden

Thu, 05/14/2026 - 13:45

The yellow area shows the last part of the Donetsk oblast that Russia has yet to seize control of. The Luhansk oblast is to the northeast, while the next two oblasts moving southwest are Zaporizhzhia and Kherson, with Crimea at the southernmost end (via

The yellow area shows the last part of the Donetsk oblast that Russia has yet to seize control of. The Luhansk oblast is to the northeast, while the next two oblasts moving southwest are Zaporizhzhia and Kherson, with Crimea at the southernmost end (via

via Express Tribune

via Express Tribune

Recent comments