The Architecture Of Abundance: How Bitcoin Reveals The Truth Of Time And Technology

Authored by Sylvain Saurel via 'In Bitcoin We Trust' Substack,

How escaping the fiat illusion and holding the world's hardest money turns the relentless march of technology into unprecedented purchasing power.

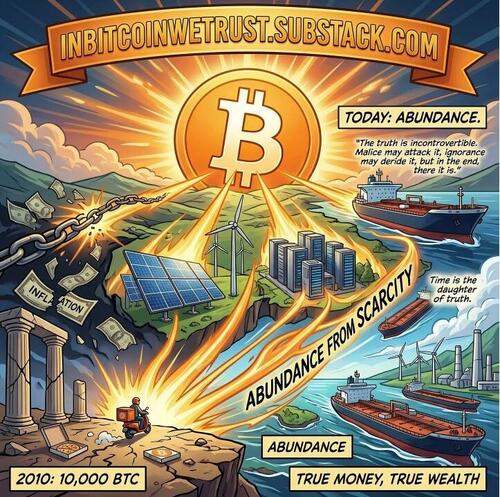

Look closely at the image below:

On the left, two standard Papa John’s pizzas, purchased in 2010 for the seemingly arbitrary sum of 10,000 Bitcoin. On the right, a colossal supertanker cutting through the ocean, a leviathan of modern engineering carrying millions of barrels of crude oil - the literal lifeblood of the global industrial economy. Today, a mere 26 Bitcoin commands this staggering vessel of kinetic energy.

If we run the mathematics of this evolution, the implications are paradigm-shattering. In a span of roughly a decade and a half, the purchasing power of that original 10,000 Bitcoins has metamorphosed from two boxes of delivered fast food into the equivalent of 384 supertankers of oil.

This image is not merely a meme or a historical curiosity; it is the most perfect, succinct encapsulation of what Bitcoin actually is. It is a visual representation of economic truth. Yet, when the world discusses Bitcoin, the conversation is almost universally dominated by the chaotic noise of short-term price action. Pundits obsess over hourly charts, quarterly earnings, regulatory whispers, and the cyclical volatility of a nascent asset finding its sea legs. But zooming out to observe the macroeconomic horizon across sixteen years reveals a profound narrative about time, technology, and the very nature of human energy.

To understand Bitcoin, we must stop looking at what it does in a week and start looking at what it does across an epoch. We must understand why patience is the ultimate economic virtue, why technology demands abundance, and why our current fiat money system is fundamentally designed to steal that abundance from us.

The Tyranny of the Short-Term and the Power of 2042

Human beings are biologically wired for high time preference. Our evolutionary ancestors survived by prioritizing immediate caloric intake and immediate safety over abstract, long-term planning. Today, this biological vestige manifests in our financial behaviors. We want immediate returns. We want the “get rich quick” button. Nobody wants to wait; nobody wants to endure the discomfort of delayed gratification.

When you look at the leap from two pizzas to 384 supertankers, you are looking at the unparalleled reward of a low time preference. You are witnessing the mathematics of holding the hardest money ever engineered by humanity.

Imagine, for a moment, the year 2042. If the purchasing power of this decentralized network can scale from melted cheese and pepperoni to global energy armadas in a mere 16 years, what will a single Bitcoin command in another two decades? What entire industries, infrastructures, or technological marvels will be priced in fractions of a single coin?

Most people cannot fathom this reality because their economic worldview is constrained by the immediate present. The volatility of the short-term timeframe shakes out those who lack conviction. But the fundamental point of Bitcoin is intrinsically linked to time: the longer you hold it, the more you gain from it. This is not a speculative guarantee based on finding a “greater fool” to buy your bags; it is a mathematical inevitability aligned with the deepest truths of technological advancement.

Technology’s Unyielding Mandate: The Deflation of Marginal Cost

To grasp why Bitcoin’s purchasing power aggressively expands over time, we must first understand the fundamental nature of technology.

What is technology, at its core? It is the process of doing more with less. From the invention of the wheel to the printing press, the steam engine, the microchip, and now artificial intelligence, every technological leap shares a singular, unifying characteristic: it drives the marginal cost of production toward zero.

When a farmer transitions from a horse-drawn plow to a mechanized tractor, the caloric energy and time required to harvest a field plummet, while the yield skyrockets. When telecommunications shifted from laying copper cables across oceans to bouncing signals off satellites and routing data through fiber optics, the cost of communicating with someone on the other side of the planet fell from dollars per minute to fractions of a cent. Today, software and AI are eating the world, automating cognitive labor and optimizing supply chains with ruthless efficiency.

The natural consequence of this technological march is abundance. As it becomes cheaper, faster, and easier to produce food, energy, housing, information, and manufactured goods, the prices of these goods should fall dramatically. Deflation—the decrease in the general price level of goods and services—is the natural, logical, and inevitable byproduct of a technologically advancing civilization.

As time elapses, technology advances. As technology advances, it births abundance. And that abundance should rightfully be delivered to humanity in the form of consistently lower prices, requiring us to work less to secure our basic needs, thereby freeing human time and capital for higher-order pursuits.

This is exactly what has happened when we measure the global economy in Bitcoin. The price of everything in the economy is significantly lower in BTC terms than it was a decade ago. Whether you are pricing real estate, the S&P 500, a gallon of milk, or a supertanker of oil, the chart denominating these assets in Bitcoin trends aggressively downward. Bitcoin accurately captures the deflationary dividend of technological progress.

So, if technology is making everything cheaper to produce, why does life feel more expensive than ever?

The Fiat Illusion: Manufacturing the Energy of Scarcity

The reason our grocery bills are soaring, housing has become unaffordable for a younger generation, and the cost of living feels like an ever-accelerating treadmill is not because technology has failed us. It is because our money is broken.

We operate on a fiat currency standard—money decreed by governments, backed by nothing but the threat of force and the promise of future taxation. More importantly, it is a debt-based monetary system. In a fiat system, money is created when debt is issued. In order for this colossal architecture of global debt to survive without collapsing into a deflationary depression, central banks and governments are mathematically forced to constantly expand the money supply. They must inflate.

Inflation is not a bug of the fiat system; it is its foundational feature. The fiat system requires the continuous debasement of currency to service ever-expanding sovereign debts.

This requirement for inflation is a silent, insidious thief. It systematically robs humanity of the lower prices that should rightfully be ours due to technological advancement. Imagine a world where human ingenuity reduces the cost to produce a good by 5%, but the central bank inflates the money supply by 7%. The price on the shelf goes up by 2%. The consumer falsely believes the good has become more expensive to create, completely blind to the fact that their money has simply become vastly weaker. The technological dividend—the 5% savings—was siphoned away by the creators of the currency.

Because fiat money relentlessly loses its purchasing power, it traps humanity in a perpetual rat race. We are forced to sprint at full capacity simply to maintain our current standard of living. Instead of receiving the abundance our technology produces, we are force-fed the energy of scarcity. We are alienated from the fruits of our collective innovation, living in a hyper-financialized world where citizens must become amateur hedge fund managers just to protect their life savings from melting away.

Bitcoin: The Denominator of Truth

Bitcoin stands in stark defiance of this systemic theft. It is an incorruptible ledger, a closed thermodynamic system of money with an absolutely scarce, unforgeable supply cap of 21 million coins. No central bank can print more to bail out failing institutions. No politician can expand their supply to fund a war. No committee can alter its monetary policy to service unpayable debts.

Because its supply is fixed and immune to manipulation, Bitcoin acts as a perfect measuring stick for the global economy. It is simply money that accurately prices the truth of technological advancement.

When you hold fiat currency, you are holding a leaky bucket. When you hold Bitcoin, you are holding an asset that acts as a sponge, eagerly absorbing the deflationary abundance generated by human innovation. As technological advances lower the cost of producing goods and services, and the supply of Bitcoin remains immutably fixed, the purchasing power of your Bitcoin inevitably rises.

As Bitcoin holders, we cease to be the victims of hidden inflation taxes. Instead, we become the direct beneficiaries of technological abundance. We capture that abundance in the form of exponentially greater purchasing power. The transformation of a 10,000 BTC stack from two pizzas to a fleet of supertankers is not a glitch; it is the correct mathematical repricing of the world against a true, unmanipulated denominator.

The Long-Term Horizon: Where Truth Resides

Both of these realities—the magnificent deflationary power of technology and the absolute scarcity of Bitcoin—take time to fully manifest.

In the short term, markets are emotional. They are driven by leverage, news cycles, panic, greed, regulatory saber-rattling, and the sheer noise of human behavioral psychology. Over a timeframe of weeks or months, Bitcoin’s price in fiat terms can fluctuate wildly, leading critics to dismiss it as a volatile speculative toy.

But true economic reality cannot be judged in the span of a fiscal quarter. The truth of money, value, and human progress is only revealed over longer time horizons. Time acts as a filter, stripping away the irrational noise of the day-to-day market and leaving only the undeniable, structural signal. Over a 16-year timeframe, the volatility smooths out, and the undeniable truth emerges: fiat money trends toward zero, while structurally sound money trends toward infinity in purchasing power.

We rely on money to communicate value across space and time. When our money is manipulated, the communication is corrupted. It lies to us about what is scarce, what is valuable, and what our time is worth. Bitcoin is money that reflects reality. It provides perfect information. We cannot ask for anything more from our money than to tell us the truth.

And the truth, eventually, is unstoppable.

As the Buddha profoundly observed:

“Three things cannot be long hidden: the sun, the moon, and the truth.”

The fiat system relies on obscurity, complexity, and a lack of public understanding to maintain its illusion. Bitcoin relies on open-source code, verifiable math, and total transparency. Every ten minutes, a new block is mined, and the network shouts its truth to the world.

It takes time for society to recognize this shift. It takes time for the legacy systems to crack under the weight of their own debt and for the populace to seek a lifeboat. But time is the ultimate ally of the honest ledger. As Leonardo da Vinci wisely noted:

“Time is the daughter of truth.”

The longer Bitcoin survives, the longer it processes blocks without fail, the deeper its roots grow into the global financial infrastructure. Every passing year is a testament to its resilience and its necessity.

In the end, the transition from a debt-based system of manufactured scarcity to a mathematically sound system of technological abundance is not just an economic imperative; it is a moral one. The legacy financial world may fight it, central bankers may scoff at it, and the impatience of the masses may momentarily dismiss it. But the historical trajectory is set.

To borrow the words of Winston Churchill:

“The truth is incontrovertible. Malice may attack it, ignorance may deride it, but in the end, there it is.”

There it is: 10,000 Bitcoin for two pizzas in 2010. 26 Bitcoin for a supertanker today. A world of infinite technological abundance is waiting for us in 2042. The only question that remains is whether you have the patience, the conviction, and the low time preference to step out of the illusion of scarcity and hold the truth.

Tyler Durden

Sat, 04/18/2026 - 10:30

via MarineTraffic

via MarineTraffic

Recent comments