The headlines proclaim the DOW is up 400 points! Yippie, hurrah! But why?

In the middle of the night, the Federal Reserve moved to make it cheaper to swap Euros for dollars, in a coordinated move with Switzerland, Canada, England, the European Central Bank and Japan.

From the Federal Reserve press release:

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing coordinated actions to enhance their capacity to provide liquidity support to the global financial system.

This is supposed to stem a global liquidity crunch. In other words, to prop up the Euro's value.

These central banks have agreed to lower the pricing on the existing temporary U.S. dollar liquidity swap arrangements by 50 basis points so that the new rate will be the U.S. dollar overnight index swap (OIS) rate plus 50 basis points. This pricing will be applied to all operations conducted from December 5, 2011. The authorization of these swap arrangements has been extended to February 1, 2013. In addition, the Bank of England, the Bank of Japan, the European Central Bank, and the Swiss National Bank will continue to offer three-month tenders until further notice.

More interesting the Central banks are offering swaps in multi-currency denominations:

As a contingency measure, these central banks have also agreed to establish temporary bilateral liquidity swap arrangements so that liquidity can be provided in each jurisdiction in any of their currencies should market conditions so warrant. At present, there is no need to offer liquidity in non-domestic currencies other than the U.S. dollar, but the central banks judge it prudent to make the necessary arrangements so that liquidity support operations could be put into place quickly should the need arise. These swap lines are authorized through February 1, 2013.

Some of these have been in place since 2008:

The Federal Open Market Committee has authorized an extension of the existing temporary U.S. dollar liquidity swap arrangements with the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, and the Swiss National Bank through February 1, 2013. The rate on these swap arrangements has been reduced from the U.S. dollar OIS rate plus 100 basis points to the OIS rate plus 50 basis points. In addition, as a contingency measure, the Federal Open Market Committee has agreed to establish similar temporary swap arrangements with these five central banks to provide liquidity in any of their currencies if necessary.

China additionally lowered their bank reserve requirements, from 21.5% to 21%.

China cut the amount of cash that the nation’s banks must set aside as reserves for the first time since 2008.

So why is Wall Street roaring? We don't know. The central banks move does not solve Europe's problems. Just yesterday we see multinational corporations plan for possible end of euro as reported the Financial Times:

International companies are preparing contingency plans for a possible break-up of the eurozone, according to interviews with dozens of multinational executives.

There goes multinationals' currency exchange rate power plays on plant locations:

With countries coming out of the euro, you’ve got massive devaluation that makes imported brands very, very expensive.”

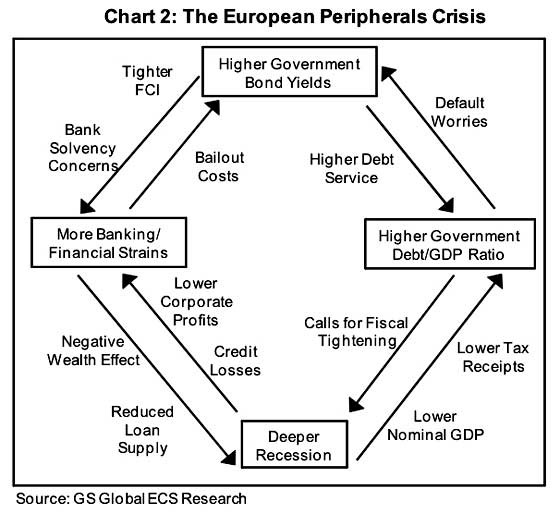

This image, found on business insider (gee, they show something useful, it's usually pretty girls and iPhones), shows the never ending vortex the European sovereign debt crisis has become.

Simon Johnson firmly believes the Euro is D.O.A.

Ultimately, an integrated currency area may remain in Europe, albeit with fewer countries and more fiscal centralization. The Germans will force the weaker countries out of the euro area or, more likely, Germany and some others will leave the euro to form their own currency. The euro zone could be expanded again later, but only after much deeper political, economic and fiscal integration.

Tragedy awaits. European politicians are likely to stall until markets force a chaotic end upon them. Let’s hope they are planning quietly to keep disorder from turning into chaos.

The problems in Europe are still not solved. Some are talking about a fiscal union as saving the day.

Others are mentioning trade imbalances as a significant cause:

What would help the Eurozone most is a MUCH cheaper euro, since the only way out of their fundamental problem (that of Germany running big trade deficits with periphery countries, but no longer wanting to fund the trade deficits that result) is by cheapening the euro greatly, so that Germany runs big trade surpluses with non-Euro countries, and the rest of Europe has more or less balanced trade.

We previously gave additional collections of events which hinted something is a brewing over the Atlantic. This is, in essence, more kicking the can down the road and money printing. In other words, another move for the markets, Wall Street, not main street or even sovereign nations.

On November 22nd, the Federal Reserve announced new bank stress tests, with foreign banks subsidiaries, read exposure to Europe, added into the mix.

Could it be this move is just the start of several? Stay tuned....

Comments

Hiding monetization behind nominal GDP and Eurodollars

"In the middle of the night, the Federal Reserve moved to make it cheaper to swap Euros for dollars, in a coordinated move with Switzerland, Canada, England, the European Central Bank and Japan." -- Robert Oak

I first heard the news last night from a blog at blogspot Jesse's Café Américain: Currency Wars: The Anglo-American Century and Why the Financial Engineers Hate Gold and Silver (29 November 2011, Paris time). Then about noon today (30 November), the WSJ online story made it official, "the market" said 'Huzzah!' and now happy times are here again as the bell at the NYSE has sounded at the end of a great day for traders and brokers.

Jesse identifies the six central banks as "Anglo-American" but I would suggest that a better descriptor would be "tri-lateral," since they include the Bank of Japan, the European Central Bank (ECB) and the Swiss National Bank. (See, Wall Street Journal online story, Central Banks Take Coordinated Action.)

In his blog, Jesse suggests that a key component of a plan or trend to disguise monetization of USA national debt is a tendency to alter GDP toward "Nominal GDP" or "NGDP", NGDP being GDP without adjustment for inflation.

Since what is said to be of most importance is the ratio of debt to GDP, a key to what is happening is that the ratio of debt to GDP becomes less if NGDP is used rather than GDP. This effect can result simply from year-over-year officially understating the rate of inflation -- GDP will appear larger than it really is, and unsustainable trends toward hyperinflation will be hidden. Thus, using NGDP rather than real GDP means a GDP growth target can be achieved simply by inflating the money supply to make up the difference between real growth and officially designated "headline growth."

However, Jesse believes that the Fed isn't relying solely on NGDP chicanery to disguise underlying problems, rather "major monetization is already occurring in the Eurodollar markets, and an ongoing stealth bailout of European debt, in order to save the big money center banks at home and broaden the reach of the Dollar." Looking back and then projecting forward, Jesse believes that "the Fed stopped reporting on Eurodollars some years ago, as a component of M3" in order "to pave the way for the monetary equivalent of a financial neo-con, to addict European governance to the US dollar and pave the way for a stronger position for the dollar as a one world currency."

This begins to sound like what I sometimes call 'goldbuggery', meaning CT built around interpretation of financial history as all about an ineluctable trend toward collapse of all global currencies (except gold) -- and the big take-over of the world by certain financial elites. As a monetarist, I agree to some extent with what I call goldbuggery, except that (again as a monetarist) I believe that the trend toward collapse can be reversed as it has more to do with public ignorance/apathy, political corruption and the central bank system of fractional reserve banking than with the operation of any universal or unavoidable laws of political economics (theories of the Austrian or von Mises School).

Jesse probably takes a view similar to mine. In any case, Jesse's Café Américain is one of the most sane and balanced open blogs in the world of PM-based economic commentary.

Jesse stops short of CT, saying, "Most of what is transpiring now has not been planned." But Jesse retains the basic skepticism and suspicion about a trend (if not necessarily a conspiracy) toward a global fiat currency --

I put Jesse's "too much power in too few hands never fails to end in exploitation" in bold, because that's where I am assured that Jesse's approach is much like my own. I am of the original 'Chicago school' as represented by Henry C. Simons. For Simons, the basic criterion for economic policy is whether it promotes individual liberty, or not -- and individual liberty is incompatible with concentration of too much power in too few hands. The Austrian school, by contrast, asserts that the basic criterion is whether economic policy promotes accumulation and concentration of capital in the hands of a few. The Austrian school promotes the idea that by promoting a system that favors capital growth and concentration, individual liberty will somehow be automatically protected and enhanced. The (original) Chicago school, by contrast, promotes the idea that by promoting a system that fosters individual liberty, the greatest material progress is fostered, protected and enhanced.

In any event, I find Jesse's analysis fairly convincing, although I wouldn't call it 100% scientific.

I think Jesse does a good job of presenting an aspect of our postmodern world system of global capital that is real and pertinent, without getting carried away into CT or losing sight of the fundamental importance of individual liberty.

nominal GDP

nominal GDP to debt ratio has to be used, else you are adjusting for inflation on debt and that doesn't work out.

Yes, currency devaluation is a way to "reduce" the debt and sure this is one major possibility.

I also see this as a way to bail out the Euro if they kick out countries or revert back to old currencies.

Robert, can you please

Robert, can you please explain in laymen's terms how this is a way to bail out the Euro. It is not at all clear to me from your excerpts how this works, nor is it clear how "this is, in essence, more kicking the can down the road and money printing." How is this "money printing"? I guess I can see that in the reduced China reserve requirements, since that will lead to the creation of more Chinese money. Is there money printing going on in US$?

I appreciate any efforts in helping me understand this and thanks for your informative blog.

miasmo.com

it makes it cheaper to swap

So, let's say people believe Germany is pulling out of the Euro and going to use their own currency. So, that means Euros won't be worth as much, they would be devalued. But by Central banks stepping in and swapping currencies very cheaply, that means the Euro has more value because it's cheaper to swap it for U.S. dollars and it can help prop up the Euro to it's original exchange rate before Germany pulled out.

It's a way to keep the Euro for devaluating. If it takes more Euros to get a dollar then the value of the Euro went down. Sovereign debt is in Euros, and no surprise they interest to sell the bonds dropped today.

It's kind of like they made a "back up" currency to the Euro in dollars,Yen, Swiss Francs.

Also, small interest rate break

Here are two ways of saying the same thing.

First, in plain English --

Excerpted from NYT article by Binyamin Appelbaum (30 November 2011), Central Banks Take Joint Action to Ease Debt Crisis --

Then, in technical jargon, from the Fed's press release --

liquidity vs solvency

Thanks for the response and also for the zero hedge link below.

If I am understanding "swaps" correctly, this will basically help Euro banks (and consequently Wall St banks who have exposure to them) with any short term liquidity crisis, but does nothing for long term solvency since "swaps" need to be traded back at some point?

Here is the Krug Man's take on it:

http://krugman.blogs.nytimes.com/2011/11/30/what-the-central-banks-did-t...

He is "mystified" by the market reaction.

miasmo.com

fundamentally that's what this post says

in bold, why this is so incredible to the markets we don't know. i.e. swaps and such help bail out the banks but don't solve the problems at all.

this article explains what swaps do pretty well

A Zerohedge article goes into how swaps protect banks and explains how using swaps are a bail out. There is all sorts of derivatives out there and exposure to European debt.

Derivatives Protect Banks the Way Nukes Protect Freedom

Not at all. Derivatives are not assets, not real economic resources. Derivatives, to make it crude, are surplus value. Like nukes in the thousands they are there to 'make the rubble bounce'. Derivatives outvalue all the collective wealth of the world many times over. Like nukes they only are here to destroy.

It is easy to think that the banksters get rich on these things. But really they destroy banks Derivatives are asymmetric hedges because the underlying assets types are dissimilar and markets different. This way, GS lost money this quarter.

From ZeroHedge. This is how derivatives are surplus value.

Now, consider this: the top four US banks (JPM Chase, Citibank, Bank of America and Goldman Sachs) control nearly 95% of the US derivatives market, which has grown by 20% since last year to $235 trillion. That figure is a third of all global derivatives of $707 trillion (up from $601 trillion in December, 2010 and $583 trillion mid-year 2010. )

Breaking that down: JPM Chase holds 11% of the world’s derivative exposure, Citibank, Bank of America, and Goldman comprise about 7% each. But, Goldman has something the others don’t – a lot fewer assets beneath its derivatives stockpile. It has 537 times as many (from 440 times last year) derivatives as assets. Think of a 537 story skyscraper on a one story see-saw. Goldman has $88 billon in assets, and $48 trillion in notional derivatives exposure. This is by FAR the highest ratio of derivatives to assets of any so-called bank backed by a government. The next highest ratio belongs to Citibank with $1.2 trillion in assets and $56 trillion in derivative exposure, or 46 to 1. JPM Chase's ratio is 44 to 1. Bank of America’s ratio is 36 to 1.

Burton Leed

Expanding Debt, and Nominal GDP - Think of Argentina

For all that is good and bad in this policy of monetization of debt and GDP, the past-masters remain, Argentina. Argentina has monetized debt, expanded the GDP and created 20% inflation. Australia and China did big stimulus and had no recession. Argentina did big money expansion as Argentina always does.

Like all things ecomomic, monetizing debt has a price, for U.S., Argentina and now Europe. Other extreme is Switzerland. Swiss have a long term economic debate re Finanz Kapital oder Arbeit Kapital? Money or Work?

U.S. has expanded its M1 mightly in the last 2 years. This stuff is Chicago School B.S which is not empirical. It is modern witchcraft.

http://www.federalreserve.gov/releases/h6/current/

Burton Leed

Context - SDR basket and Currency Wars

I have failed to provide context in my presentation of recent commentary at Jesse's Café Américain, by omitting a major contextual component in Jesse's analysis of the recent action by the Fed (and related tri-lateral or 'Anglo-American' central banks) to shore up the Euro crisis by injecting Eurodollars.

I omitted Jesse's discussion on SDRs in context of the "currency wars" theories popularized by James Rickards (author of "Currency Wars: The Making of the Next Global Crisis"). See, Wikipedia article Currency_war. Jesse also discusses the current phase in this era of 'Currency Wars', namely the 'Third Gold War'. (Café Américain, 5 May 2010)

The "Currency Wars" buzz has, of course, threaded its way in and out of discussion here at EP, mostly back in 2010. Notably, using the EP search engine, there's a link to a guest post on ZeroHedge (Tyler Durden) by Maurizio D'Orlando of AsiaNews.it, "Currency Wars And The Fed's Demise" (20 November 2010) that relates the grand currency wars meme to our little lives here in USA as affected by Fed actions. See,

188.126.66.66/article/guest-post-currency-wars-and-fed%E2%80%99s-demise

Jesse's long-term analysis relates to the emerging IMF Special Drawing Rights (SDRs) 'currency', presently based on a basket of national currencies. The fundamental questions, especially long-term, are (1) whether the SDR basket could or should include not only major currencies but also PM, and, (2) whether the US $ and the British £ are over-represented in the currency basket.

Note: Jesse's Café Américain doesn't purport to be an information source like EconomicPopulist.org, however, I find the commentary there helpful in understanding what's going on, especially when both Europe and the USA are involved. Graphs and valid information sources are cited, but Jesse's Café Américain is primarily to present one person's opinion.

From the blog page --

Context - NGDP as Fed targeting

I have failed to provide context in my presentation of recent commentary at Jesse's Café Américain, by insufficient attention to the word and concept of 'targeting'.

Jesse suggests that the Fed may be trending toward making a fundamental change in the models that it uses to analyze data and decide policy. Jesse's focus is on proposed Fed targeting of NGDP goals. Such targeting would abandon or de-emphasize the current more-or-less statutory targeting of (1) employment (including reduction in unemployment) and (2) inflation -- in favor of targeting growth measured as NGDP.

This is the approach of Scott Sumner (UK professor of economics), presented by Sumner in WSJ video interview, posted by Jesse as background on Sumner's approach. See, this WSJ webpage. Also see, Wikipedia article on Scott Sumner.

PDFs and webpages of Sumner's work are available from the UK libertarian think-tank, Adam Smith Institute, at their website, www.adamsmith.org. In particular, summary and free download of PDF (11 April 2011) titled The case for NGDP targeting - lessons from the Great Recession is available at this webpage.

Jesse's criticism of proposed Fed policy of NGDP targeting --

BTW: It's interesting that Sumner points mainly to mismanagement (or worse?) of regulatory functions as the core of USA economic problems. He points out that whereas the US has suffered three major financial collapses over the past century, Canada has suffered none of these. He suggests that the US could learn from the better regulatory structure and practices of Canada.