Hat tip to Firedoglake, for picking this up from MSNBC and The London Guardian:

In remarks that will fuel the row around excessive pay, Lord Griffiths, vice-chairman of Goldman Sachs International and a former adviser to Margaret Thatcher, said banks should not be ashamed of rewarding their staff.

Speaking to an audience at St Paul’s Cathedral in London about morality in the marketplace last night, Griffiths said the British public should “tolerate the inequality as a way to achieve greater prosperity for all”

Continued downstairs. . .

With public anger mounting at the forecast of bumper bonuses for bankers only a year after the industry was rescued by the taxpayer, he said bankers’ bonuses should be seen as part of a longer-term investment in Britain’s economy. “I believe that we should be thinking about the medium-term common good, not the short-term common good … We should not, therefore, be ashamed of offering compensation in an internationally competitive market which ensures the bank businesses here and employs British people,” he said.

Griffiths said that many banks would relocate abroad if the government cracked down on bonus culture. “If we said we’re not going to have as big bonuses or the same bonuses as last year, I think then you’d find that lots of City firms could easily hive off their operations to Switzerland or the far east,” he said.

What Lord Griffiths is spewing is standard conservative wrong-wing economic horse patooties. The plain fact is that if there is not enough income spread around all income levels, then something economists call aggregate demand generation falter, and the economy gets flush down the crapper. In fact, income inequality is exactly what caused the First Great Depression, according to Franklin Roosevelt’s Federal Reserve Chairman, Marriner Eccles. In his memoirs, 'Beckoning Frontiers (New York, Alfred A. Knopf, 1951), Eccles explained:

''As mass production has to be accompanied by mass consumption, mass consumption, in turn, implies a distribution of wealth -- not of existing wealth, but of wealth as it is currently produced -- to provide men with buying power equal to the amount of goods and services offered by the nation's economic machinery.'' [Emphasis in original.]

Instead of achieving that kind of distribution, a giant suction pump had by 1929-30 drawn into a few hands an increasing portion of currently produced wealth. This served them as capital accumulations. But by taking purchasing power out of the hands of mass consumers, the savers denied to themselves the kind of effective demand for their products that would justify a reinvestment of their capital accumulations in new plants. In consequence, as in a poker game where the chips were concentrated in fewer and fewer hands, the other fellows could stay in the game only by borrowing. When their credit ran out, the game stopped.

That is what happened to us in the twenties. We sustained high levels of employment in that period with the aid of an exceptional expansion of debt outside of the banking system. This debt was provided by the large growth of business savings as well as savings by individuals, particularly in the upper-income groups where taxes were relatively low. Private debt outside of the banking system increased about fifty per cent. This debt, which was at high interest rates, largely took the form of mortgage debt on housing, office, and hotel structures, consumer installment debt, brokers' loans, and foreign debt. The stimulation to spend by debt-creation of this sort was short-lived and could not be counted on to sustain high levels of employment for long periods of time. Had there been a better distribution of the current income from the national product -- in other words, had there been less savings by business and the higher-income groups and more income in the lower groups -- we should have had far greater stability in our economy. Had the six billion dollars, for instance, that were loaned by corporations and wealthy individuals for stock-market speculation been distributed to the public as lower prices or higher wages and with less profits to the corporations and the well-to-do, it would have prevented or greatly moderated the economic collapse that began at the end of 1929.

The time came when there were no more poker chips to be loaned on credit. Debtors thereupon were forced to curtail their consumption in an effort to create a margin that could be applied to the reduction of outstanding debts. This naturally reduced the demand for goods of all kinds and brought on what seemed to be overproduction, but was in reality underconsumption when judged in terms of the real world instead of the money world. This, in turn, brought about a fall in prices and employment.

Unemployment further decreased the consumption of goods, which further increased unemployment, thus closing the circle in a continuing decline of prices. Earnings began to disappear, requiring economies of all kinds in the wages, salaries, and time of those employed. And thus again the vicious circle of deflation was closed until one third of the entire working population was unemployed, with our national income reduced by fifty per cent, and with the aggregate debt burden greater than ever before, not in dollars, but measured by current values and income that represented the ability to pay. Fixed charges, such as taxes, railroad and other utility rates, insurance and interest charges, clung close to the 1929 level and required such a portion of the national income to meet them that the amount left for consumption of goods was not sufficient to support the population.

This then, was my reading of what brought on the depression.

Here’s another reason income inequality can be very bad if it becomes too large. Remember a few years ago, when the New York Yankees were sweeping into every World Series year after year after year, there was some talk about somehow placing a cap on the Yankees’ payroll? The idea was that the Yankees were such a rich franchise, compared to all the other major league baseball teams, that they were literally in a league by themselves, able to outbid everybody else for the best players. Having all the best players, of course, gives the Yankees an unfair advantage, and – except for the point spread - the outcome of any game in which the Yankees played was a foregone conclusion. And there was never any doubt about the playoffs and the World Series: the Yankees would always dominate. Unless some way was found to negate the Yankees’ payroll advantage and make sure that other teams were able to hire and retain talented players, the game itself would suffer. Who would want to come see their home team play against the Yankees if it was certain that the home team would lose? Who would bother to buy seasons tickets if the outcome of the playoffs and the World Series would always favor the Yankees because the monopoly on talent the Yankees commanded precluded the possibility of the home team ever winning? Such outcomes -- or more accurately, just the expectation of such outcomes -- would drag down fan enthusiasm, and ticket sales for all other major league franchises would wither, even further strengthening the Yankees’ financial juggernaut. A self-reinforcing cycle, of good talent flowing only to the Yankees, would, in the end, lead to the destruction of major league baseball itself.

That’s pretty much the situation we’re in now, regarding the shocking disparity in pay between Wall Street and Main Street. Average annual earnings for production and nonsupervisory workers was $31,615 in 2008.

(Based on the statistics reported in these tables and a little work in a spreadsheet).

That is less than one tenth what JP Morgan Chase is going to pay each of its employees on average, $353,834. Goldman Sachs is on track to pay each of its employees an average of $386,429. (See this Bloomberg article.) The controversy over the Yankees’ ability to outbid other teams for top players was at a time that the Yankees were not even at twice the average pay per player. Imagine what would have happened if the Yankees could afford to pay its players an average of ten times more what other teams paid.

As former savings and loan fraud investigator William Black recently wrote in How the Servant Became a Predator: Finance’s Five Fatal Flaws:

The U.S. real economy suffers from critical shortages of employees with strong mathematical, engineering, and scientific backgrounds. Graduates in these three fields all too frequently choose careers in finance rather than the real economy because the financial sector provides far greater executive compensation. Individuals with these quantitative backgrounds work overwhelmingly in devising the kinds of financial models that were important contributors to the financial crisis. We take people that could be conducting the research & development work essential to the success of our real economy (including its success in becoming sustainable) and put them instead in financial sector activities where, because of that sector's perverse incentives, they further damage both the financial sector and the real economy.

Still not convinced? How about this, from Sara Robinson back at the end August:

A liberal democratic society is a complex system that's designed to be very resilient and self-correcting in the face of all kinds of extremism. But the health of that system -- especially its natural immunity to would-be attackers -- ultimately depends on just one factor. It cannot survive without people's ongoing confidence in a functioning political contract.

When it's working right, this contract guarantees the upper classes predictable, reliable wealth in return for their investments. It promises the middle class mobility, comfort, and security. It ensures the working classes fair reward for fair work, chances to move ahead, and protection against very real risk that they'll be forced into poverty if they can't work any more. Generally, as long as everybody gets their piece of this constantly re-negotiated deal, everybody stays invested in keeping the system going -- and a democratic society will remain upright, healthy, and moving mostly forward.

For the past four decades, conservatives have done everything in their power to dismantle that essential contract, and thus destroy our mutual confidence in the fundamental agreements that allow any democratic system to function. (None dare call it treason -- but a solid case could be made.) This isn't news: by now, most of us can recite the litany, chapter and verse, of the all the many ways they hacked away at America's essential ability to function as the Constitution intended.

But the biggest loser, as always, has been the working class -- the people whose only real power lies in their sweat and their numbers. Their faith in the promise of democratic self-government has been shattered through years of union-busting, farm foreclosures, factory exports, college grant cuts, subprime mortgage scams, and all manner of betrayal, treachery, neglect, and abuse. Over in the comments threads at Orcinus, we hear from these furious folks almost every day. The way they see it, representative democracy has repeatedly failed to deliver on anything it might have once promised them. At this point, the disgust runs so deep that anybody who's got other ideas -- theocracy, corporatocracy, anarchy, whaddaya got? -- has a fair shot at getting their attention.

Now, here’s the thing. If you saw the PBS Frontline special yesterday evening, The Warning, about the decision NOT to regulate financial derivatives in the mid-1990s, one of the dramatic quotes used at the beginning to hook the audience is that if there had been meaningful regulation of derivatives there would have been massive financial turmoil.

Massive financial turmoil. Well, yeah, duhhhh! The blood suckers of Wall Street would of course be in an uproar if anyone actually tried to shut down their casino and make them play honest. I hope people are prepared to face a horrific downturn in financial market indicators if serious financial reform is ever enacted, because, of course any serious reform that forces the financial system back into subservience to the real economy will mean that Wall Street’s world has ended. I just hope people are prepared for the wailing and gnashing of teeth when that happens.

What must be understood is that the people responsible for this mess – Lord Griffiths, Robert Rubin, Larry Summers, Alan Greenspan, Phil Gramm, Dick Fuld, Lloyd Blankfein, Jamie Dimon, John Mack and all the others – really believe that the financial system can be a source of wealth. But the reality is that it can’t; the financial system can never create wealth - it can only manage wealth, speculate on it, and redistribute it.

Now that last, redistribute wealth, is the key. We want the financial system to redistribute previously accumulated wealth, by allocating it to those entrepreneurs that seem to have a good idea for creating new wealth. But that’s not what the financial system has been doing, for nearly three decades now.

Roosevelt University economics professor Ozgur Orhangazi last year wrote a book entitled, Financialization and the US Economy, in which he notes, "The largest and most important use of funds by the NFCs (non-financial companies) is the expenditures made to acquire capital goods for productive purposes." (I disagree; the most important, but certainly not the largest, is spending on research and development. Capital expenditures is the second most important use of funds by NFCs.) Wikipedia has a useful definition of capital goods:

Individuals, organizations and governments use capital goods in the production of other goods or commodities. Capital goods include factories, machinery, tools, equipment, and various buildings which are used to produce other products for consumption. Capital goods, then, are products which are not produced for immediate consumption; rather, they are objects that are used to produce other goods and services. These types of goods are important economic factors because they are key to developing a positive return from manufacturing other products and commodities.

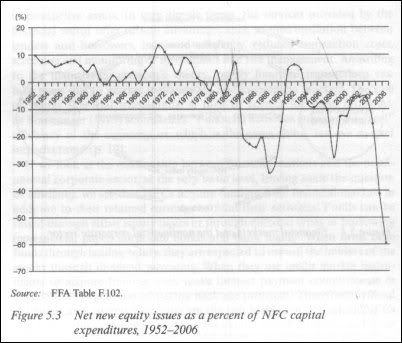

Prof. Orhangazi shows that since 1984, new equity issues have been less than capital expenditures by U.S. non-financial companies, except for the three years of 1991 to 1993. In other words, non-financial companies do NOT use the stock market to raise funds for capital improvement programs.

In fact, Orhangazi notes,

Figure 5.3 shows net funds raised through equity issuance, this time as a percent of capital expenditures (recall that in Figure 2.14 we saw NFC stock buybacks as a percent of NFC / gross value added). It is evident that the stock market has not historically been a major source of NFC funds. On a quarterly basis, its contribution never exceeds 18 percent of capital expenditures. On average its contribution has been below 10 percent, even in the 1952-1980 period before (the increase in stock buybacks. However, there is a dramatic change in the relationship between the stock market and the NFCs starting in the early 1980s. Except for brief periods, in the post-1980 era the net equity issuance of the NFCs has been negative and often large. The NFCs have indeed been buying back their own stocks. The stock market has turned into an institution through which NFCs channel funds to financial markets, not the other way around.

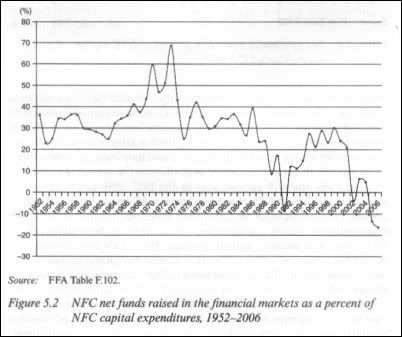

But that's just the stock market, some might reply. OK, well, Prof. Orhangazi looked at financing from all financial markets, Here's the

percentage of capital expenditures by U.S. non-financial companies that was raised in U.S. financial markets from 1952 to 2006.

In fact, the financial system has been extracting wealth from the real economy. Here’s a stunning graph from a July 2003 paper by Professor James Crotty of the University of Massachsetts, Amherst, The Neoliberal Paradox: The Impact of Destructive Product Market Competition and Impatient Finance on Nonfinancial Corporations in the Neoliberal Era

This is why middle class and working class wages have stagnated and even declined the past three decades. This is why U.S. companies flee “high priced” labor in the U.S. and re-locate manufacturing facilities to countries whose low labor costs have more to do with the lack of workplace safety, environmental, and consumer protections than anything else. This is why companies refuse to spend the money to pay for the externalities – like pollution - they create. This is why pension funds have been raided, and labor unions repeatedly attacked.

But Lord Griffiths, Robert Rubin, Larry Summers, and all the rest do not understand all this. You have to understand, they honestly think that the financial system, by itself, is a source of wealth. And you look at the vast riches these people have amassed in their careers in finance, and it’s hard to say that they are wrong. But now we’ve reached the point that the real economy can no longer carry the usurious and speculative burden the financial system imposes on it. Aggregate demand generation has been decimated by income inequality: doesn’t what Mariner Eccles described a half century ago sound uncomfortably familiar today?

Are Lord Griffiths, Robert Rubin, Larry Summers evil? I would argue only in the sense of St. Augustine, who wrote “For what is that which we call evil but the absence of good?”

Back in late 1800s there arose the trusts, massive industrial conglomerates mostly organized by the House of Morgan and the Rockefellers. A series of financial collapses resulted from this concentration of economic power (income inequality, again). Fortunately, in response there arose great Populist and Progressive leaders such as Minnesota Congressman Charles Lindbergh, father of the famous aviatior that flew across the Atlantic. In 1913, Congressman Lindbergh wrote a little book entitled Banking and Currency and The Money Trust

The banks are properly the clearing housed for money and credit exchanges, but they have misapplied their trust and have become our commercial masters. Many of them have associated themselves with the gambling speculators and are now speculating for themselves. Further, the people’s deposits are being used by them and those to whom they loan to pyramid in stocks, bonds, and other securities, which aggregate at the present time approximately amounts to $50,000,000,000 and is rapidly nearing the $100,000,000,000 mark. Excessive dividends and interest are charged and compounded semiannually and annually on this sum. That decreases our net earnings, increases the price of the commodities we buy, and prevents a proper reduction in the hours of labor required. . . .

SNIP

The speculation and gambling that is incidental to our banking and currency system is simply appalling, and it is absolutely ridiculous that we should tolerate it, and pay the cost of its continuance.

SNIP

It must be apparent to anyone that the money with which to pay the expenses incurred by operating this system (by which I mean to include the whole system of trusts) is collected from the people by capitalizing the products of our energy and even discounting the future in the form of stocks, bonds, and securities issued, on which they collect dividends and interest. This is being accomplished by a reduction of our wages and of the prices for which we sell our products, or the services we render as well as by increasing the price of what they control that we must buy. By inversion this prevents a proper reduction in the hours of labor. These have not decreased, nor has our pay increased proportionately with the new mechanical devices and the new methods of application which have immensely increased our productive energy, but the additional product which has resulted from their use has been capitalized in order that the dividends which we pay shall increase. All of these things were scientifically figured out, then commercialized, then speculatized, and finally gamblerized both as to the present and the future. All have been overdone and all pooled as a common charge against the products accruing from the expenditure of our life’s energy.

Many of us were children when the extortion began, and we can hardly blame our parents for permitting the initiation of what we have allowed to be developed into a full-fledged, scientific, legalized system of extortion. But now, since we understand its effects, our children ought to look back on us with shame if we permit its continuance. It is not the bankers who have primarily fastened upon us this system of capitalizing our life energies for their own selfish use. It is the banking and currency system, which we have allowed to remain in operation, and create special interests. The people alone have the power to amend or change it. Therefore we and not the bankers are responsible for the existence of the present system.

Yes, it was complete folly to think that financial services could replace the real economy, especially manufacturing, as a source of wealth. There were people who warned about this in the 1980s and 1990s, when Reagan began dismantling the pro-industrial policies in favor of free trade and free financial markets. But as we see now, free financial markets have only served to loot the real economy.

Lord Griffiths warns that if the banskters can’t keep their obscene wages of sin, then they will flee to Switzerland. I have two responses to that. 1. Cross-border capital controls. 2. Does Switzerland have air defenses against cruise missiles?

Does that second answer sound shrill? Perhaps, too militant? More Americans are dieing every month for lack of medical care than were killed on 9-11. We have an overton window to move here, people: we must radically alter the financial system. The Obama administration is just now beginning to wake up to the fact that banksters will be banksters and corporatists will be corporatists, now matter how many trillions in tax payer bailouts you hand them. That’s why we’re starting to see some movement against executive pay, against the trust exclusion for health insurers, for Medicare-E or Americare. Now is not the time to dial down our shrillness; now is the time to press our advantages. Lord Griffiths wants to talk scary? So can we.

We have the responsibility to seize back our own economic destiny. No one else will do it for us. It is up to us to bring the good to this issue

Comments

It is amazing how many people

equate capitalism with democracy. Capitalism can destroy democracy as we are seeing with the astroturfing, 5 lobbyists to 1 congressperson, and massive misinformation campaigns by U.S. Chamber of Commerce.

What is sorely needed Countervailing Power - Capitalism needs this.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

American Capitalism = NO Accountability

American capitalism has evolved into a situation where there is no accountability. Who has really has been held accountable for this crisis? Even with Lehman Brothers those who crashed the company haven't had to disgorge any past profits.

Look, Larry Summers pushes hard for de-regulation. He gets a very influential job with the Obama Administration. Goldman Sachs makes huge bets in OTC market with AIG and loses but gets $93 billion from gov't to cover their losses. AIG makes all kinds of bets its ass can't cash and it gets bailed out. The list is endless.

But, we suffer the consequences. We lose our homes, jobs and shirts.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

LTCM - another example of NO Accountability

Do people remember Long Term Capital Management? In 1998, LTCM practically brings down the financial system because of greedy and reckless bets ($1.25 trillion notional value in interest rate swaps). They get bought out - I am sure the hedge fund partners got a good chunk of change in the bail out. John Meriweather, founder of LTCM, goes one to start several other hedge funds after that.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

I'm curious as to how much

I'm curious as to how much longer we're going to tolerate this baloney. In any other country these clowns would have been grabbed from their beds and torn to pieces months ago. What's wrong with us, America?

Frustrating.

I think it's a number of factors: complacency, apathy, not being told truth by corporate media, and a certain level of "dummy downism".

could you imagine if the national evening news leadoff with a report like PBS' Frontline - the warning. Maybe more people would listen.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

Where are the pitchforks?

Bad as things are, I just don't sense critcal mass out there. The safety net (full of holes as it is) gives people hope. People are still eating and "getting by," and they have a pretty short attention span. Sunday afternoon football and talking heads seem to have replaced religion as the "opiate of the masses." Also, there is the knowledge that the bank doesn't really want your house (thus slow foreclosure), and you can't go to jail for "just owing money." Even the "We want our $$$ back" signs at events have vanished. People adjust to new circumstances and Garrison Keillor tells them it isn't worth worrying about. Bernie Madoff has been sent to jail, and small time ponzi operators are being arrested on the six o'clock news. People have stopped paying attention to the oligarchy and, anyway, they are being publicly (verbally) flogged before being allowed to go ahead and take their bonuses and grow richer still. It will take a larger crisis than we've had, but at least we've learned something about the half-life of public outrage.

Frank T.

Frank T.

Labeled Terrorists

Remember anyone doing that would be labeled a terrorist and never heard from again.

They are secure in their ivory towers short of anything but a complete collapse of the economy. If that were to happen so many people would have literally nothing something would happen. Hence the warning from Bernanke and Paulson to Bush that if they didn't get a bailout (no questions asked) there would be rioting in the streets. They probably failed to mention that the rioting would take place on Wall Street directed towards Wall Street.

Econoterrorists

Remember we used to worry about fanatics bringing down physical structures or the OPEC mob doing clever speculation in markets ahead of their changes in policy. Then money laundering by narcotraffickers was a big concern in the 1990s. If you have TBTF threatening to bring down the economy if they don't get their way on bailouts, that smacks of extortion and econoterrorism. Of course, the Bush administration and Greenspan were of the "look the other way, the markets will take care of it" school of denial. This White Collar crime on a systemic scale is such a threat to our economy that we need to define it and go after it. If we can find money for Goldman Sachs, we can certainly afford to hire more attorneys and investigators at Justice (and the SEC). How many executives at AIG and Moody's were short the XLF last year? Or were they just asleep?

Frank T.

Frank T.