Futures Tumble As Latest Chinese "DeepSeek Moment" Sparks Chip Meltdown

A surprise breakthrough from Chinese AI startup Moonshot (which is now at the top of the Frontend code benchmark on Arena) rumbled through global markets, sending chip stocks reeling, as queasiness returned about the industry’s unprecedented spending spree (something we have been warning about for the past year). Moonshot claims its new Kimi K3 model rivals top offerings from OpenAI and Anthropic in a release reminiscent of last year’s “DeepSeek moment.” It came as President Xi Jinping appeared at China’s premier AI summit, underscoring how rapidly the nation’s AI developers are closing the gap with US rivals (discussed here a month ago). Meanwhile, delays by Alphabet to the launch of the latest Gemini model has also dented tech sentiment. As a result as of 8:00am ET, S&P futures are 0.8% lower with Nasdaq futs tumbling 1.7%; pre-market, Mag 7 are all lower with NVDA (-2.8%), AMZN (-2.1%), and META (-1.8%) among the most notable decliners. AI and Semis concerns continued to dominate the market narrative overnight ahead of Mag 7 earnings next week. What is different from the past few weeks of momentum selloff is that both Mag 7 and Semis were being sold overnight and yesterday, pointing to "concerns over hyperscalers’ AI CapEx and the sustainability of the AI rally" according to JPM. Moonshot’s AI model release also led to further concerns in China AI model competition and questions on AI CapEx (“DeepSeek 2.0” concerns): overnight, Asia AI baskets and China AI baskets (which include Moonshot’s competitors Z.AI and MiniMax) fell 5-8%. Bond yields are lower across the curve: 2y and 10y are 2.1bp and 2.8bp lower, respectively. Oil added another 1.8%; WTI now at $80.47 this morning after Kuwait said power and water plants were attacked by Iran as hostilities in the Gulf escalate with every passing day. Both base and precious metals are higher this morning. US economic data calendar includes June import/export price index, and June housing starts (8:30am), June industrial production (9:15am) and July preliminary University of Michigan sentiment (10am).

In premarket trading, Mag 7 stocks are all lower (Nvidia -2.4%, Amazon -1.4%, Microsoft -1.9%, Tesla -1.7%, Alphabet -1.5%, Meta Platforms -1.5%, Apple -0.1%). Chipmakers and other AI-related firms are set to extend their selloff amid a broad unwind of the tech trade. Marvell Technology (MRVL) -2%, Qualcomm -2%.

- Autoliv (ALV) falls 5% after the airbag and seatbelt maker reported second-quarter adjusted earnings per share that narrowly missed consensus estimates.

- Intuitive Surgical (ISRG) tumbles 10% after the robotic-surgery company maintained its forecast for Worldwide da Vinci robotic procedure growth for the full year, even as its second-quarter results came in ahead of the average analyst estimates.

- Netflix (NFLX) falls 10% after the streaming giant forecast a second consecutive quarter of slowing sales growth. Analysts note that the tepid current quarter forecast is overshadowing an otherwise in-line quarter.

- Staar Surgical (STAA) drops 8% after the maker of implantable lenses posted preliminary second quarter results where sales in Europe, theMiddle East and Africa declined by a low single-digit percentage, reflecting ongoing turmoil in the Middle East.

In other corporate news SpaceX aborted Thursday’s Starship rocket mission when some of its engines didn’t fire up, it's stock tumbled another 3% to $125, the lowest since its IPO less than two months ago. US regulators traced a parasite outbreak that’s sickened thousands in Michigan and nearby states to shredded iceberg lettuce served at Taco Bell restaurants, identifying a single supplier as the apparent source.

Tech is once again dragging futures lower in early trading as questions over momentum, semiconductor capex and hyperscaler debt persist, masking a powerful rotation beneath the surface. Traders rushed to exit positions in stocks that had fueled this year’s rally, sending the Nasdaq tumbling. The S&P 500 Equal Weight Index posted an all-time high in Thursday’s cash session and the VIX remains below the key psychological level of 20, but the S&P 500 is down on the week and set to deepen those losses on Friday.

Stock investors are taking profits on crowded positions in chip-related stocks, with a key gauge of industry giants still up 68% this year. For Francisco Simon, European head of strategy at Santander Asset Management, the selloff still looks moderate in comparison to the preceding rally. “We would distinguish between fundamentals and positioning,” he said. “From a fundamental perspective, the picture remains solid: earnings momentum has been exceptional this year, and results are still coming in strongly.”

Beata Manthey, head of European and global equity strategy at Citigroup, says sharp stock rotations are necessary for the equity rally to broaden beyond the tech sector. “The market has started to hope for some long-awaited broadening,” Manthey told Bloomberg Television. “For that to happen, you need to have some rotations, and rotations tend to happen in quite a violent way sometimes — and this is what we’re seeing right now.”

Also in tech, the marquee listing of CXMT ignited a rush among retail investors as China’s homegrown memory giant opened books for an IPO to raise $9.8 billion, the second-largest in the nation’s history. The retail portion of the IPO was 212 times oversubscribed. President Xi hailed China’s progress in developing low-cost AI in his debut at the World AI Conference in Shanghai on Friday. The rise of China’s AI models shaping the technology’s global rules is stirring security alarms in Washington and Beijing alike.Elsewhere, Japanese memory chipmaker Kioxia’s market capitalization has now halved in just a month since becoming the nation’s most valuable company.

“When there’s panic, no one wants to be the last one in a selloff, so the selling pressure increases,” said Guillermo Hernández Sampere, head of trading at MPPM. “With the start of reporting, the suspicion of overvaluation has been confirmed and will continue for a bit.”

In short, chipmakers and other AI-related firms are set to extend their selloff amid a broad unwind of the tech trade. Meanwhile Netflix, already more than 40% lower in the past year, is also weighing on tech sentiment. The streaming giant fell 10% in premarket trade Friday after forecasting a second consecutive quarter of slowing sales growth, fanning fears for its future.

Cash would offer good protection in the near term, Simon at Santander Asset Management said. Bonds are a less attractive option as higher oil prices could undermine the defensive characteristics of sovereign debt. “The key reassurance would probably come from the earnings season,” he said. “If companies continue to deliver solid results, and valuations become more attractive after the correction, that could help bring longer-term buyers back.”

Another day of attacks and counterstrikes in the Middle East also weighed on sentiment. Concerns are growing that the US and Iran will intensify hostilities, making oil tanker operators wary of transiting the Strait of Hormuz.

In geopolitics, Trump accused China of interfering with US elections in 2020, claiming the Chinese government stole voter files, including names, addresses and other sensitive data. The US administration said it would shorten the duration of visas for foreign journalists - raising concern about a new round of tit-for-tat restrictions with China.

Meanwhile, the Fed’s Vice Chair Philip Jefferson suggested the central bank should consider raising interest rates if inflation doesn’t cool soon.

Selling by US corporate insiders raised another red flag about investor caution. Executives sold $77.6 billion of stock during the first half, according to EPFR Global Market Intelligence, the second-highest amount in more than 20 years a classic red flag to some investors because it suggests people with the most corporate knowledge are wary about markets.

European equities edged lower on Friday. with technology and mining shares leading declines, while utilities and telecommunications stocks outperform. Tech subindex of the Stoxx 600 down to the lowest since May. Here are the biggest movers on Friday:

- Tomra gains as much as 16% after the recycling equipment firm’s 2Q report beat expectations and the firm announced a contract to supply 1,200 recycling machines with a large UK retailer

- EQT rises as much as 13% after the investment firm’s first-half earnings beat estimates, providing some relief to a stock that had fallen more than 20% year-to-date through Thursday

- Getinge shares jump as much as 10% after the Swedish health-care equipment firm reported second-quarter sales and earnings which JPMorgan says were better than expected

- Assa Abloy gains as much as 6.2%, the most in a year, after the Swedish lock and entrance systems maker reported its latest earnings

- European semiconductor stocks decline across the board on Friday. AI trades that were popular in the first half lose ground amid concerns over the sustainability of AI spending

- Lagercrantz shares plunge as much as 16%, its biggest drop since 2022. The industrial conglomerate posted quarterly margins and earnings that missed expectations, according to DNB Carnegie

- AAK sinks as much as 12% after the Swedish maker of vegetable oils and fats saw a softer second quarter, impacted by lower volumes, price pressure in Food Ingredients and production-related challenges at its Karlshamn site

- DKSH shares fall as much as 8.3%, the most since September, after the Swiss conglomerate reported operating profit for the first half-year that missed the average analyst estimate

- Burberry shares fall as much as 7.3% after the UK luxury brand posted first-quarter results that were weaker than expected in Europe and Asia

- Valterra Platinum slipped as much as 2.4% after the miner reported 2Q earnings and 1H guidance. Analysts note that 2Q own mined volumes missed, while PGM refined production was in line

Asian stocks slipped the most in three weeks despite robust earnings from Taiwan Semiconductor Manufacturing Co., highlighting how elevated expectations have become for AI-related companies. The MSCI Asia Pacific Index dropped 2.8% and is headed for a second straight weekly decline. TSMC fell more than 7%, triggering a correction in Taiwan’s Taiex. The Nikkei 225 slid 4% as Japanese chip-related stocks such as Kioxia Holdings Corp. and Tokyo Electron Ltd. came under pressure. Hong Kong and mainland China also declined, while South Korea’s markets were mercifully closed for a holiday, even though the KORU 3x levered korea ETF plunged. TSMC reported a faster-than-anticipated 77% jump in quarterly net income and raised both its revenue and spending projections. The main chipmaker for Nvidia Corp. now expects sales to grow more than 40% this year and plans to spend as much as $64 billion in 2026, reflecting confidence that AI-driven demand for chips and data centers will remain strong. Some markets with lower exposure to AI such as Indonesia, the Philippines and India rose. Malaysia’s benchmark stock index gained 0.5% as the country reported a surprise surge in economic growth in the second quarter. Investors will focus on earnings for companies including CATL and Shin-Etsu Chemical in the week ahead. Other key events include Indonesia’s monetary policy. The Jakarta stock index has climbed for seven straight sessions, the longest streak in about a year.

In FX, the Bloomberg Dollar Spot Index is up 0.1%, with the Swiss franc outperforming among major currencies while the Aussie dollar and sterling lag. Traders continued to dial down expectations for Federal Reserve interest-rate hikes this year.

In rates, treasuries hold modest gains despite the rise in oil prices, sending 10-year yields four basis points lower to 4.52% with US stock index futures under pressure from chipmaker shares after surprise breakthrough from Chinese AI startup Moonshot and Alphabet’s delayed launch of latest Gemini model. Limiting gains, oil futures are up more than 2% after Kuwait said power and water plants were attacked by Iran. Treasury yields are 2bp-4bp lower led by 5- to 10-year sectors, flattening 2s10s curve by about 1bp; 10-year near 4.51% outperforms bunds and gilts in the sector by 2bp and 1bp respectively.

In commodities, WTI crude oil futures are up 2.6% near session highs, heading for biggest weekly gain since April as the escalating conflict between the US and Iran disrupts Middle East supply. IG dollar issuance slate empty so far, though Bank of America, Citigroup and Wells Fargo are expected to tap the market as soon as Friday; weekly volume is near $47 billion. Gold moving higher but short of $4,000/oz.

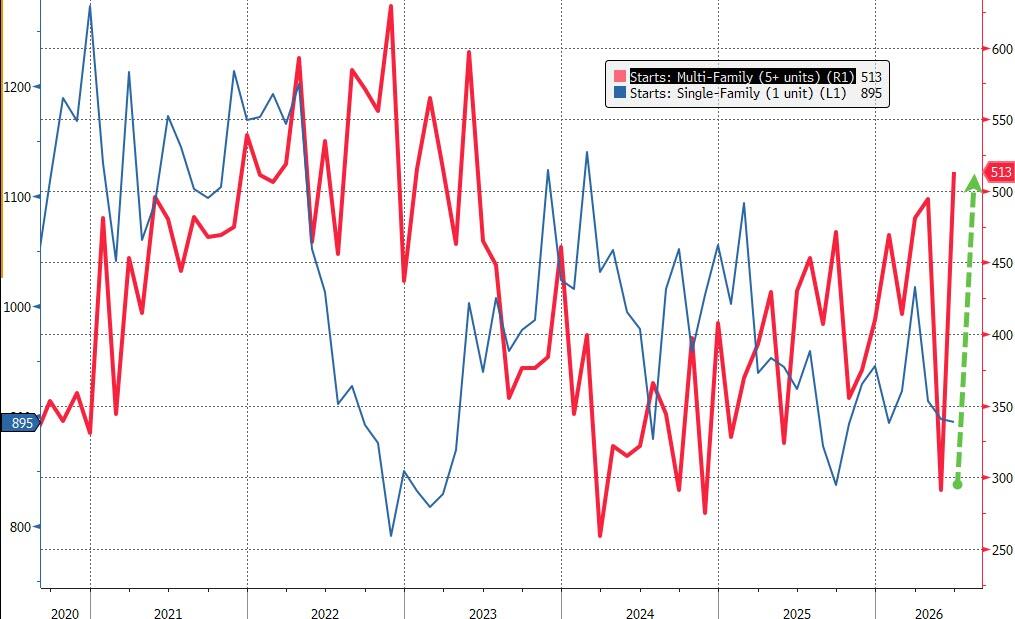

US economic data calendar includes June import/export price index, and June housing starts (8:30am), June industrial production (9:15am) and July preliminary University of Michigan sentiment (10am). Fed calendar is blank; external communications blackout period commences Saturday ahead of the July 29 policy decision

Market Snapshot

Top Overnight News

- US President Trump announced the immediate declassification of intelligence on elections during his primetime address and noted that China engaged in election-related activities in 2020 and did not want him to win the election, while he claimed that China attempted to manufacture ballots for Biden and worked to influence businesses against him. China's Foreign Ministry denied these accusations.

- China’s Moonshot AI has launched an artificial-intelligence model, Kimi K3, it says outperforms some cutting-edge U.S. systems, the latest sign that Chinese labs can rival American counterparts like OpenAI and Anthropic in critical technology frontiers. WSJ

- The U.S. struck multiple bridges in Iran on Thursday to cut off supply routes to a port city and naval base in the Strait of Hormuz that Iran uses to attack ships and project power, according to a senior U.S. official. Several attacks on bridges were reported in and around the port city of Bandar Abbas overnight Thursday, and highways connecting Bandar Abbas to nearby provinces were declared closed, according to Iran’s state broadcaster IRIB. WSJ

- Two US-sanctioned tankers carrying cooking fuel are U-turning and navigating in the Gulf of Oman and Arabian Sea as the US steps up enforcement of its blockade on Iranian shipping. A third sanctioned LPG vessel is indicating China as its destination. BBG

- Japanese PM Sanae Takaichi called for households and the GPIF to increase investment in domestic financial assets, fueling expectations of possible allocation changes at the fund. Finance Minister Satsuki Katayama reiterated her willingness to take “decisive action” in currency markets. BBG

- Xi Jinping called for inclusive cooperation on AI development and urged the world to avoid technological rivalries at China’s top tech summit. BBG

- The ECB will probably pause to assess inflation next week before delivering a final rate hike in September. BBG

- New York City air quality remains at “unhealthy” levels today as the EPA warned people to spend more time indoors, with wildfire smoke blanketing much of the East Coast. Several communities across northern Ontario have initiated evacuation to avoid the blaze. BBG

- BP and ConocoPhillips are set to announce billions of dollars of new investments in Iraq on Friday as Washington seeks to bolster the country’s energy sector and reduce the region’s reliance on routes vulnerable to Iranian disruption, according to people familiar with the plans. CNBC

- A top executive at Amazon’s cloud division plans to join Meta Platforms in the coming weeks, a sign of the social-media giant’s growing ambitions in developing data centers and computing resources. Dave Brown, one of the most senior executives at Amazon Web Services, will bring his nearly two decades of experience to Meta, where he will report to the company’s head of infrastructure and focus on the firm’s data center build-out. WSJ

- US President Trump called on Congress to pass the Save America Act in light of recent revelations.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured as the tech selling rolled over from Wall St and with sentiment weighed on by US-Iran escalation, in which the US conducted a sixth consecutive night of strikes on Iran and targeted infrastructure, including an airport, railway station and several bridges. ASX 200 was dragged lower by weakness in mining, materials, resources and tech, while telecoms, energy and defensives were at the other end of the spectrum, helping cushion the downside. Nikkei 225 underperformed and took the brunt of the semiconductor sell-off in the absence of its South Korean counterpart due to Constitution Day, while Kioxia was heavily pressured and has shed 50% of its market cap from last month's peak. Hang Seng and Shanghai Comp conformed to the downbeat mood amid the tech-related woes, and with sentiment also not helped by US President Trump's primetime address, in which he accused China of meddling in the 2024 US Election and called for Congress to pass the SAVE America Act.

Top Asian News

- Japanese PM Takaichi said the government will pursue steps that encourage investment in Japanese financial assets, including by households and pension funds like the GPIF.

- Chinese President Xi said that the world has entered an unprecedented period of AI innovation, adding they should seize rare historic opportunities to encourage open source AI.

- China FX regulator said foreign investments into China saw net inflows in H1 and outbound investments continue to grow steadily.

European bourses (STOXX 600 -0.7%) are broadly lower, following on from the weakness in Asia (Nikkei -4%, Hang Seng -2.1%), with clear underperformance seen in the AEX (-1.0%) and FTSE MIB (-0.8%). Tech (ASML -4.2%, STMicroelectronics -6.9%) is the clear underperformer following the sharp selloff overnight in APAC names, as worries of stretched valuations persist. Despite the selloff, this week has been broadly positive in the tech space, with both TSMC and ASML reporting strong Q2 figures that beat estimates. Today's weakness just shows that, despite positive news, concerns over the AI capex and its current momentum persist. In terms of the broader sector space, the bias is mixed. Utilities (+1.5%) top the sector pile, followed by Food, Beverages & Tobacco (+0.9%) and Telecoms (+1.1%). Outside of Tech (-2.9%), Basic Resources (-2.1%) and Banks (-1.2%) are the sector laggards. US equity futures are lower across the board, with underperformance in the NQ (-1.9%), given the tech weakness overnight. After-hours, Netflix (-9% pre-market) reported Q2 earnings that came broadly in-line with expectations, but investors were left disappointed by its earnings forecast, with Q3 EPS and Revenue guidance missing estimates. For SpaceX (-3.5% pre-market) , shares fell below its IPO price of USD 135 for the first time on Thursday after the launch of Flight 13 was aborted.

Top European News

- EU Inflation Rate YoY Final (Jun) Y/Y 2.8% vs. Exp. 2.8% (Prev. 3.2%, Low. 2.8%, High. 2.9%).

- EU Inflation Rate MoM Final (Jun) M/M -0.1% vs. Exp. -0.1% (Prev. 0.1%, Low. -0.1%, High. -0.1%).

- EU Core Inflation Rate YoY Final (Jun) Y/Y 2.4% vs. Exp. 2.4% (Prev. 2.6%).

FX

- G10s are mixed against Buck with recent outperformers AUD and GBP underperforming against the Greenback, while Thursday’s CHF underperformance reverses.

- USD is modestly firmer today as it gains some haven demand as stocks (NQ -1.9%) slip as tech weakness remains a theme. A couple of factors are driving today, but to summarise, Nikkei 225 was the target for selling amid the KOSPI closure overnight (due to domestic holiday), which saw stocks take a stronger negative lead from APAC and help the Buck. Aside from this, macro newsflow is light with crude a touch firmer as US and Iran continue to exchange strikes for the sixth day.

- GBP, which is set for a fourth week of gains, pulls back a touch from the 1.35 level as participants await the coronation of incoming PM Burnham. EUR/GBP also saw Sterling outperform for its fourth week, but like Cable, off recent lows as it reclaims 0.85. There remains a level of uncertainty around the incoming PM, with none of his cabinet officials confirmed as of yet, and many policies still unknown. ING expects a return to 0.870 in EUR/GBP by late summer.

- JPY is flat against the Buck despite c. 30pips of downside seen this morning. Japanese PM Takaichi said the govt. would pursue steps that encourage investment in Japanese financial assets, including by households and pension funds like the GPIF. To remind, last week FinMin Katayama said she would pursue steps to promote investment in Japanese assets by GPIF and others. There was some scepticism around this remark as it would be a textbook tactic to encourage domestic investment and passively limit outflows - Katayama is not in a position to direct changes, it would be under the jurisdiction of the Labour Ministry. We await further updates with a timeline around any potential GPIF changes, for now, JPY flat against the Buck near 162.50 despite earlier gains.

Fixed Income

- Fixed income benchmarks are firmer across the board, despite a clear driver; however, debt could be finding some haven flows as equities print deep selloffs globally.

- Gilts (+26 ticks) outperform, with Andy Burnham to begin his Labour premiership on Monday. Focus will be on who Burnham chooses as Chancellor (widely expected to be Home Secretary Mahmood) and what his plans are for the government. Reporting by Bloomberg stated that he has asked the civil service to prepare plans for new North Sea oil and gas drilling and public control of Thames Water. Regarding the Chancellor position, Mahmood is likely to be named Chancellor, but this has already drawn some backlash. Rachel Maskell told the Times that appointing Mahmood would be a mistake and that Miliband “shines well above Shabana.” Despite this, gilts trade at the top end of its 87.15-87.59 range.

- JGBs (+36 ticks) have steadily bid higher in early European trade, after Japanese PM Takaichi said the government will pursue steps that encourage investment in Japanese financial assets, including by households and pension funds. She even specifically named GPIF. Focus on pension fund investments in domestic assets started after FinMin Katayama said she wanted to encourage the GPIF to invest more. Takaichi's more recent comments would likely strengthen the view that the government is keen to have the GPIF consider altering its asset allocations.

- USTs (+8 ticks) trend higher despite a lack of events on the calendar. Fed's Jefferson gave remarks overnight, stating that it would be appropriate to reconsider the stance in the scenario in which inflation does not start cooling.

Commodities

- The US continued to strike Iran for a sixth consecutive night. Following this, Iran claimed power facilities, bridges and civilian infrastructure were struck. And in response, Iran launched its own strikes on Gulf neighbours.

- More pertinently was a severe warning from the Iranian Army Spokesman. He stated that if the US strike the infrastructure of Iran, all infrastructure in the region will be a legitimate target; He added that “either all countries in the region can export oil or no one can”.

- Other news in the region, the UKMTO received 2 reports. More recently, there was a report 65NM south of Al Mukalia, in which unauthorised personnel boarded the vessel. Sources say armed assailants boarded a chemical products tanker Asana in the Gulf of Aden, which is potentially related.

- Crude benchmarks spent the overnight session in the green, amidst the aforementioned developments. Brent Sep’26 (+1.7%) holds towards the top end of a USD 83.71-85.88/bbl range.

- Spot gold (+0.5%) is incrementally firmer this morning, though still remains just shy of the USD 4k/oz mark, after dipping below that mark in the prior session. Recent pressure has been driven by the ongoing inflationary woes surrounding the latest US-Iran escalation. Nonetheless, some analysts remain confident in the structural drivers for the yellow metal, namely, continued central bank purchases. Elsewhere, base metals are broadly in the red this morning – hampered by the risk tone. 3M LME Copper trades within a USD 13,429-13,563/t range.

- BP (BP/LN) and ConocoPhillips (COP) reportedly set to announce billions of dollars of new investments in Iraq on Friday, CNBC reports; sources said the figure may be in the tens of billions.

- Chinese LNG importers are exploring ways to reduce reliance on Qatar, Bloomberg reported.

- China State Planner NDRC to cut retail fuel prices in the current bi-monthly cycle, effective July 18th. To cut gasoline prices by CNY 300/t, and diesel by CNY 290/t.

- TotalEnergies (TTE FP) cut output at Port Arthur refinery as the reformer is undergoing repairs.

Central Banks

- Fed's Jefferson (voter) said the current policy stance should support the job market and allow inflation to resume its decline towards 2% as tariff effects and energy prices pass through. Jefferson said in a scenario where inflation does not start cooling, it could be appropriate to reconsider the stance and ensure they deliver price stability, while he added that current policy is well-positioned to respond based on incoming data, the evolving outlook and balance of risks, and he is firmly committed to returning inflation to the 2% target, consistent with the dual mandate.

- BoJ reportedly sees little need for consecutive rate rises, may reconsider its assessment of economic risks, according to Bloomberg citing sources. It is also likely to raise its growth forecast for this year from its current 0.5%. Officials may revise their downside-risk assessment as AI-related demand supports exports, profits and incomes, while faster cost pass-through keeps underlying inflation risks elevated above the 2% target.

Geopolitics

- US President Trump said they will see the fruits of labour in Iran shortly.

- US CENTCOM said forces conducted a new wave of strikes against Iran for the sixth consecutive night to further degrade Iranian military capabilities. The US launched a missile attack on Iranshahr airport, targeted a railway station in Bandar Abbas and struck five bridges in southern Iran. It was also reported that explosions were heard in Ahvaz, Chabahar and Bushehr, with missiles hitting air and naval bases in Bushehr.

- US CENTCOM announced Marines conducted an inspection aboard M/T Wen Yao in the Gulf of Oman on July 16th, while it was separately reported that only three ships crossed the Strait of Hormuz in the last 24 hours, according to marine traffic data cited by Al Jazeera.

- Iran targeted US radars in Kuwait with a drone strike, and explosions were reported at the US Navy's Fifth Fleet Naval Base in Bahrain, while blasts were heard at a US airbase in Qatar and in Erbil, Iraq.

- IRGC claimed to have launched an attack on a US command centre in Syria's Al-Tanf, while it warned no oil or gas will be exported through the Strait of Hormuz as long as US attacks continue.

- Iran has informed allies, including Hezbollah, that the waiting phase is about to end and ordered them to prepare for military scenarios, according to Kann news citing Lebanese press.

- Kuwait’s Defence Ministry said Iranian 'aggression' on Thursday targeted a number of vital facilities, resulting in material damage.

- Iranian armed forces senior spokesperson said they will never allow the US to interfere in the Strait of Hormuz, while he stated that the route Iran has determined in the Strait of Hormuz is safe, and any route outside it will be unsafe and ships will be damaged. The spokesperson also warned that if the US strike the infrastructure of Iran, all infrastructure in the region will be a legitimate target and stated that "Either all countries in the region can export oil or no one can".

- UKMTO has received a report of an incident 19 nautical miles east of Khasab, Oman. Additionally, the UKMTO received another report of an incident 65NM south of Al Mukalia, Yemen, with the vessel boarded by unauthorised personnel. Following this, maritime sources said armed assailants boarded a chemical products tanker Asana in the Gulf of Aden, off the coast of southern Yemen.

- Lebanese sources said the US-Israeli-Lebanon meeting would likely be postponed to finalise technical arrangements, Sky News Arabia reported.

- Islamic Resistance of Iraq put a USD 10mln bounty on US President Trump.

- Naftogaz said a Russian drone attack suspended operations at a gas production facility in Ukraine’s Kharkiv region.

US Event Calendar

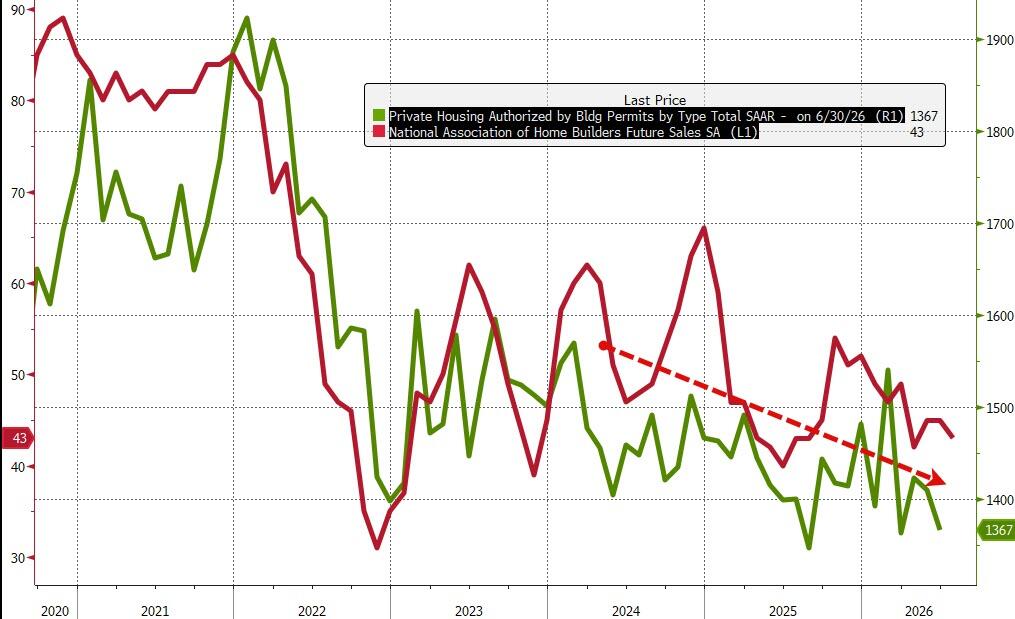

- 8:30 am: Jun Import Price Index MoM, est. -0.65%, prior 1.9%

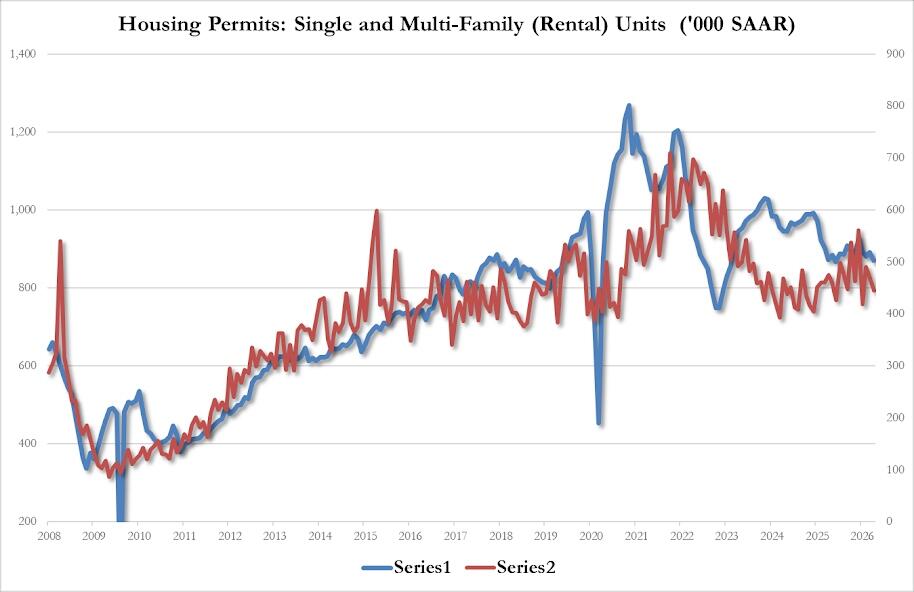

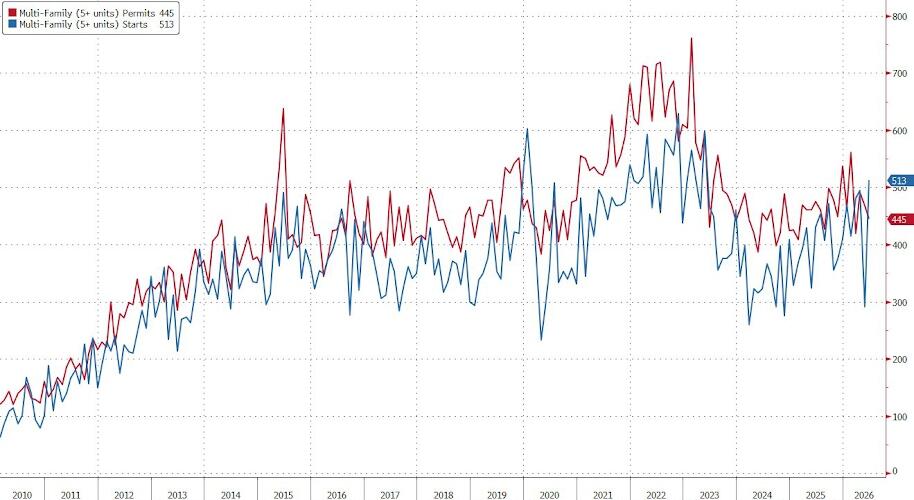

- 8:30 am: Jun Housing Starts, est. 1310k, prior 1177k

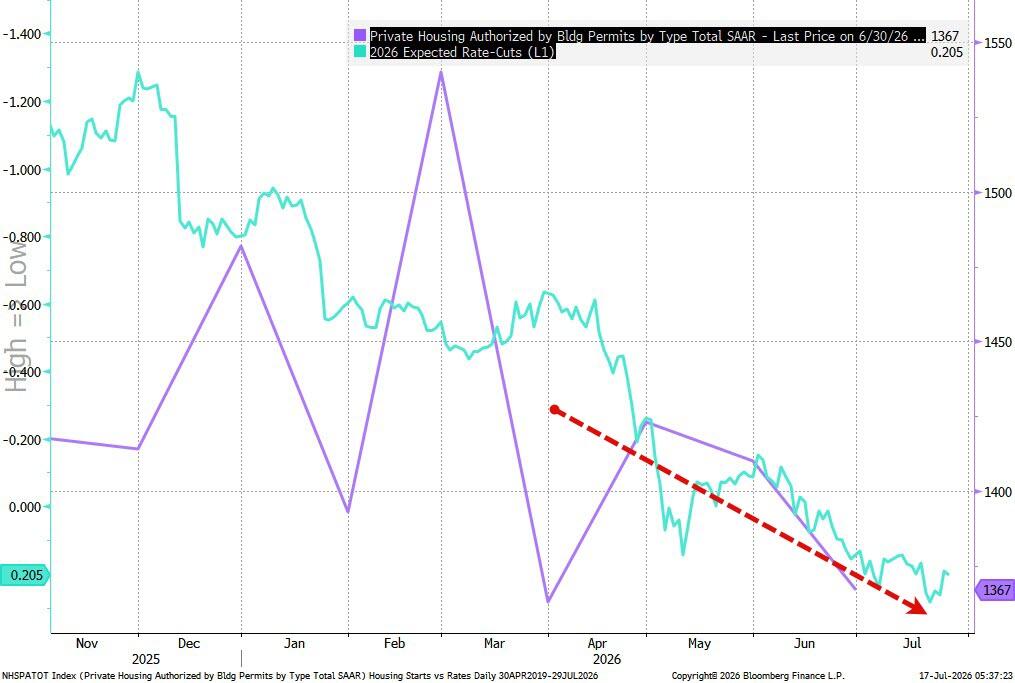

- 8:30 am: Jun P Building Permits, est. 1403k, prior 1410k

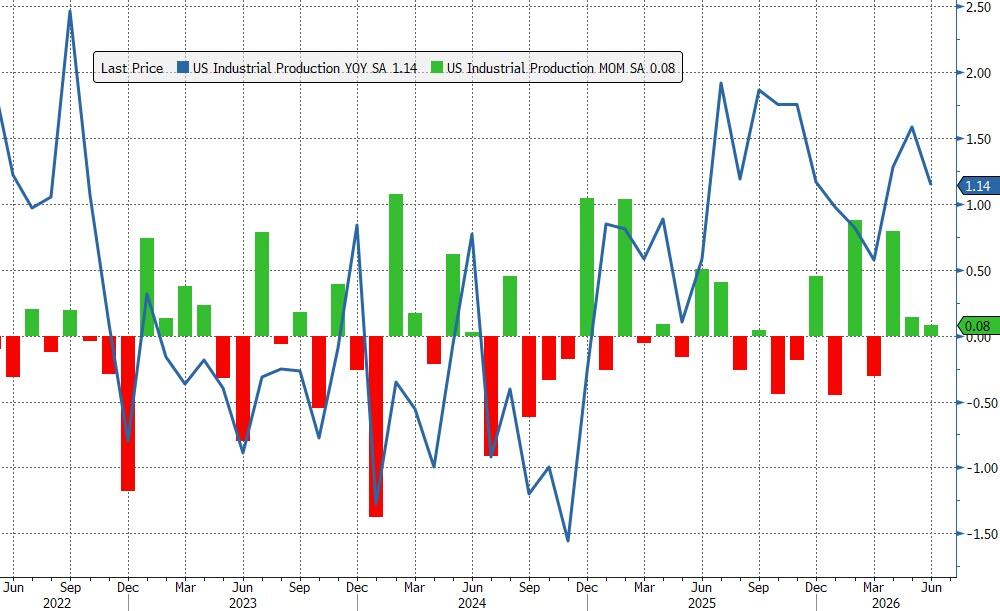

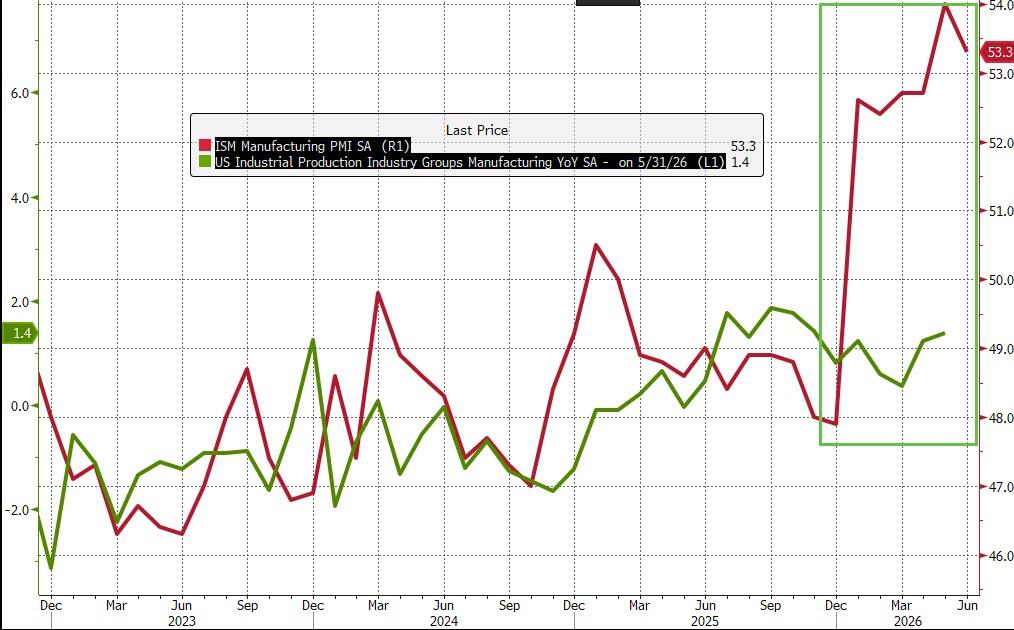

- 9:15 am: Jun Industrial Production MoM, est. 0.2%, prior 0.1%

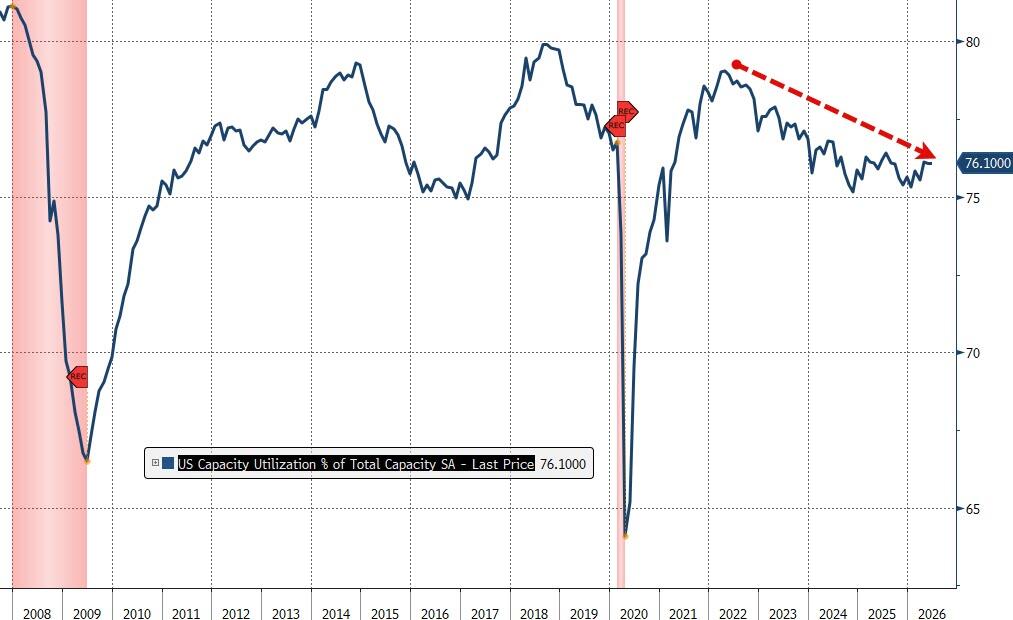

- 9:15 am: Jun Capacity Utilization, est. 76.2%, prior 76.2%

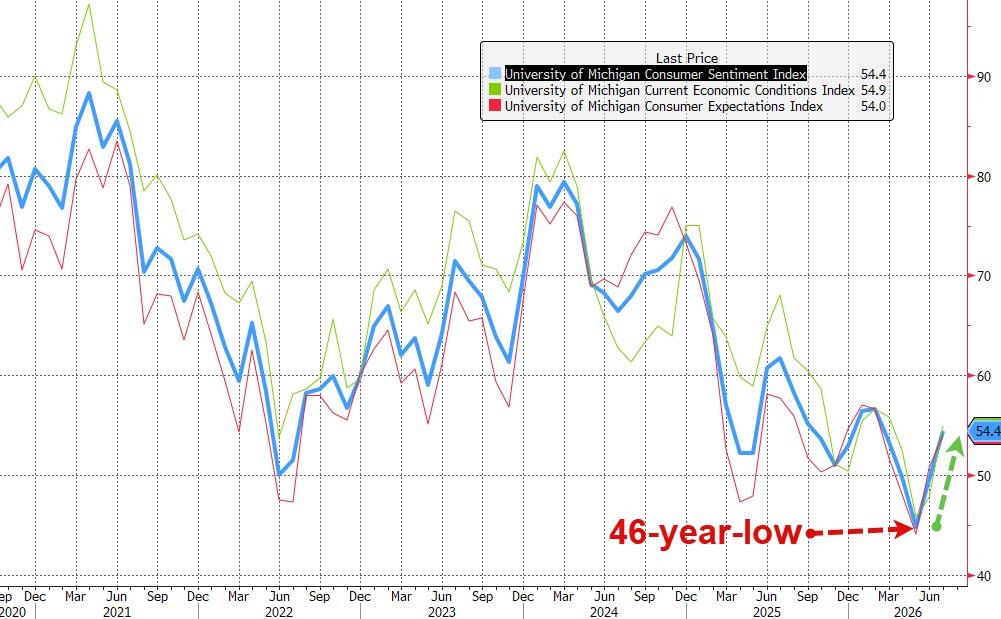

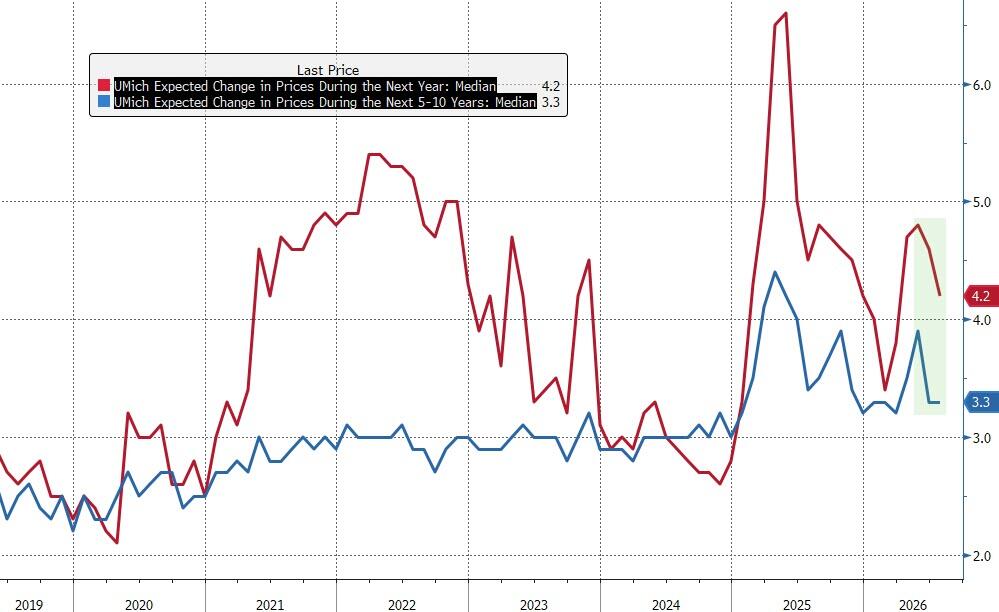

- 10:00 am: Jul P U. of Mich. Sentiment, est. 51, prior 49.5

DB's Jim Reid concludes the overnight wrap

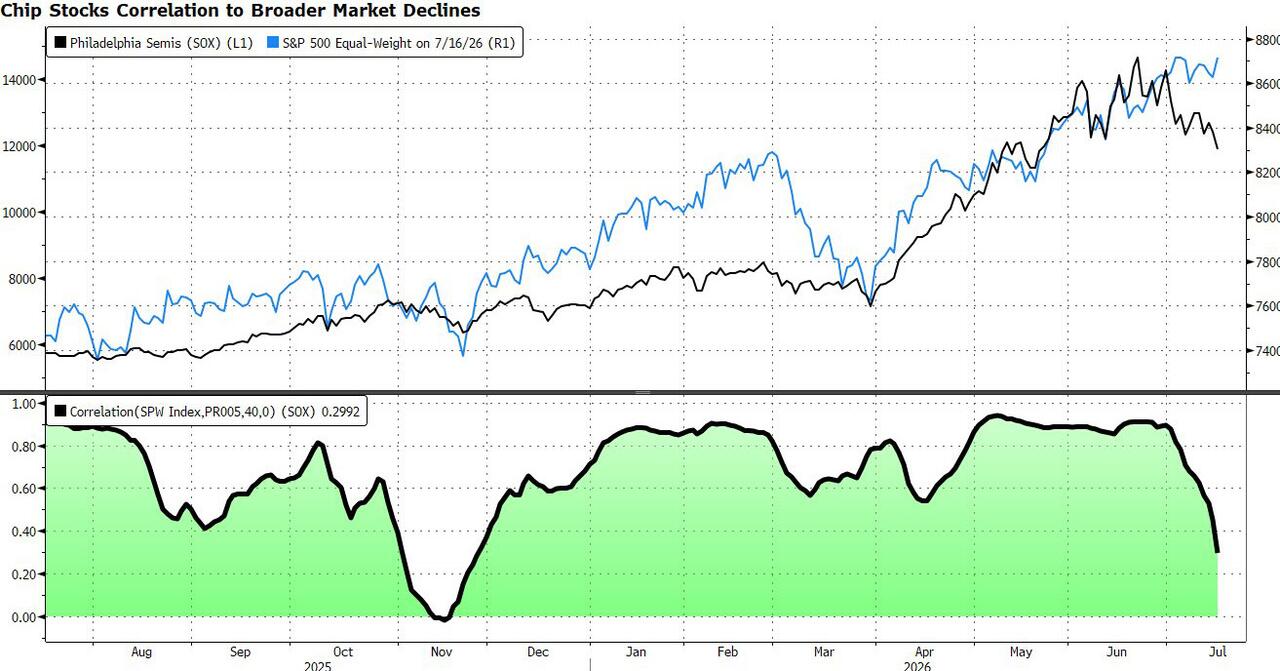

As we go to press this morning, global equities are continuing to slump, as fresh doubts about the AI trade have driven a pronounced selloff in tech stocks. Indeed, the S&P 500 fell -0.51% yesterday, and this morning futures are down another -0.78%. Moreover, there’s no sign of any letup this morning in Asia, with very sharp declines for the Nikkei (-4.81%), the CSI 300 (-2.45%), the Hang Seng (-1.98%) and the Shanghai Comp (-1.64%), whilst the KOSPI is closed for a public holiday. Indeed, that slide indicates the Nikkei is currently likely on course for its worst day since March, and also leaves the index on track for technical correction territory, having now shed over 12% since its peak less than a month ago.

There wasn’t a single catalyst behind the selloff, but we had TSMC’s earnings shortly after we went to press yesterday, and their share price is down -5.26% this morning after they said that capital expenditure would be higher than previously forecast. Meanwhile, Netflix’s earnings disappointed after the close last night, pushing their shares almost -9% lower in after-hours trading. And in the background, fears about rate hikes and more persistent inflation are still there, with Brent crude oil up another +1.06% this morning to $85.12/bbl. That would be its first close above $85/bbl in over a month, and that combination of concerns around tech and inflation has really put a dent in the more buoyant narrative after the soft US CPI report earlier this week.

Before the slump accelerated overnight, US equities had already seen a rough session yesterday thanks to the fresh slide in chip stocks. In fact, the Philly semiconductor index (-4.29%) hit an 8-week low, having now shed -18.91% from its peak less than a month ago. So that now leaves it close to the -20% mark that would mark a technical start of a bear market, which is a big turnaround from Q2, when it posted its best quarterly performance since the index began in the early 1990s. The AI-related tech pullback wasn’t limited to chipmakers either, with a decline for the Mag-7 (-1.27%) led by a slide in Alphabet’s shares (-4.44%) after Bloomberg reported a months-long delay for its new Gemini 3.5 Pro AI model. So that tech decline dragged on the S&P 500 (-0.51%), which fell even as nearly three-quarters of its constituents advanced on the day.

That positive breadth in the US stock market was supported by the latest batch of US data, which suggested that the economy was still in decent shape. Most notably, the weekly initial jobless claims were down to 208k in the week ending July 11 (vs. 217k expected), which was their lowest in two months. So that reassured investors that the labour market was holding up into Q3. Meanwhile, retail sales grew by +0.2% in June as expected, and there was an upward revision of a tenth to the May figures. So collectively, that added to the picture of ongoing data resilience, and we also saw the Atlanta Fed’s GDPNow estimate for Q2 move up as well, now showing an annualised rate of +1.7% (vs. +1.3% before).

In terms of the latest in the Middle East, oil prices oscillated back and forth through the day, as strikes between the US and Iran continued. But this morning they’re currently slightly higher at $85.12/bbl, which would be their first close above $85/bbl in over a month if sustained. In terms of the latest, the US military said overnight that they’ve completed another wave of strikes on Iran, whilst Iran’s Press TV said they targeted US military sites in Kuwait. Otherwise, there was also a Reuters report yesterday that Iran had asked its Houthi allies in Yemen to be ready to close the Red Sea oil route if the US struck Iran’s power network, which raised fears about further supply-chain disruption.

This backdrop saw the probability of a Fed hike by September inch up from 55% to 57%, whilst the number of hikes priced by December was up +1.1bps on the day to 27bps. In turn, Treasury yields edged higher as well, with the 2yr yield (+0.6bps) up to 4.14%, whilst the 10yr yield (+0.5bps) stood at 4.55%. Those moves came as Fed speakers highlighted the potential for rate hikes. For instance, Dallas Fed President Logan (voter) said that “modestly higher interest rates would better balance the outlook and risks” as the path towards a disinflation scenario was for now “more a hope than a likelihood”. Meanwhile, Kansas City Fed President Schmid (non-voter) cautioned that even though the June inflation data was better than expected, inflation “is too hot and has been above target for too long”.

Earlier on, European markets had mixed performance before the slump gathered pace later in the US session. On the bright side, the STOXX 600 (+0.16%) posted a third consecutive advance. But there was an uneven picture across the continent, with gains for the UK’s FTSE 100 (+0.54%) and Spain’s IBEX 35 (+0.15%), alongside losses for the German DAX (-0.34%) and France’s CAC 40 (-0.05%). For sovereign bonds, there were more consistent losses, with 10yr bund yields (+1.3bps) up to 3.13%, whilst 10yr OAT yields (+1.7bps) hit a post-2009 high of 3.93%. European bonds weren’t helped by a continued rise in European natural gas prices, with futures up another +0.79% to a 3-month high of €54.79/MWh.

Here in the UK, data showed GDP grew by a monthly +0.1% in May (vs. unch expected). So gilts underperformed following the data, with the 10yr yield (+2.8bps) rising as investors dialled up the chance of Bank of England rate hikes this year. Meanwhile, Andy Burnham is set to become leader of the governing Labour Party today, having been the only candidate nominated in the contest. He’s then set to become Prime Minister on Monday, after incumbent PM Keir Starmer formally resigns.

Finally, yesterday saw a notable milestone for gold (-2.07%), which fell back below $4,000 to close at its lowest level of 2026 so far at $3,976/oz. That’s a far cry from how it began the year, as January saw gold’s best monthly performance since 1999. But it’s now down over -7% since the year began, and over -25% from its late-January peak.

Looking at the day ahead, US data releases include industrial production, capacity utilization, housing starts and building permits for June, along with the University of Michigan’s preliminary consumer sentiment index for July. In the Euro Area, there’s also the final CPI print for June. Otherwise, central bank speakers include Fed Vice Chair Jefferson and the ECB’s Cipollone.

Tyler Durden

Fri, 07/17/2026 - 08:35

Illustrative wartime image from earlier in the conflict.

Illustrative wartime image from earlier in the conflict. Iran's bridges have come under fresh strikes, via social media/X.

Iran's bridges have come under fresh strikes, via social media/X.

MSNBC; Getty Images

MSNBC; Getty Images

Source:

Source:

{kind=link}

Recent comments