Key takeaways:

- The CROWN Act is legislation that protects students, workers, and housing applicants from race-based hair discrimination.

- 30 states have enacted some version of the CROWN Act, building momentum for a federal version to pass in Congress.

- Expansions of civil rights laws like the CROWN Act are more urgent than ever amid Trump administration attacks on nondiscrimination protections.

In an era of Trump administration attacks on nondiscrimination protections and diversity, equity, and inclusion (DEI) initiatives, workers and students need the guardrails included in the CROWN Act more than ever.

The CROWN Act stands for Creating a Respectful and Open World for Natural Hair. It expands existing civil rights law to prohibit race-based hair discrimination in schools, housing, and workplaces. Far from being solely focused on aesthetics, the CROWN Act protects against implicit bias and policing of Black and brown bodies. It codifies hair discrimination as racism and prohibits employers, public schools, and housing agencies from imposing whiteness as the uniform for success.

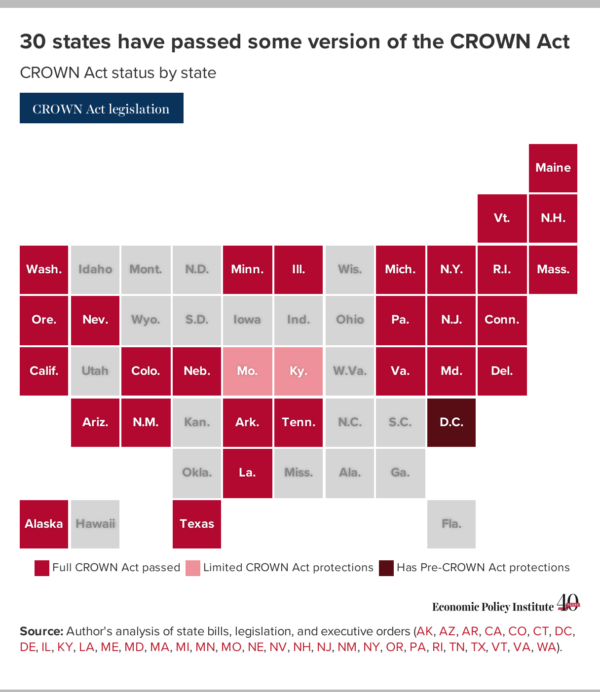

The CROWN Act is now law in 30 states

Pennsylvania and Rhode Island became the most recent states to pass the law in 2025, joining a growing list of states that have passed some form of the CROWN Act. Similar to the limited protections in Kentucky (which only provides public service and employee protections), Missouri also recently passed a limited version of the law that only applies to educational institutions—not workplaces or housing.

Figure A

Since the start of the second Trump administration, five states (Florida, Mississippi, Ohio, North Carolina, and South Carolina) have introduced at least one version of the CROWN Act.

Expanding CROWN Act legislation at the local level can be a significant incremental step toward expanding protections more broadly. In at least three of the states that introduced legislation, local CROWN laws have been adopted in cities including Charlotte, North Carolina, Columbus, Ohio, and Miami Beach, Florida. Such local policies have proven helpful in laying groundwork for passage of state laws elsewhere; for example, localities in Pennsylvania and Missouri passed CROWN Act laws years prior to these passing at the state level.

It’s time to pass the CROWN Act in Congress

Representative Watson Coleman (D-NJ) and Senator Cory Booker (D-NJ) introduced a federal version of the CROWN Act in the House and Senate last February. Neither bill has received a vote. With 60% of states already having passed the CROWN Act, the policy clearly has enough popular support to pass both chambers and become law.

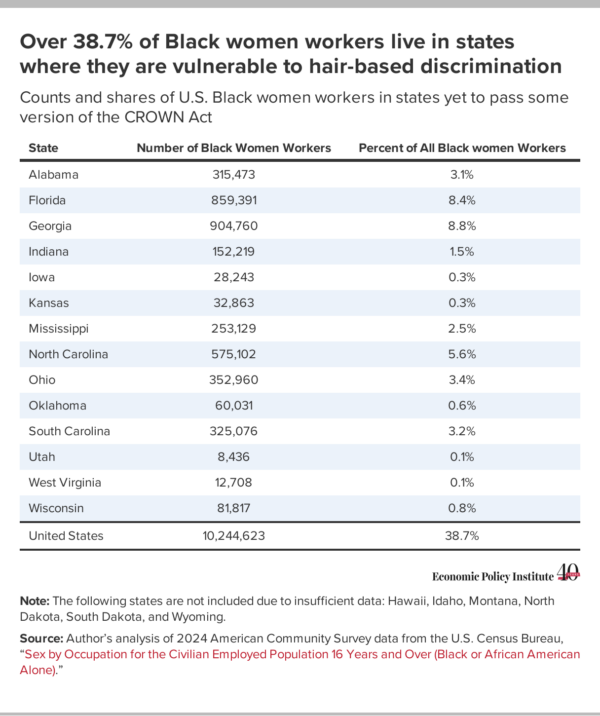

A federal CROWN Act would provide consistent nationwide protection against hair discrimination for workers—especially Black women workers who have larger pay disparities and who are intersectionally impacted by a history of racist laws. Over 38.7% of Black women workers live in states where they are vulnerable to hair-based discrimination, based on the most recent 2024 data. That’s a slight improvement from the 44% of Black women workers who lacked protections in 2023, thanks to six more states—Kentucky, Missouri, New Hampshire, Pennsylvania, Rhode Island, and Vermont—recently passing some version of the CROWN Act.

Table 1

Although some states did not have large enough populations of Black women to be tracked in the data presented in Table 1, Black students and workers in states with smaller Black populations remain susceptible to discrimination. In South Dakota, for example, a student was told to cut their locks or leave school. Black students have shared similar stories in states across the country with varying Black population density.

Expansion of the CROWN Act must be coupled with strong enforcement

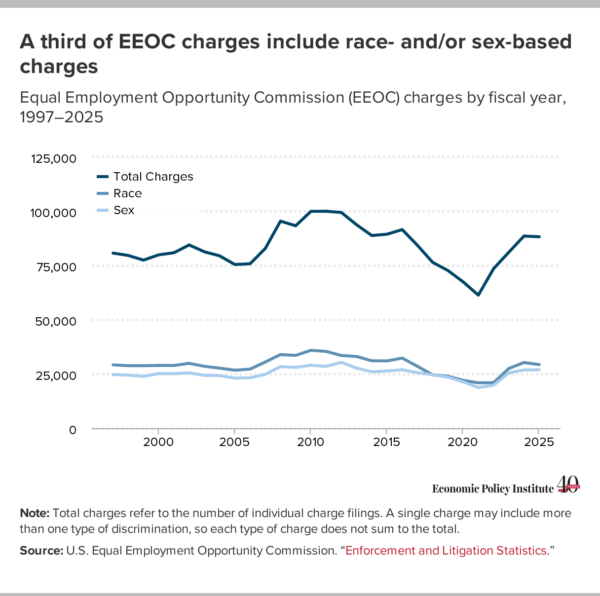

In an anti-DEI political climate, preventing hair-based discrimination must be coupled with addressing a growing crisis in federal and state nondiscrimination enforcement systems. Current threats to the Equal Employment Opportunity Commission’s (EEOC) enforcement mission are eroding protections for Black and brown workers. The EEOC was established by the Civil Rights Act of 1964 (the same law that the CROWN Act would expand) and was designed to be an independent federal agency to protect workers and promote fairness and equity in employment. The EEOC’s role in reducing discrimination has helped to boost average income by $493 to $1,233 per person since 1960. Historically, the EEOC has been a key source of protection for Black and brown people and women: A third of all EEOC charges were related to race (29,338) or sex (26,941) last year.

1

Last year, the Trump-appointed chair of the EEOC hijacked the agency’s mission by actively soliciting complaints from white male workers and encouraging “DEI-related discrimination” claims of “reverse racism.” In addition to assigning a new chair, the Trump administration has weakened the EEOC by removing the ability to collect full pay data, limiting gender data collection, and removing commissioners—preventing a quorum and disrupting proceedings.

The Civil Rights Act itself and the protections that the EEOC was created to enforce are at risk. And some states are following the Trump administration’s lead by weakening state-level civil rights laws and enforcement systems. For example, in 2025, Iowa became the first state in history to strip nondiscrimination protection from a protected class when it removed gender identity from its state Civil Rights Act. In response, many cities and counties expanded their local civil rights ordinances to ensure protections against discrimination based on gender identity, but in 2026 the state went a step further and banned local governments from protecting any class not explicitly listed in state law. These recent legislative changes explicitly targeted trans people for discrimination, but will also have the broader effect of preempting local governments from adopting any expanded civil rights protections in the future, including local versions of the CROWN Act.

In the meantime, discrimination has not stopped and continues to have a measurable impact on Black, brown, and women workers—especially related to opportunities for securing a job and workplace advancement. New research finds that 59% of white adults hold anti-Black prejudice, contributing to a greater likelihood that Black applicants are rejected from jobs compared with their white counterparts. Women are paid 18.6% less than men. The disparity increases when considering race: Black women are paid 68.3% and Hispanic women are paid 64.5% of white men’s pay.

It is imperative to both expand protections like the CROWN Act at the local, state, and federal levels and strengthen state civil rights enforcement, while working toward eventual restoration of the EEOC’s capacity to carry out its mission to protect against discrimination in the workplace.

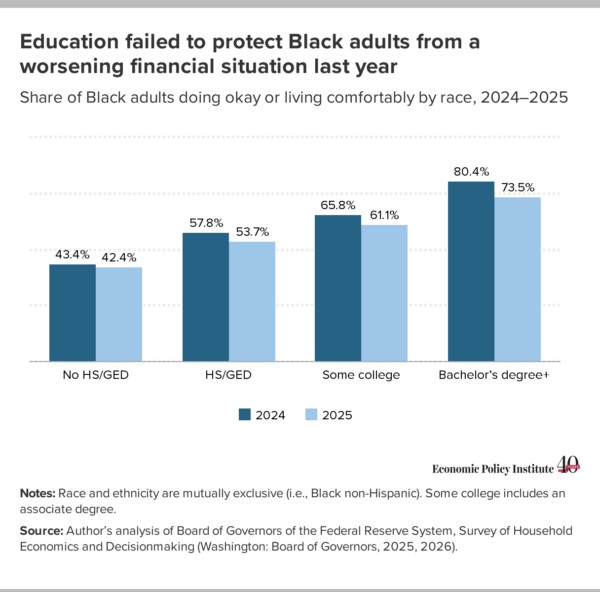

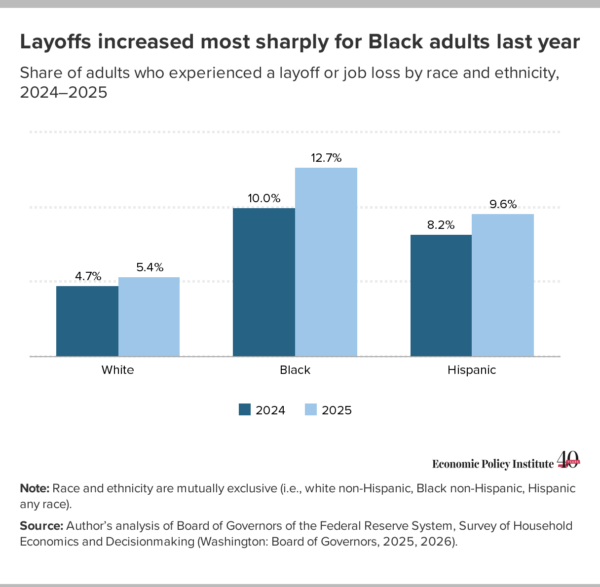

Black adults were more likely to experience a sharp increase in layoffs last year

Black adults were more likely to experience a sharp increase in layoffs last year

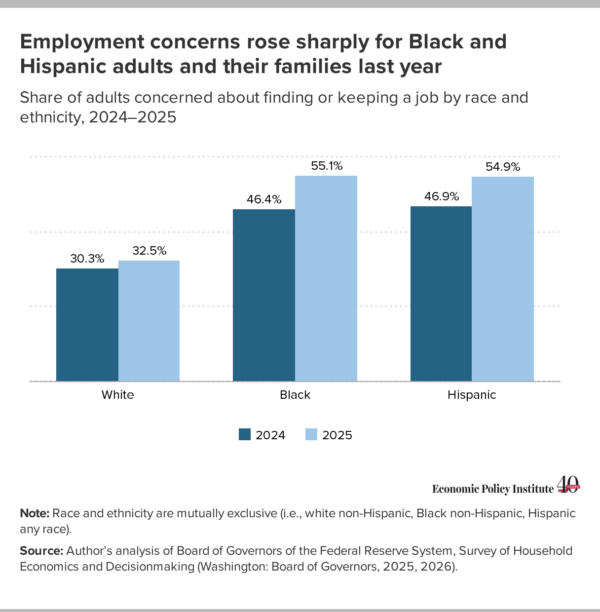

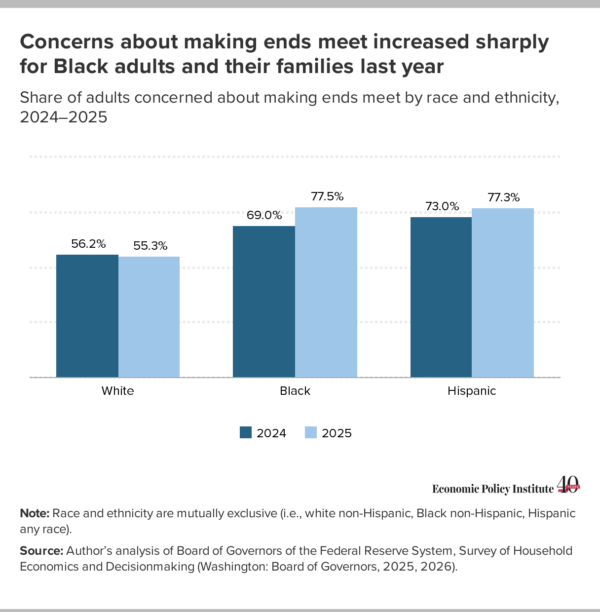

Black adults and their families have grown increasingly more concerned about their economic security

Black adults and their families have grown increasingly more concerned about their economic security

We cannot address the affordability crisis without dealing with its root causes

We cannot address the affordability crisis without dealing with its root causes

Recent comments